Globalisation is not merely the free flow of goods across borders. It represents a complex web of multinational legal frameworks, regulatory compliance requirements, and strategic cross-border transactions that demand sophisticated legal expertise. Law firms serve as the essential architects enabling international business operations, navigating intricate treaty obligations, mergers and acquisitions, and evolving geopolitical landscapes. This article explores how law firms facilitate global commerce through strategic networks, contrasting expansion methodologies, and adaptive responses to shifting international dynamics.

| Point | Details |

|---|---|

| Cross border expertise | Law firms provide cross border expertise enabling multinational operations across multiple jurisdictions. |

| Strategic alliance networks | International networks and alliances are key strategies for global law firms to coordinate cross border projects. |

| Mergers and acquisitions | Chinese firms pursue mergers and acquisitions while Western firms prefer organic growth to expand abroad. |

| Transnational mindset shift | Firms must adapt rapidly to shifting geopolitical regionalisation by adopting a transnational mindset that prioritises compliant global operations. |

Law firms provide the essential infrastructure for multinational corporations to operate across jurisdictions. Law firms provide cross-border legal expertise enabling multinational operations through advice on international treaties, mergers and acquisitions, project finance, and regulatory navigation. Without this specialised counsel, businesses would struggle to interpret conflicting legal regimes, manage compliance obligations, or structure transactions that span multiple countries.

Consider project finance for large infrastructure developments. Law firms advise on complex financing arrangements involving multiple lenders, governmental entities, and regulatory bodies across different jurisdictions. The Qatar LNG project exemplifies this, where legal teams coordinated financing structures complying with Qatari law, international banking regulations, and investor protection frameworks simultaneously. Such transactions require deep knowledge of international financial law, contractual drafting expertise, and the ability to negotiate terms acceptable to parties operating under diverse legal traditions.

Global mergers and acquisitions present another domain where law firms prove indispensable. Cross-border M&A legal structuring demands coordination across multiple regulatory approval processes, tax optimisation strategies, and cultural due diligence considerations. Law firms manage these multifaceted transactions by assembling teams with jurisdiction-specific knowledge whilst maintaining strategic oversight of the entire deal structure.

Regulatory compliance in multiple jurisdictions represents perhaps the most consistent demand on law firms supporting globalisation. Multinational corporations face overlapping and sometimes contradictory regulatory requirements across markets. Law firms develop practical frameworks to navigate this complexity:

The value of hiring international lawyers becomes evident when businesses expand beyond domestic markets. These specialists bring not only technical legal knowledge but also cultural intelligence and relationship networks that smooth cross-border transactions. They understand how legal concepts translate across different legal traditions, whether common law, civil law, or hybrid systems, and can anticipate potential friction points before they escalate into costly disputes.

Law firms also play a crucial advisory role in treaty interpretation and application. International trade agreements, bilateral investment treaties, and multilateral conventions create rights and obligations that businesses must navigate carefully. Legal counsel helps clients leverage treaty benefits, such as preferential tariff treatment or investor protection mechanisms, whilst ensuring compliance with treaty obligations that might restrict certain business practices.

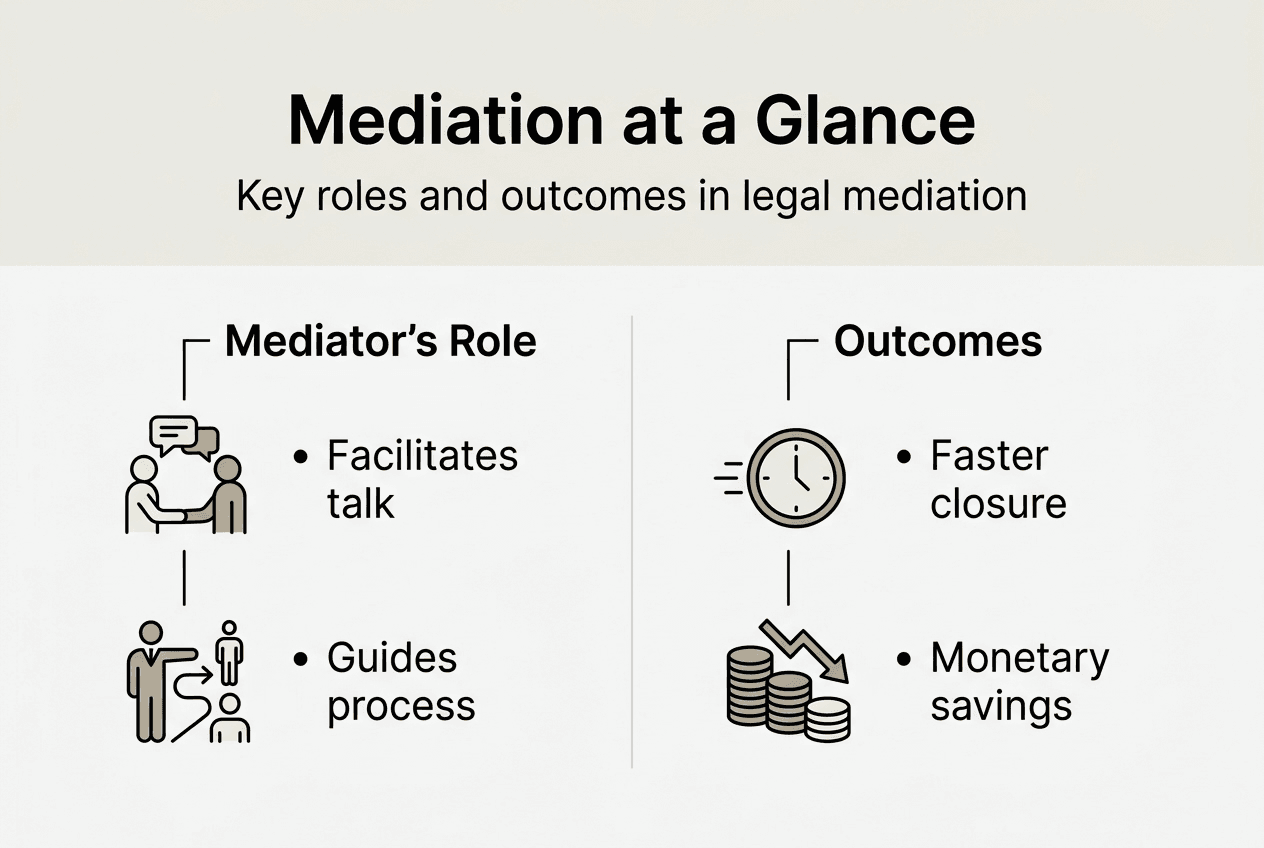

Law firms adopt various structural models to deliver global services, each with distinct advantages and trade-offs. International alliances and networks range from informal referral arrangements to highly coordinated multi-jurisdictional practices operating under unified brand identities. Research shows informal alliances with strong communication interfaces yield higher effectiveness than either purely formal structures or loosely connected networks.

The effectiveness of alliance structures depends significantly on how firms balance autonomy with coordination. Empirical studies examining law firm alliances reveal that moderate formalisation combined with robust communication channels produces optimal client outcomes. Too much formalisation creates bureaucratic friction, whilst insufficient structure leads to inconsistent service quality and coordination failures.

| Model type | Structure | Advantages | Disadvantages |

|---|---|---|---|

| Informal alliance | Loose referral network | Maximum firm autonomy, low overhead | Inconsistent service quality, weak coordination |

| Formal alliance | Coordinated network with shared standards | Balanced autonomy and consistency | Requires significant management investment |

| Merger | Full integration under single entity | Unified culture and systems | Loss of local identity, integration challenges |

| One firm model | Globally coordinated practice groups | Seamless client service, knowledge sharing | Complex governance, potential conflicts |

The ‘one firm’ model represents the most integrated approach, where law firms operate as a single global entity with coordinated practice groups spanning multiple jurisdictions. This model facilitates seamless client service, as teams can mobilise resources across offices without navigating inter-firm politics or conflicting billing arrangements. However, it requires sophisticated governance structures to manage diverse partnership interests and maintain cultural cohesion across geographically dispersed offices.

Mergers offer another path to global coverage, though they present significant integration challenges. When law firms merge across borders, they must reconcile different partnership structures, compensation systems, and professional cultures. Successful mergers require years of careful integration work to realise the promised synergies of combined expertise and market reach.

Choosing international law firms requires understanding these structural differences. Clients should evaluate not only the firm’s geographic footprint but also how effectively its offices collaborate on cross-border matters. A firm with offices in 50 countries delivers little value if those offices operate as independent silos unable to coordinate complex transactions.

Pro Tip: When selecting a global law firm, request examples of recent cross-border matters and speak with lawyers from multiple offices involved in the same transaction. This reveals the quality of internal coordination and communication systems that directly impact service delivery.

Alliance effectiveness hinges on several factors beyond formal structure. Trust between member firms, compatible professional standards, and aligned economic incentives all contribute to successful collaboration. The most effective alliances invest in relationship building through regular partner meetings, joint training programmes, and secondment opportunities that build personal connections across member firms.

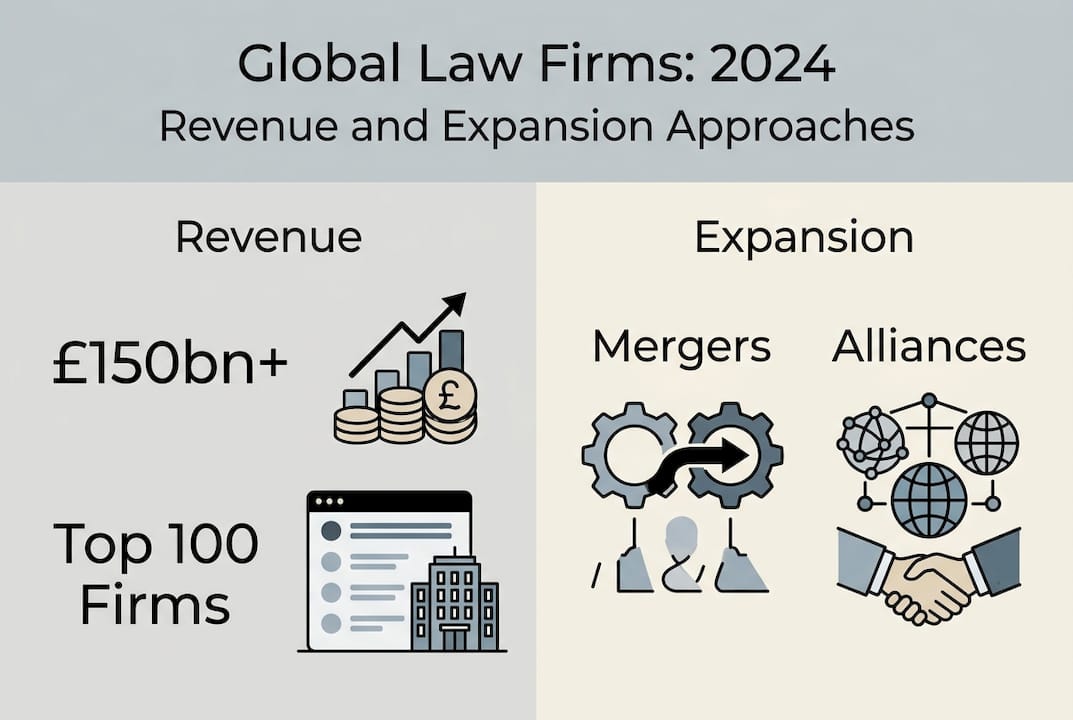

The globalisation strategies of law firms vary significantly between established Western practices and rapidly expanding Chinese firms. Chinese law firms pursue rapid global growth mainly through mergers and acquisitions, whilst Western firms focus on organic expansion and building local expertise over extended timeframes. These contrasting approaches reflect different market dynamics, regulatory environments, and strategic priorities.

Chinese firms have pursued aggressive international expansion to support Chinese corporations investing abroad under Belt and Road Initiative projects and other outbound investment programmes. King & Wood Mallesons exemplifies this approach, having expanded through strategic mergers to establish presence across Asia, Europe, and the Middle East. Dacheng Dentons, formed through merger, now operates 125 offices globally, demonstrating the scale achievable through acquisition-driven growth.

Western firms traditionally favour organic expansion, opening new offices through lateral partner hires or deploying existing partners to establish local presence. This methodology prioritises cultural integration and quality control, ensuring new offices align with the firm’s established standards and client service philosophy. Organic growth proceeds more slowly but typically produces more cohesive firm cultures and consistent service delivery.

| Metric | Chinese firms | Western firms |

|---|---|---|

| Primary expansion method | Mergers and acquisitions | Organic growth and lateral hires |

| Overseas offices growth (2018-2024) | 47.5% increase | 12% increase |

| Average integration timeline | 1-2 years | 3-5 years |

| Client driver | Outbound Chinese investment | Established multinational relationships |

Global 100 law firms surpassed £150bn revenue in 2024, demonstrating the substantial economic scale of international legal services. Chinese firms have expanded overseas offices by 47.5% since 2018, far outpacing Western competitors. This rapid expansion creates both opportunities and challenges, as firms must quickly integrate diverse legal cultures and maintain quality standards across newly acquired practices.

The differing expansion strategies also reflect regulatory environments. Chinese firms operate within a legal market that has only recently opened to international competition and still maintains restrictions on foreign firm activities. This creates strong incentives for Chinese firms to establish overseas presence through acquisition rather than attempting to build relationships and reputation from scratch in unfamiliar markets.

Western firms benefit from decades of established international relationships and brand recognition that facilitate organic expansion. When a prominent London or New York firm opens a new office, it often brings existing client relationships that provide immediate revenue whilst the office builds local market presence. Chinese firms typically lack these pre-existing relationships in foreign markets, making acquisition of established local firms a more viable entry strategy.

Pro Tip: Businesses evaluating law firms should consider expansion methodology as an indicator of service consistency. Firms that grow organically often maintain more uniform quality standards, whilst those expanding through acquisition may exhibit greater variation between offices during integration periods.

The international business law guide landscape increasingly features both Western and Chinese firms competing for multinational client mandates. This competition benefits clients through expanded service options and competitive pricing, though it also requires more careful due diligence to ensure selected firms possess genuine cross-border capabilities rather than merely geographic presence.

Geopolitical fragmentation and regionalisation trends present profound challenges for law firms supporting global commerce. Geopolitical shifts require law firms to adapt to sanctions, supply chains, and environmental, social, and governance issues that increasingly dominate cross-border transactions. The relatively stable post-Cold War globalisation era has given way to a more fractured international landscape characterised by strategic competition, technology restrictions, and supply chain reconfigurations.

Sanctions compliance has evolved from a specialised niche into a core competency for any firm advising multinational clients. Western sanctions targeting Russia, China, Iran, and other jurisdictions create complex compliance matrices that businesses must navigate. Law firms develop sophisticated sanctions screening systems, advise on permissible transaction structures, and help clients assess risks of secondary sanctions that might apply to non-sanctioned parties dealing with sanctioned entities.

Supply chain legal risks have intensified as companies diversify sourcing away from concentrated manufacturing bases. This ‘friendshoring’ trend requires legal counsel on establishing operations in new jurisdictions, navigating unfamiliar regulatory environments, and managing contractual relationships across more complex supplier networks. Law firms help clients balance efficiency gains from concentrated supply chains against resilience benefits of geographic diversification.

Environmental, social, and governance obligations increasingly shape international transactions. Investors demand ESG due diligence, regulators impose disclosure requirements, and stakeholders scrutinise corporate environmental and social impacts. Law firms advise on ESG compliance frameworks, disclosure obligations, and risk mitigation strategies that satisfy multiple stakeholder constituencies.

Key adaptation strategies for law firms navigating this shifting environment include:

“The distinction between domestic and international law has blurred considerably. Law firms must shift from local to transnational mindsets, leveraging global networks amid blurred domestic-international law lines. What appears as a purely domestic transaction often implicates international regulatory regimes, whilst ostensibly international matters may trigger domestic compliance obligations.”

This transnational mindset requires lawyers to think beyond their home jurisdiction’s legal framework and consider how multiple regulatory regimes interact. A European company acquiring a US business must consider not only European merger control and US antitrust review but also potential Chinese regulatory approval if the target has significant Chinese operations or technology with national security implications.

The international law role UK business continues evolving as the United Kingdom establishes its post-Brexit international legal framework. UK firms advise clients on navigating the changed relationship with European Union law whilst capitalising on new treaty relationships and regulatory autonomy. This transition illustrates how geopolitical shifts create both challenges and opportunities for legal practitioners.

Leveraging global networks becomes essential for managing overlapping regulatory regimes. No single lawyer can maintain current expertise across all relevant jurisdictions, but well-coordinated networks enable firms to mobilise specialist knowledge as needed. The most effective firms invest in knowledge management systems that capture expertise across their networks and facilitate rapid information sharing when novel legal issues arise.

Regionalisation trends may partially reverse decades of globalisation, but they do not eliminate the need for cross-border legal services. Instead, they create more complex regional regulatory frameworks that require equally sophisticated legal navigation. Law firms that successfully adapt to this environment will combine deep regional expertise with the ability to coordinate across regions when client needs demand it.

Navigating the complexities of international business law requires experienced counsel who understand both legal technicalities and commercial realities. Ali Legal offers comprehensive support for businesses and professionals managing cross-border legal challenges, combining deep expertise with practical, client-focused service delivery.

Our civil litigation services extend to complex international disputes requiring coordination across multiple jurisdictions. When conflicts arise in cross-border transactions, our team brings strategic litigation expertise that protects your interests whilst managing the procedural complexities of multi-jurisdictional disputes. We understand how to leverage international legal frameworks to achieve favourable outcomes for clients facing global legal challenges.

For businesses navigating commercial disagreements with international dimensions, our commercial litigation solutions provide strategy-led dispute resolution when stakes are high. We advise on enforcement of international arbitration awards, recognition of foreign judgements, and resolution of conflicts involving parties across multiple countries.

Our international business law services support UK businesses expanding globally and international clients establishing UK operations. From contract negotiation to regulatory compliance, we provide the legal foundation for successful international commerce.

Law firms face regulatory complexity across multiple jurisdictions, requiring coordination of diverse legal requirements that may conflict. Geopolitical risks including sanctions and trade restrictions demand constant monitoring and adaptive strategies. Cross-border coordination challenges arise from time zones, language barriers, and differing professional cultures that can impede seamless service delivery.

Firms leverage transnational legal networks to access jurisdiction-specific expertise when conflicts arise between legal regimes. They develop compliance frameworks that identify applicable laws and establish protocols for managing contradictions. Expert legal counsel advises clients on jurisdictional risks, helping them structure transactions to minimise exposure to conflicting requirements whilst maintaining commercial viability.

Alliances provide multi-jurisdictional coverage without the complexity and cost of full mergers, increasing organisational agility. Member firms retain local market knowledge and relationships whilst accessing broader geographic reach through alliance partners. Clients benefit from consistent service standards across jurisdictions and coordinated advice that considers implications across multiple markets simultaneously.

Firms develop specialised teams focused on sanctions compliance, supply chain restructuring, and ESG obligations that dominate current cross-border transactions. They establish regional expertise centres to capitalise on supply chain diversification creating opportunities in emerging markets. Enhanced regulatory monitoring systems track geopolitical developments that might impact client operations, enabling proactive rather than reactive legal strategies.

Many individuals and businesses assume that generic legal services suffice for their needs. This widespread belief overlooks how personalised legal solutions address unique risks, values, and compliance requirements far more effectively. Tailored legal services transform client satisfaction, operational efficiency, and strategic outcomes across civil litigation, family law, corporate matters, and regulatory compliance. This guide explores how customised legal support delivers superior results compared to standardised approaches, helping you understand when bespoke solutions provide the greatest value for your specific circumstances.

| Point | Details |

|---|---|

| Tailored client focus | Tailored legal solutions enhance satisfaction and loyalty by addressing each client’s unique needs and preferences. |

| Flexible communication and fees | Personalised services accommodate preferred communication styles and flexible fee arrangements to fit budgets and schedules. |

| Improved retention and trust | Client centred solutions lead to higher retention and fewer disputes as guidance reflects individual risk tolerances. |

| Tech driven efficiency | Customised AI and contract lifecycle management deliver substantial efficiency gains and cost savings compared with generic tools. |

Generic legal services treat all clients identically, ignoring individual circumstances and preferences. Client centred legal services enhance satisfaction, loyalty, and retention by addressing unique needs, values, and risk tolerances that standardised approaches overlook. When solicitors customise their advice and delivery methods to match your specific situation, you receive precisely what your matter requires rather than cookie cutter templates.

Personalisation begins with understanding your priorities. Some clients prioritise speed and efficiency, whilst others value detailed explanations and regular updates. Tailored services accommodate these preferences through flexible communication channels, whether you prefer email updates, video calls, or face to face meetings. This adaptability builds stronger solicitor client partnerships founded on mutual understanding rather than rigid procedures.

Flexible fee arrangements represent another dimension of personalisation. Fixed fees suit clients who value budget certainty, whilst hourly billing may benefit those with unpredictable legal needs. Tailored pricing models align costs with your specific matter complexity and risk profile, eliminating the frustration of paying for unnecessary services or receiving inadequate support.

Pro Tip: Request an initial consultation to discuss your preferred communication style and fee structure before engaging a solicitor. This conversation establishes expectations and ensures the partnership fits your working preferences from the outset.

The measurable impact of personalisation appears in retention data. Firms offering customised services report significantly higher client loyalty rates because clients feel understood and valued. Reduced miscommunications lower the risk of disputes and improve case outcomes, as solicitors grasp the nuances of your situation rather than applying generic solutions. When you receive clear legal advice tailored to your circumstances, you make better informed decisions that align with your goals.

“Personalised legal services transform the client experience from transactional to relational, building trust that extends beyond individual matters.”

Key benefits of client centred tailored services include:

Legal technology revolutionises service delivery, but generic tools often create as many problems as they solve. Customised AI and contract lifecycle management solutions yield 55% improvement in key value metrics compared to generic alternatives. This dramatic difference stems from bespoke systems designed for specific legal workflows rather than attempting to serve every possible use case.

Generic AI tools raise significant accuracy concerns, with 40% of legal professionals worried about errors in standardised artificial intelligence applications. Custom AI solutions address these concerns by training on your specific documents, terminology, and legal requirements. When AI understands your particular context, it generates more accurate contract clauses, identifies relevant precedents, and flags potential issues with greater precision.

Contract lifecycle management systems tailored to your organisation reduce legal involvement in routine contracting from 76% to just 39%. This efficiency gain frees solicitors to focus on complex strategic matters whilst automated workflows handle standard agreements. The time savings translate directly into cost reductions and faster business operations, as contracts move through approval processes without unnecessary bottlenecks.

| Metric | Generic Solutions | Tailored Solutions | Improvement |

|---|---|---|---|

| Revenue growth | Baseline | 20% higher | +20% |

| Client retention | Baseline | 30% higher | +30% |

| Operational efficiency | Baseline | Up to 30% gains | +30% |

| Key value metrics | Baseline | 55% improvement | +55% |

Firms using tailored legal software report 20% higher revenue growth and 30% higher retention rates alongside efficiency gains reaching 30% compared to off the shelf alternatives. These improvements compound over time, as custom systems evolve with your changing needs rather than forcing you to adapt to rigid software limitations.

Implementing tailored legal technology follows these strategic steps:

Pro Tip: Prioritise customisation investments in areas with highest transaction volumes or greatest compliance risks. These domains deliver fastest return on investment whilst reducing exposure to costly errors.

Strategic insourcing combined with tailored technology optimises legal spend. By handling routine matters internally with custom tools whilst engaging external solicitors for complex issues, organisations achieve significant cost reductions. This hybrid approach maintains quality whilst eliminating unnecessary external fees for work that customised systems handle efficiently. Proper regulatory compliance becomes more manageable when technology monitors obligations specific to your industry and jurisdiction.

“Custom legal technology transforms solicitors from document processors into strategic advisers, elevating the value they deliver to clients.”

Not every legal matter requires bespoke treatment. Standardisation suits routine tasks, but tailored solutions excel for complex, client specific needs as generic programmes may hinder growth and risk management. Understanding this distinction helps you allocate resources effectively, using standardised approaches where appropriate whilst investing in customisation for matters demanding individualised attention.

Routine legal work benefits from standardisation because consistency improves efficiency and reduces costs. Standard employment contracts, basic non disclosure agreements, and simple property transactions follow predictable patterns where templates serve adequately. These matters involve minimal unique risk factors and well established legal frameworks, making customisation unnecessary and potentially wasteful.

Complex matters demand tailored solutions because generic approaches miss critical nuances. Commercial disputes, regulatory investigations, international transactions, and strategic corporate restructuring involve unique fact patterns, competing interests, and significant financial or reputational stakes. Standardised advice in these contexts proves inadequate and potentially dangerous, as overlooked details create vulnerabilities.

| Scenario | Standardised Approach | Tailored Approach | Recommended |

|---|---|---|---|

| Basic employment contracts | Suitable | Unnecessary | Standardised |

| Complex commercial litigation | Inadequate | Essential | Tailored |

| Routine property conveyancing | Efficient | Excessive | Standardised |

| Multi jurisdictional compliance | Risky | Critical | Tailored |

| Simple NDAs | Appropriate | Overkill | Standardised |

| Strategic M&A transactions | Dangerous | Necessary | Tailored |

Confidentiality considerations further complicate technology choices. Tailored AI use must ensure confidentiality to avoid privilege waiver as public tools may disclose sensitive data, compromising legal protections. Generic AI platforms often process inputs through shared infrastructure, potentially exposing confidential information to unauthorised access or inadvertent disclosure.

Private, customised AI systems mitigate these risks by processing data within controlled environments. When handling privileged communications or sensitive commercial information, invest in bespoke technology maintaining confidentiality rather than risking exposure through public tools. The cost of custom solutions pales compared to potential damages from privilege waiver or data breaches.

Key factors determining when tailored solutions provide superior value:

Understanding the role of legal counsel helps you recognise when generic advice proves insufficient. Solicitors adding genuine value through tailored analysis justify their fees by preventing costly mistakes and identifying opportunities standardised approaches miss.

Personalised legal services deliver practical benefits across diverse practice areas, helping individuals and businesses maintain compliance whilst gaining competitive advantages. Strategic insourcing of high cost legal work leads to significant legal spend reductions when combined with tailored external support for specialised matters. This hybrid approach optimises resource allocation whilst maintaining quality.

Complex regulatory frameworks demand customised compliance strategies. Generic compliance programmes overlook industry specific requirements and jurisdictional nuances that create exposure. Tailored legal advice helps you navigate these complexities by identifying obligations specific to your operations, implementing monitoring systems aligned with your risk profile, and responding to regulatory changes affecting your sector.

Commercial litigation benefits enormously from personalised strategies. Each dispute involves unique relationships, evidence, and business objectives that standardised approaches cannot address effectively. Customised litigation strategies consider your risk tolerance, budget constraints, and desired outcomes, whether that means aggressive pursuit of claims or pragmatic settlement. Understanding your business context allows solicitors to recommend tactics serving your broader interests rather than simply following generic playbooks.

Family law matters inherently require tailored approaches because every family situation differs. Cookie cutter divorce settlements or custody arrangements ignore the specific needs of children, financial circumstances of parties, and cultural considerations affecting families. Personalised family law services account for these unique factors, producing agreements that work for your specific situation rather than forcing you into standardised templates.

Corporate and commercial transactions demand bespoke structuring to optimise tax positions, allocate risks appropriately, and protect strategic interests. Generic transaction documents miss opportunities for value creation and leave vulnerabilities that sophisticated counterparties exploit. Tailored commercial advice identifies these issues and structures deals advancing your objectives.

Practical applications of tailored legal solutions include:

Engaging with commercial litigation specialists ensures your dispute strategy serves broader business goals rather than simply pursuing legal victories. Similarly, comprehensive legal compliance services tailored to your industry and jurisdiction reduce regulatory risks whilst avoiding unnecessary compliance burdens.

Better risk management emerges from personalised legal advice because solicitors understanding your business identify vulnerabilities generic reviews miss. This proactive approach prevents problems rather than simply reacting to crises, supporting sustainable business growth through sound legal foundations.

Having explored how tailored legal solutions deliver superior outcomes, you may wonder how to access these benefits for your specific needs. Ali Legal offers customised legal support designed around your unique circumstances, whether you require assistance with commercial disputes, regulatory compliance, or strategic business matters.

Our commercial litigation services provide strategy led dispute resolution when stakes are high, combining deep sector knowledge with personalised tactics serving your business objectives. We recognise that effective litigation requires understanding your commercial context, not just legal principles. Our regulatory compliance solutions keep your operations sharp and compliant through tailored programmes addressing your specific industry requirements and risk profile. Rather than generic checklists, we develop compliance frameworks fitting your operational realities.

Engaging with specialist solicitors who take time to understand your situation optimises legal outcomes whilst controlling costs. Fixed fee arrangements provide budget certainty, whilst our transparent communication keeps you informed without overwhelming you with unnecessary detail. Contact Ali Legal today to discuss how personalised legal services can address your specific needs and support your goals.

Tailored legal solutions deliver higher client satisfaction through services addressing your unique needs and risk tolerance. They provide significant cost savings and efficiency gains, with custom technology improving key metrics by 55% compared to generic alternatives. Personalised approaches also enable better risk management and regulatory compliance across all practice areas.

Choose tailored services for complex matters involving significant financial stakes, strategic business importance, or confidentiality requirements. Standardised approaches suit routine transactions like basic contracts or simple property conveyancing. If your matter involves unique circumstances, multiple jurisdictions, or potential disputes, personalised legal advice proves essential.

Customised legal technology reduces errors by training on your specific documents and terminology, addressing the 40% accuracy concerns associated with generic AI tools. It decreases legal involvement in routine contracting from 76% to 39%, freeing solicitors for strategic work. Tailored systems also maintain confidentiality better than public tools, protecting privileged information.

Yes, personalised legal services often reduce total costs despite potentially higher hourly rates. Strategic insourcing of routine work combined with tailored external support for complex matters cuts legal spend significantly. Custom technology automates repetitive tasks, whilst personalised advice prevents costly mistakes that generic approaches miss, delivering better value overall.

Assess your matter complexity, strategic importance, and potential consequences. If standardised templates adequately address your situation with minimal unique risk factors, customisation may prove unnecessary. However, if your matter involves significant stakes, unusual circumstances, regulatory complexity, or confidential information, tailored legal solutions provide superior protection and outcomes.

Choosing legal representation often feels like navigating a maze blindfolded. Nearly 80% of law firm clients feel uncared for, revealing a profound disconnect between traditional legal practices and client expectations. Relationship-based legal services flip this script entirely. They prioritise transparent communication, genuine client partnerships, and personalised attention across family law, personal injury, and corporate matters. When solicitors treat you as a strategic partner rather than just another case file, outcomes improve dramatically. This approach transforms legal services from transactional encounters into collaborative relationships built on trust, clarity, and shared goals.

| Point | Details |

|---|---|

| Transparent communication | Clients receive regular updates in plain language so they understand every decision and the associated costs. |

| Client as partner | When treated as strategic partners, solicitors focus on long term outcomes and collaborative problem solving rather than single file results. |

| Personalised attention | Personalised attention enables tailored strategies across family law, personal injury, and corporate matters. |

| Cost clarity | Fixed fees and upfront cost discussions remove surprises and help clients plan their recovery and finances. |

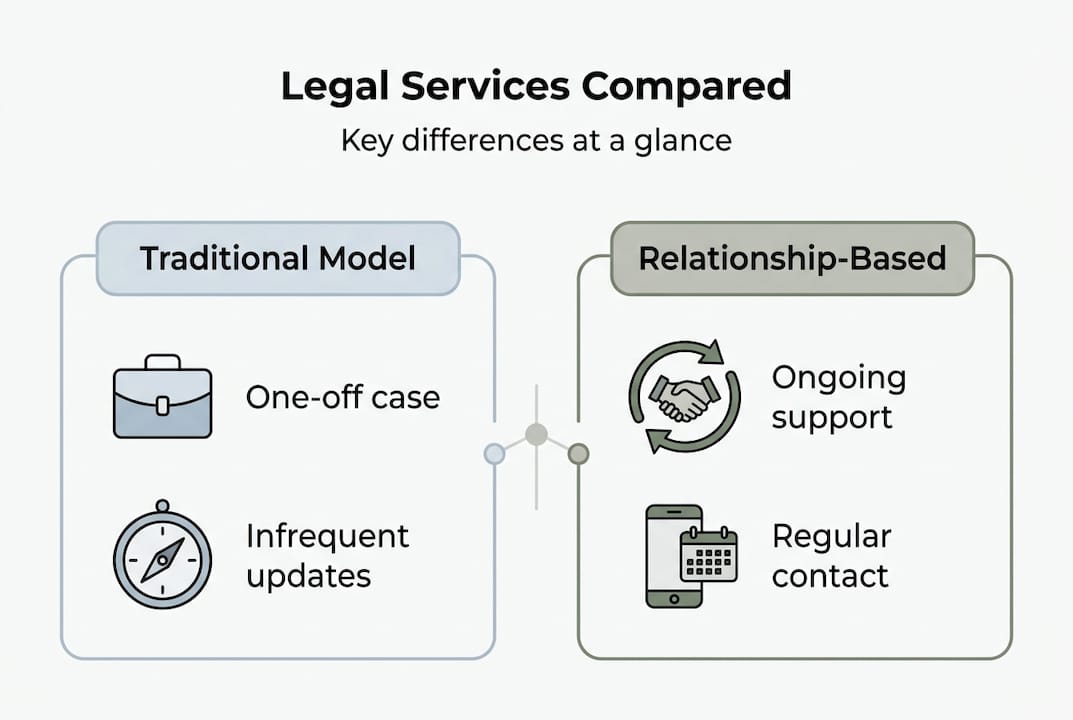

Relationship-based legal services represent a fundamental shift in how solicitors engage with clients. Rather than viewing legal matters as isolated transactions, this approach builds ongoing partnerships centred on understanding your unique needs, circumstances, and goals. The foundation rests on three pillars: transparent communication, genuine empathy, and collaborative problem-solving.

Transparent communication means you receive regular updates without having to chase your solicitor. Your legal team explains complex concepts in plain language, ensuring you understand every decision point. This clarity extends to billing practices, with fixed fees and upfront cost discussions eliminating unpleasant surprises.

Building trust requires more than professional competence. It demands solicitors who listen actively, acknowledge your concerns, and adapt their approach to your communication preferences. Some clients prefer detailed written updates, whilst others value quick phone calls. Relationship-focused firms accommodate these differences naturally.

Practitioners benefit from treating clients as strategic assets for sustainable growth, creating mutual value that extends beyond individual cases. This partnership mindset transforms how legal services function. Your solicitor becomes invested in your long-term success, not just closing the current file.

Pro Tip: Request a feedback session within the first two weeks of engagement. This early checkpoint prevents misunderstandings and establishes clear communication patterns that serve you throughout your legal matter.

When solicitors view you as a partner, they proactively identify opportunities and risks you might not recognise. They anticipate your questions and provide context that helps you make informed decisions. This collaborative dynamic proves especially valuable in complex family disputes, personal injury negotiations, and corporate transactions where outcomes hinge on understanding nuanced details. The importance of clear legal advice becomes evident when you experience genuine partnership versus transactional service.

Personal attention translates directly into better legal strategies. When your solicitor invests time understanding your specific situation, they craft approaches tailored to your circumstances rather than applying generic templates. Family law matters benefit enormously from this personalisation. Divorce proceedings, child custody arrangements, and financial settlements require sensitivity to emotional dynamics alongside legal expertise.

Transparency reduces stress significantly during challenging legal processes. Knowing exactly where your case stands, what steps come next, and how costs accumulate provides peace of mind. Personal injury clients particularly value this clarity whilst recovering from accidents. Regular updates about claim progress, settlement negotiations, and expected timelines help you plan your recovery and financial future with confidence.

Relationship-focused firms empower you to make better-informed decisions. Rather than simply presenting options, they explain the practical implications of each choice. What does accepting this settlement mean for your long-term financial security? How might different custody arrangements affect your children’s wellbeing? These conversations go beyond legal technicalities to address real-world consequences.

Nearly 80% of clients feel uncared for but those treated as strategic assets see better results, demonstrating the measurable impact of relationship-based approaches. Client satisfaction surveys consistently show higher ratings for firms prioritising ongoing engagement and personalised service.

“The difference between feeling like a case number and feeling truly heard cannot be overstated. When your solicitor knows your name, remembers your concerns, and proactively addresses your needs, the entire legal experience transforms from intimidating to manageable.”

Specialised support in family and divorce legal care exemplifies how relationship-based services improve outcomes during life’s most difficult transitions. Similarly, comprehensive personal injury litigation guidance demonstrates how sustained client relationships lead to more favourable settlements and smoother claims processes.

The benefits extend beyond individual cases. Clients who establish strong relationships with their legal teams gain a trusted adviser for future needs. Business clients particularly value this continuity, as their solicitor develops deep understanding of their operations, industry challenges, and strategic objectives over time.

Traditional legal services often operate on a transactional model. You contact a solicitor when problems arise, they address the immediate issue, and the relationship ends when the matter concludes. Communication typically occurs when you initiate contact or when critical deadlines approach. This reactive approach leaves many clients feeling disconnected and uncertain about their case status.

Relationship-based services flip this dynamic. Your solicitor maintains regular contact throughout your matter, providing proactive updates and anticipating your questions. Communication flows naturally in both directions, with your legal team actively seeking your input and feedback.

| Feature | Traditional legal services | Relationship-based legal services |

|---|---|---|

| Communication frequency | Client-initiated or deadline-driven | Regular proactive updates and check-ins |

| Fee transparency | Often hourly billing with unpredictable costs | Fixed fees with upfront cost discussions |

| Client focus | Case-centric approach | Person-centric partnership approach |

| Engagement duration | Ends when matter concludes | Ongoing advisory relationship |

| Feedback mechanisms | Limited or non-existent | Regular satisfaction checks and adjustments |

Fee transparency distinguishes these approaches significantly. Traditional firms frequently bill by the hour, making final costs difficult to predict. Relationship-based practices typically offer fixed fees or clear pricing structures, allowing you to budget confidently. This transparency extends to explaining why certain actions cost more and identifying opportunities to reduce expenses without compromising outcomes.

The philosophical difference runs deeper than communication patterns. Traditional services focus on resolving the immediate legal problem efficiently. Relationship-based services consider your broader circumstances and long-term wellbeing. How does this divorce settlement affect your retirement plans? Will this corporate structure support your business growth over the next decade?

Pro Tip: When interviewing potential solicitors, ask specific questions about their client engagement process. How frequently will they update you? What communication channels do they offer? How do they gather and respond to client feedback? Their answers reveal whether they genuinely prioritise relationships or simply claim to.

Feedback mechanisms prove crucial for service quality. Relationship-focused firms actively solicit your input throughout your matter, adjusting their approach based on your preferences and concerns. This responsiveness creates a collaborative environment where you feel heard and valued. Understanding the role of legal counsel in business and exploring legal retainers for UK businesses illustrates how ongoing relationships deliver superior value compared to one-off engagements.

Family law demands exceptional sensitivity and personalised attention. Divorce, child custody disputes, and financial settlements involve deeply personal matters where emotional support matters as much as legal expertise. Relationship-based solicitors recognise that family law clients need someone who understands their unique family dynamics, not just statutory requirements.

These solicitors invest time learning about your children’s needs, your financial circumstances, and your hopes for post-divorce life. They explain options in context, helping you understand how different arrangements might work practically. This personalised guidance proves invaluable when making decisions that affect your family’s future.

Personal injury litigation benefits enormously from sustained client relationships. Recovery from serious accidents takes time, and your legal needs evolve throughout the process. Relationship-focused solicitors maintain regular contact, adjusting their approach as your medical situation and financial needs change. They coordinate with medical professionals, insurers, and other parties whilst keeping you informed every step of the way.

Corporate law clients gain strategic partners who understand their business inside and out. Rather than calling a solicitor only when problems arise, you have an adviser who knows your industry, competitive challenges, and growth objectives. This deep understanding enables proactive guidance on contracts, compliance, risk management, and strategic transactions.

| Practice area | Client satisfaction rating | Average case duration | Communication frequency |

|---|---|---|---|

| Family law | 4.7/5.0 | 8-14 months | Weekly updates |

| Personal injury | 4.8/5.0 | 10-18 months | Fortnightly updates |

| Corporate law | 4.6/5.0 | Ongoing advisory | Monthly reviews |

Seeking relationship-based legal counsel requires a deliberate approach:

Pro Tip: Prioritise firms with proven track records in your specific legal area that explicitly commit to regular communication and transparent billing. Check online reviews and testimonials for consistent mentions of responsiveness and client care.

Exploring essential family law tips provides valuable context for relationship-based family legal services. Similarly, comprehensive guides on personal injury claims and corporate law in the UK demonstrate how specialised expertise combines with client-focused approaches to deliver superior outcomes across diverse legal matters.

Navigating complex legal matters becomes significantly easier when you partner with solicitors who genuinely prioritise your needs and goals. Ali Legal specialises in relationship-based legal services that transform how you experience legal support. We focus on transparent communication, personalised strategies, and long-term client partnerships across our core practice areas.

Our family and divorce legal care provides compassionate guidance during life’s most challenging transitions. We combine legal expertise with genuine understanding of your family’s unique circumstances. For personal injury matters, our comprehensive litigation support ensures you receive the compensation you deserve whilst maintaining clear communication throughout your recovery. Business clients benefit from our strategic corporate law services that support sustainable growth through proactive legal guidance and transparent advice. Contact Ali Legal today to experience legal services built on trust, clarity, and genuine partnership.

Relationship-based legal services prioritise ongoing client partnerships over transactional interactions. Solicitors invest time understanding your unique circumstances, maintain regular communication, and provide personalised strategies tailored to your specific needs. This approach treats you as a strategic partner rather than just another case file.

Transparent communication and consistent engagement build trust naturally over time. When solicitors proactively update you, explain complex concepts clearly, and demonstrate genuine interest in your wellbeing, you feel valued and confident in their guidance. Regular feedback opportunities ensure your concerns are heard and addressed promptly, strengthening the partnership.

Not necessarily. Many relationship-focused firms offer fixed fees and transparent pricing structures that provide better value than unpredictable hourly billing. The personalised attention and proactive guidance often prevent costly mistakes and delays, ultimately saving money. Understanding the importance of clear legal advice helps you recognise the long-term value of transparent, relationship-based services.

Ask specific questions during initial consultations about communication frequency, feedback mechanisms, and how they tailor strategies to individual circumstances. Request client references and check testimonials for consistent mentions of responsiveness and personalised service. Establish clear expectations early about how often you’ll receive updates and through which channels.

Absolutely. Corporate clients benefit significantly from solicitors who understand their business operations, industry challenges, and strategic objectives. Ongoing advisory relationships through legal retainers for UK businesses provide proactive guidance on contracts, compliance, and growth opportunities. This deep understanding enables solicitors to anticipate needs and provide strategic counsel that supports long-term success.

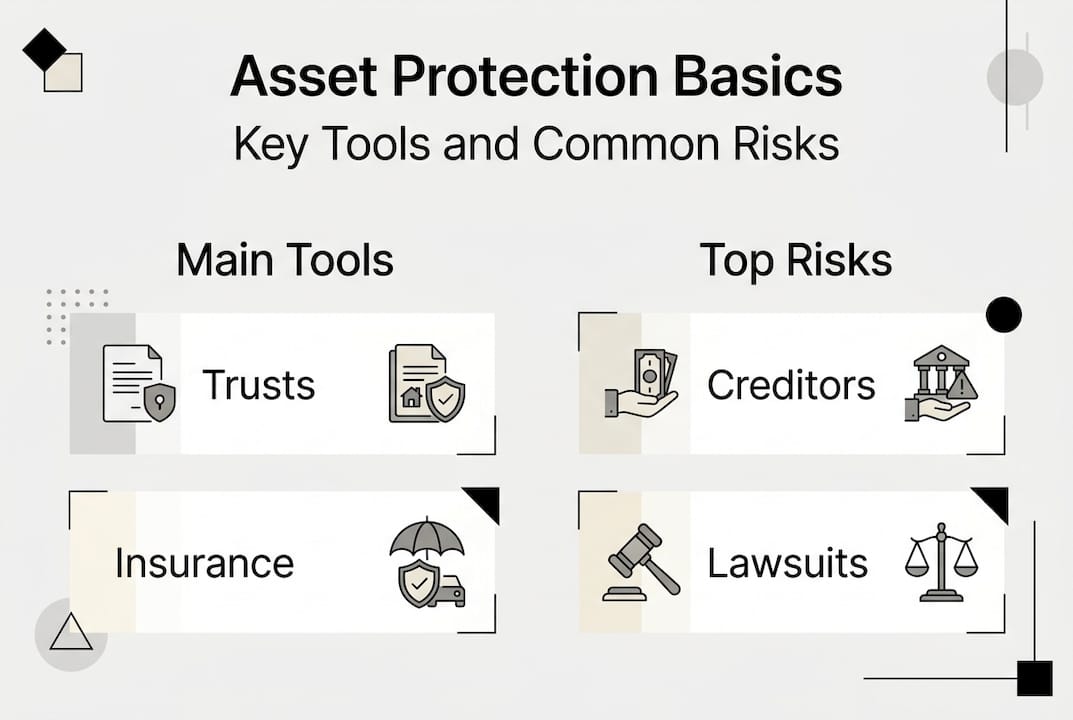

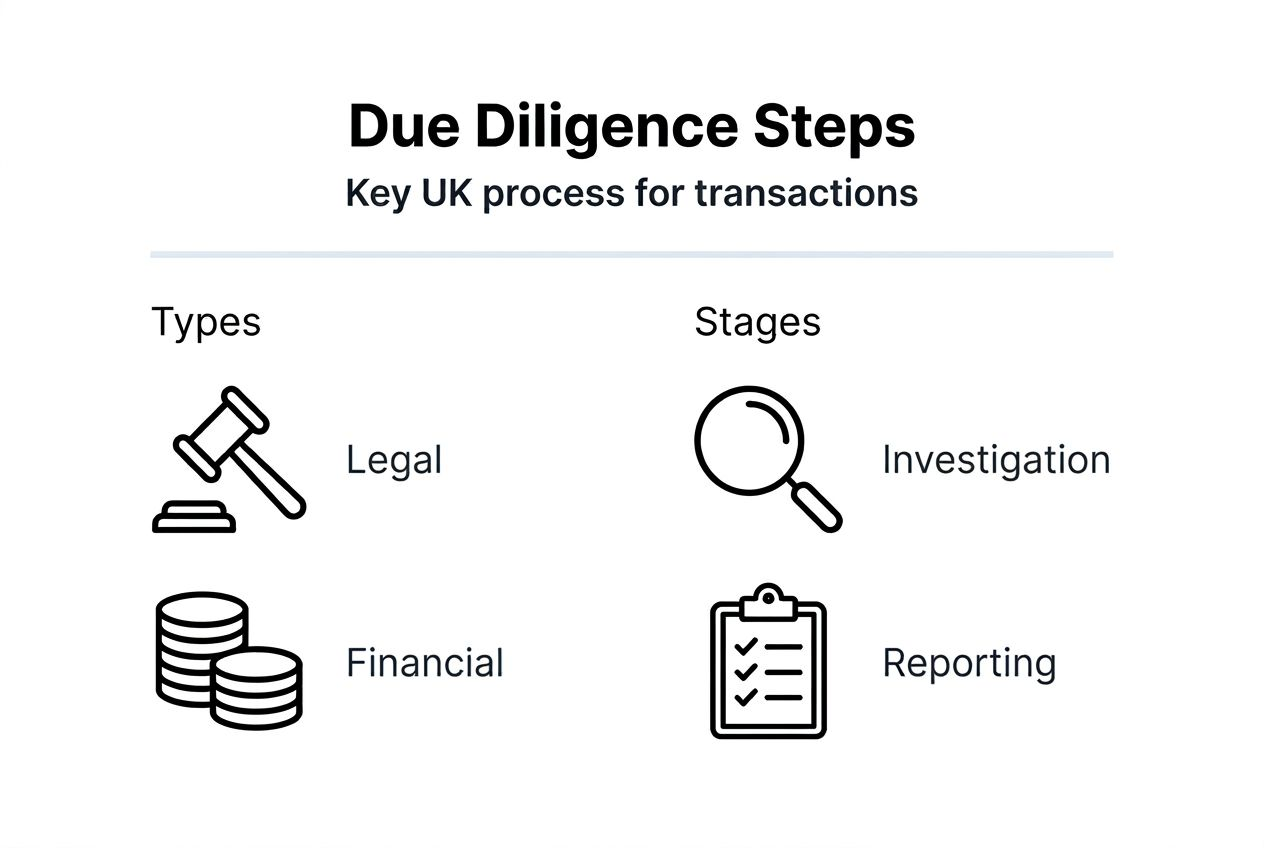

Many people believe asset protection is simply about hiding wealth from creditors or avoiding legitimate obligations. That misunderstanding can lead to poor decisions and legal trouble. True asset protection involves legally structuring your finances and holdings to shield them from genuine risks like lawsuits, business failures, and unforeseen liabilities. This guide clarifies what asset protection actually means, explores proven strategies including trusts and business structures, and explains how UK legal frameworks support these methods. You’ll learn practical steps to evaluate your risks, select appropriate protection tools, and implement them correctly. Whether you’re a business owner or an individual with assets to preserve, understanding these principles helps you make informed decisions and avoid costly mistakes.

| Point | Details |

|---|---|

| Legal protection | Asset protection uses lawful strategies to safeguard personal and business holdings from creditors, lawsuits, and liabilities. |

| Multiple tools | Effective protection combines trusts, insurance policies, and appropriate business structures tailored to individual circumstances. |

| UK compliance | Success requires understanding and following UK legal frameworks to ensure strategies remain valid and enforceable. |

| Professional guidance | Expert legal advice prevents common pitfalls and ensures asset protection plans align with current regulations. |

| Regular reviews | Updating protection measures as circumstances change maintains their effectiveness over time. |

Asset protection refers to strategies that legally protect assets from creditors and liabilities. It’s not about evading legitimate debts or hiding wealth from authorities. Instead, it involves structuring your holdings in ways that make them less vulnerable to claims whilst remaining fully compliant with the law.

The purpose is straightforward: preserve what you’ve worked to build. Business owners face risks from commercial disputes, professional negligence claims, and contract breaches. Individuals encounter threats from divorce proceedings, personal injury claims, and unexpected financial crises. Without proper protection, a single lawsuit or business failure can wipe out savings, property, and investments accumulated over decades.

Several misconceptions cloud understanding of this field. Some think asset protection only matters for the wealthy, but anyone with property, savings, or business interests benefits from appropriate safeguards. Others assume it involves offshore accounts or complex schemes, when often the most effective tools are domestic trusts and properly structured business entities. The key is matching strategies to your specific situation and risk profile.

Key risks that asset protection addresses include:

Understanding legal risk management forms the foundation for effective asset protection. UK law provides various frameworks, from trust legislation to company structures, that enable legitimate protection when used correctly. The challenge lies in selecting appropriate tools and implementing them before problems arise, because courts view protection measures established after a claim surfaces with considerable scepticism.

Several proven methods help safeguard assets, each with distinct advantages depending on your circumstances. The most effective approach typically combines multiple strategies rather than relying on a single tool.

Trusts are a popular legal mechanism used to isolate assets from personal liabilities in the UK. When you place assets into a properly structured trust, they’re owned by the trust itself rather than you personally. This separation means creditors pursuing claims against you cannot easily access trust property. Discretionary trusts offer particular flexibility, allowing trustees to distribute income and capital among beneficiaries as circumstances change.

Insurance provides another essential layer of protection. Professional indemnity insurance shields business owners from negligence claims, whilst liability insurance covers accidents and injuries. These policies transfer risk to insurers, preventing claims from directly threatening your personal wealth. The key is maintaining adequate coverage limits that reflect your actual exposure.

Business structures significantly impact asset protection. Operating as a limited company creates legal separation between business debts and personal assets. If the company faces financial difficulty, creditors generally cannot pursue directors’ personal property beyond their investment in the company. This contrasts sharply with sole traders, whose personal assets remain fully exposed to business liabilities.

| Strategy | Primary benefit | Main limitation |

| — | — |

| Discretionary trusts | Strong creditor protection through legal separation | Requires professional setup and ongoing management |

| Limited companies | Shields personal assets from business debts | Directors may face personal liability for wrongful trading |

| Insurance policies | Transfers risk to insurers with defined coverage | Only protects against insured risks up to policy limits |

| Pension schemes | Protected from most creditors under UK law | Funds locked until retirement age |

UK legal frameworks support these strategies through established trust law, company legislation, and insurance regulations. However, certain limitations apply. Courts can set aside transfers made to defraud creditors, and some debts like personal guarantees pierce corporate protection. Understanding these boundaries prevents wasted effort on ineffective measures.

Practical implementation tips include:

Pro Tip: Many people focus solely on property law when protecting real estate, but combining property ownership structures with insurance and trusts creates far stronger protection than any single method alone.

The most robust protection comes from layering strategies. A business owner might operate through a limited company, maintain comprehensive insurance, place investment property in a trust, and maximise pension contributions. Each layer addresses different risks, and together they create defence in depth that’s difficult for creditors to penetrate. Professional advice ensures these elements work together effectively rather than creating conflicts or gaps.

Successful asset protection depends on understanding and complying with UK legal frameworks to avoid challenges. Several key areas of law shape what’s permissible and what crosses into problematic territory.

Trust law provides the foundation for one of the most powerful protection tools. The Trustee Act 2000 and various case law principles govern how trusts must be established and administered. Trusts created for legitimate purposes like estate planning or protecting vulnerable beneficiaries receive full legal recognition. However, trusts established solely to frustrate creditors may be set aside under the Insolvency Act 1986.

Property law affects how you can structure ownership of real estate and physical assets. Joint tenancy versus tenancy in common creates different inheritance and creditor exposure profiles. Placing property into trusts or companies changes the legal ownership and associated protections. Each structure carries specific implications for tax, succession, and creditor access.

Company law determines how business structures protect personal assets. The Companies Act 2006 establishes limited liability for shareholders, but directors face personal liability for wrongful trading if they continue operating whilst insolvent. Understanding these boundaries helps you maintain protection whilst avoiding personal exposure.

Ensuring legal compliance requires several steps:

The timing of protective measures matters enormously. Courts scrutinise transfers made shortly before or after claims arise, often viewing them as attempts to defraud creditors. Establishing protection during stable periods, as part of normal financial planning, carries far less risk of challenge.

Common legal pitfalls include:

Professional legal advice significantly improves outcomes in securing assets effectively. Attempting to implement complex structures without expert guidance often creates vulnerabilities rather than protection.

Documented professional consultation serves two purposes. First, it ensures your strategies actually work as intended under current law. Second, it demonstrates good faith if anyone later questions your actions. Courts view individuals who sought and followed professional advice more favourably than those who attempted DIY protection schemes.

Estate planning integrates closely with asset protection. Wills, trusts, and succession planning all affect how assets are protected during your lifetime and after death. Coordinating these elements prevents gaps where assets become vulnerable during transitions.

Regular legal reviews keep protection current as laws change. Tax legislation, insolvency rules, and trust law all evolve. What worked five years ago might now create unexpected exposure. Annual reviews with your legal adviser identify needed updates before problems arise.

Implementing effective protection requires systematic evaluation of your situation followed by targeted action. Start by assessing your specific risks and assets, then select appropriate strategies.

Step by step risk evaluation and strategy selection:

Personal finance scenarios demonstrate how protection works in practice. Consider a medical professional facing potential negligence claims. Professional indemnity insurance provides the first line of defence, covering most claims up to policy limits. Placing the family home and investment property into a trust adds another layer, separating personal assets from professional liabilities. Maximising pension contributions moves additional wealth into protected vehicles.

Business contexts require different approaches. A company director might establish a limited company to separate business debts from personal wealth. Key person insurance protects against financial impact if crucial team members become unable to work. Maintaining proper corporate formalities, separate bank accounts, and clear documentation preserves the limited liability protection.

Insurance and liability coverage form essential components of any protection plan. Professional indemnity, public liability, and directors’ and officers’ insurance address different risk categories. The key is matching coverage to actual exposure. Under insurance leaves gaps, whilst excessive coverage wastes money better spent elsewhere.

Planning and regular reviews are key to keeping asset protection measures effective over time. Life changes constantly. You acquire new assets, start businesses, face different risks, and encounter evolving legal frameworks. Annual reviews ensure your protection adapts accordingly.

Pro Tip: The most common implementation mistake is waiting until problems appear before establishing protection. Courts view last minute transfers with extreme scepticism and often set them aside. Effective protection requires planning during calm periods, not crisis response.

Practical implementation considerations include:

Real world application often combines multiple tools. A business owner might operate through a limited company with comprehensive insurance, place investment property in a family trust, maximise pension contributions, and maintain emergency reserves in protected accounts. Each element addresses specific risks whilst together creating robust overall protection.

Common mistakes to avoid during implementation:

The most effective protection balances security with practicality. Overly complex schemes become difficult to maintain and may not survive legal challenge. Simple, well documented structures implemented for clear purposes tend to prove most durable. Focus on legitimate business and family planning objectives, with asset protection as a natural consequence rather than the sole purpose.

Protecting your assets requires more than understanding general principles. You need strategies tailored to your specific situation, implemented correctly within UK legal frameworks. That’s where expert guidance makes the difference between effective protection and wasted effort.

Ali Legal provides experienced civil litigation support when disputes threaten your interests. Our team understands how asset protection intersects with litigation, helping you safeguard holdings whilst resolving conflicts effectively. We’ve guided countless clients through complex situations where proper planning prevented devastating losses.

Our commercial litigation expertise extends to protecting business interests during high stakes disputes. Whether you’re facing contract breaches, partnership disagreements, or creditor claims, we develop strategies that defend your position whilst preserving what you’ve built.

Accessible consultations let us understand your unique circumstances and tailor protection strategies accordingly. We explain options clearly, outline costs transparently, and help you make informed decisions about safeguarding your wealth. Contact Ali Legal today to discuss how we can help secure your financial future with expert legal guidance and proven asset protection strategies.

Asset protection encompasses legal strategies that shield your wealth from creditors, lawsuits, and other financial threats. It matters because unexpected claims, business failures, or legal disputes can eliminate assets you’ve spent years building. Proper protection preserves your financial security whilst remaining fully compliant with UK law.

Trusts create legal separation by transferring ownership to the trust itself, removing assets from your personal estate. This differs from insurance, which transfers risk to insurers, and company structures, which separate business from personal liabilities. Trusts offer particular strength against personal creditors but require proper setup and ongoing administration to remain effective.

Courts can set aside transfers made to defraud creditors under insolvency law, potentially reversing your protection efforts. You might face accusations of fraudulent conveyance if timing or documentation appears suspicious. Improperly structured protection can also trigger unexpected tax liabilities or fail to provide intended benefits, wasting time and money.

Costs vary significantly based on complexity. Simple measures like adequate insurance might cost hundreds annually, whilst establishing trusts typically requires several thousand pounds in legal fees plus ongoing administration costs. Limited company formation costs less than trusts but requires annual compliance expenses. Professional advice helps identify cost effective options for your situation.

Seek advice before problems arise, ideally as part of regular financial planning. Once claims surface or financial difficulty looms, options become limited and courts scrutinise any protective measures closely. Early consultation during stable periods provides maximum flexibility and ensures strategies withstand potential challenges whilst serving legitimate purposes.

Many people believe compensation claims are straightforward processes that guarantee financial recovery after an injury or property damage. The reality proves far more nuanced, involving complex legal requirements, damage calculations, and strategic considerations that significantly impact outcomes. Understanding what compensation claims truly entail, how damages are assessed, and which legal hurdles you might face can transform your approach to seeking restitution. This guide clarifies the fundamentals of compensation claims, explains calculation methods, explores key legal challenges, and outlines the practical steps for filing your claim in 2026.

| Point | Details |

|---|---|

| Definition and scope | Compensation claims seek financial restitution for economic losses like medical bills and non-economic damages such as pain and suffering resulting from negligence. |

| Calculation methods | Economic damages use receipts and bills whilst non-economic damages rely on per diem or multiplier methods to estimate value. |

| Legal proof required | Claimants must establish duty, breach, causation, and harm whilst navigating comparative fault rules that can reduce awards. |

| Settlement likelihood | Approximately 95% of claims settle before trial, making negotiation skills and documentation more critical than courtroom performance. |

| No win no fee considerations | Conditional fee agreements provide access to justice but involve success fees that reduce net payouts and potential disbursement liabilities. |

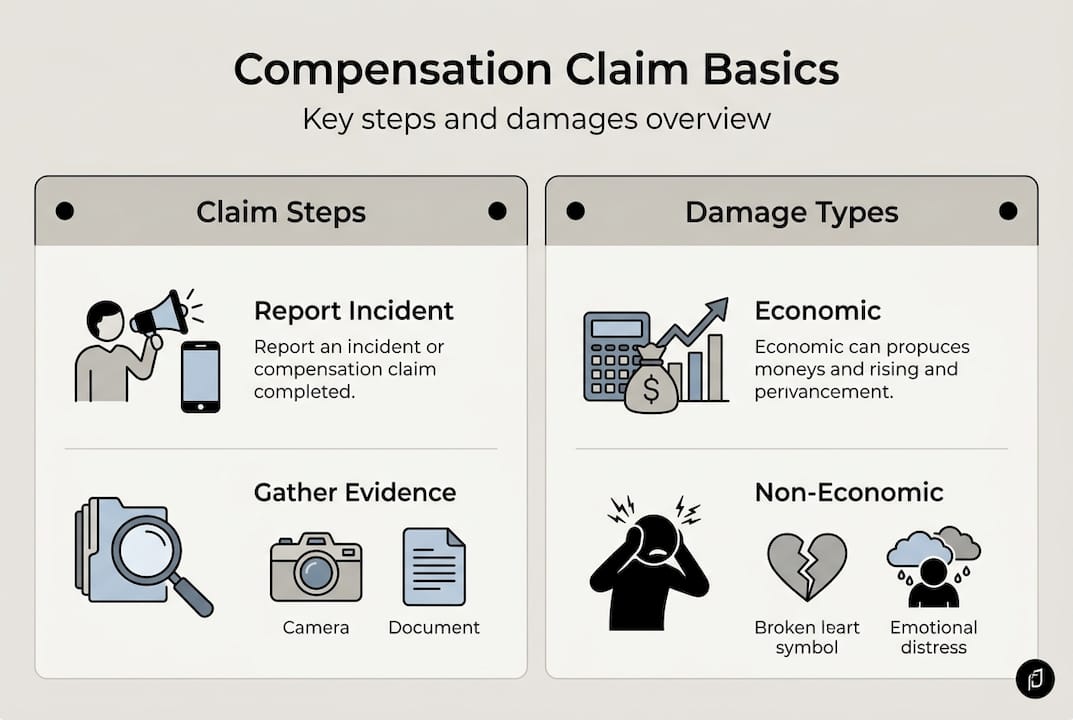

A compensation claim is a legal demand for financial restitution covering economic and non-economic damages caused by another party’s negligence. These claims arise when someone suffers personal injury or property damage due to actions or failures of an individual, business, or organisation that owed them a duty of care. The fundamental premise requires proving that negligence directly caused measurable losses, creating a legal right to seek monetary compensation.

Compensation claims encompass two primary damage categories. Economic damages represent quantifiable financial losses such as medical expenses, rehabilitation costs, lost wages, property repair bills, and replacement costs for damaged possessions. Non-economic damages address intangible losses including pain, suffering, emotional distress, loss of enjoyment of life, and permanent disability or disfigurement. The personal injury claims process requires documenting both categories thoroughly to maximise recovery.

Typical compensation claims involve diverse scenarios:

The basic legal conditions for pursuing a claim require establishing that the defendant owed you a duty of care, breached that duty through action or inaction, and directly caused losses you can demonstrate through evidence. For instance, a property owner who fails to repair a broken staircase breaches their duty to visitors, and if someone falls and breaks their leg, they can claim medical expenses, lost earnings during recovery, and compensation for pain and suffering.

Understanding these fundamentals helps you recognise when you have grounds for a claim and what evidence you need to gather. The personal injury litigation guide provides additional context on building strong cases that withstand scrutiny during negotiations or trial.

Understanding what compensation claims cover naturally leads to grasping how damages are calculated to know what you can realistically expect to claim. Calculation methods differ significantly between economic and non-economic damages, requiring distinct approaches to valuation and documentation.

Economic damages are calculated via bills and receipts that provide concrete evidence of financial losses. Medical expenses include hospital bills, prescription costs, physiotherapy sessions, and future treatment needs projected by medical professionals. Lost wages calculations use pay slips, tax returns, and employer statements to establish pre-injury earnings and multiply by time off work. Property damage claims total repair estimates from qualified assessors or replacement costs for items beyond economical repair, minus any applicable insurance deductible.

Non-economic damages prove more subjective, relying on two primary methods. The per diem approach assigns a daily rate to pain and suffering, multiplying it by recovery days. The multiplier method takes total economic damages and applies a factor between 1.5 and 5 based on injury severity, with catastrophic injuries commanding higher multipliers. Courts and insurers consider injury permanence, treatment duration, impact on daily activities, and psychological effects when determining appropriate multipliers.

Property damage claims follow straightforward valuation. Assessors inspect damage, obtain repair quotes from licensed contractors, and compare against pre-damage market value. If repair costs exceed replacement value, insurers typically offer replacement minus depreciation. Deductibles specified in insurance policies reduce final payouts, creating out-of-pocket expenses claimants can pursue from at-fault parties.

| Damage type | Calculation method | Example |

|---|---|---|

| Economic | Actual bills and receipts | £15,000 medical costs plus £8,000 lost wages |

| Non-economic | Per diem or multiplier | £23,000 economic damages × 3 multiplier = £69,000 |

| Property | Repair or replacement cost minus deductible | £4,500 repair estimate minus £500 deductible = £4,000 |

Pro Tip: Begin documenting every expense immediately after an incident, photographing damage, retaining all receipts, and maintaining detailed journals of pain levels and activity limitations. This contemporaneous evidence proves far more persuasive than reconstructed records months later, significantly strengthening your economic and non-economic damage claims. The personal injury law guide explores additional damages calculation methods that courts apply in complex cases.

With damage calculation understood, it becomes vital to recognise the legal hurdles and strategies that influence your compensation claim’s success. Even strong claims face obstacles that can reduce awards or derail cases entirely without proper preparation and representation.

Proving negligence requires showing duty, breach, causation, and harm. First, establish the defendant owed you a duty of care, which exists in most everyday situations like driving safely or maintaining safe premises. Second, demonstrate they breached that duty through action or inaction falling below reasonable standards. Third, prove causation linking the breach directly to your injuries, excluding pre-existing conditions or intervening factors. Fourth, show actual harm occurred, whether physical injury, property damage, or financial loss. Missing any element defeats your claim regardless of how sympathetic your situation appears.

Comparative fault systems complicate claims significantly. Comparative fault and damage caps affect compensation amounts when claimants share responsibility for incidents. Pure comparative fault jurisdictions reduce awards proportionally, so 30% claimant fault in a £100,000 claim yields £70,000. Modified comparative fault bars recovery if claimant fault exceeds 50% or 51%, depending on jurisdiction. Insurers aggressively argue plaintiff fault to reduce payouts, scrutinising every action before and during incidents.

Damage caps limit non-economic awards in some jurisdictions, particularly for medical negligence claims. These legislative limits can drastically reduce compensation for severe injuries causing permanent disability or disfigurement. Understanding applicable caps helps set realistic expectations and influences whether pursuing litigation proves worthwhile compared to settlement offers.

Insurers employ multiple tactics to minimise payouts:

Most claims settle pre-trial, with approximately 95% resolving through negotiation rather than courtroom battles. Strong documentation and legal representation prove crucial for achieving optimal outcomes. Represented claimants navigate complex procedures, counter insurer tactics effectively, and leverage litigation threats to secure fair settlement agreements.

Represented plaintiffs receive 3.5 times higher settlements than unrepresented claimants, demonstrating the substantial value professional advocacy brings to compensation claims.

Pro Tip: Consult a solicitor immediately after an incident, before providing recorded statements to insurers or accepting any settlement offers. Early legal advice prevents common mistakes like admitting fault, accepting inadequate compensation, or missing critical evidence preservation steps. Understanding comparative fault rules in your jurisdiction helps you assess realistic claim values and negotiation strategies.

Finally, we examine how to practically initiate and navigate your compensation claim in 2026, including what to expect and smart approaches that maximise success. Understanding the process demystifies what might seem overwhelming and helps you prepare effectively.

The typical claim process follows these stages:

Approximately 95% of claims settle before trial, making negotiation skills more valuable than courtroom prowess. Average settlement amounts vary dramatically by injury type, ranging from £2,000 for minor soft tissue injuries to £250,000 for severe permanent disabilities. Timelines span three months for straightforward cases to three years for complex litigation, with most settlements occurring within 12 to 18 months.

| Aspect | Settlement | Trial |

|---|---|---|

| Likelihood | 95% of cases | 5% of cases |

| Timeline | 6 to 18 months | 18 to 36 months |

| Control | Parties negotiate terms | Judge or jury decides |

| Costs | Lower legal fees | Substantial litigation expenses |

| Certainty | Guaranteed outcome | Unpredictable verdict risk |

| Privacy | Confidential agreements | Public court records |

No win no fee agreements, formally called conditional fee arrangements, allow claimants to pursue cases without upfront legal costs. Solicitors receive payment only upon successful settlement or verdict, taking their fee as a percentage of recovered damages plus a success fee. No win no fee risks include reduced net payout and potential liability for disbursements like expert witness fees or court costs if unsuccessful, though many solicitors offer insurance against such expenses.

Benefits include access to justice for those unable to afford hourly legal fees and solicitor motivation to maximise recovery since their payment depends on success. Drawbacks involve success fees reducing your net compensation by 25% to 40% and potential pressure to settle prematurely to secure payment. The personal injury claims guide explores these arrangements comprehensively.

Pro Tip: When choosing solicitors, compare success fee percentages, clarify whether you face disbursement liability if unsuccessful, and verify their track record in cases similar to yours. Prepare for your legal consultation by organising all evidence, listing questions, and understanding realistic timelines. Review personal injury law statistics and the no win no fee scheme details before committing to representation agreements.

Having understood the process and challenges, here is how Ali Legal can help you confidently pursue your compensation claim. Navigating compensation claims requires expertise in civil litigation and deep knowledge of personal injury law that transforms complex procedures into manageable steps.

Ali Legal offers expert support throughout the personal injury claims process, from initial case evaluation through settlement negotiation or trial representation. Our solicitors understand the tactics insurers employ to minimise payouts and counter them effectively with thorough evidence preparation, strategic negotiation, and litigation readiness when necessary. We provide transparent fixed fee structures and clear communication, ensuring you understand each development and decision point.

Professional legal representation significantly increases your compensation and navigates complex procedures that overwhelm unrepresented claimants. Our tailored advice addresses your specific circumstances, calculating realistic claim values, identifying all liable parties, and building compelling cases that withstand scrutiny. Discover how strategic case handling can maximise your claim’s success in 2026 by consulting with our experienced team.

A compensation claim qualifies when you suffer personal injury or property damage due to another party’s negligence, breach of duty, or intentional wrongdoing. You must demonstrate measurable losses, whether economic damages like medical bills or non-economic damages such as pain and suffering. The personal injury claims guide details specific qualifying scenarios.

Most compensation claims settle within 12 to 18 months, though straightforward cases may resolve in three to six months whilst complex litigation can extend beyond three years. Timeline factors include injury severity, liability disputes, negotiation willingness, and court scheduling if trial becomes necessary. Early legal consultation and thorough evidence gathering accelerate the process.

Success depends on proving negligence, demonstrating causation, and documenting damages convincingly. Approximately 95% of claims settle successfully before trial, though settlement amounts vary based on evidence strength and representation quality. Represented claimants achieve substantially higher recoveries than those proceeding alone, with professional advocacy increasing settlements by 3.5 times on average.

No win no fee arrangements provide access to justice without upfront costs, making them worthwhile for claimants unable to afford hourly legal fees. However, success fees reduce net compensation by 25% to 40%, and some agreements carry disbursement liability risks. Compare solicitor terms carefully, verify track records, and understand all potential costs before committing to conditional fee arrangements.

Proving negligence requires establishing four elements: the defendant owed you a duty of care, breached that duty through substandard actions or omissions, directly caused your injuries through that breach, and you suffered actual damages as a result. Gather evidence including accident reports, witness statements, photographs, medical records, and expert opinions that document each element convincingly.