Menu

Get Expert Legal Support Today

Contract disputes cost British businesses millions every year, often resulting from unclear or misunderstood contract terms. For small and medium business owners, the challenge goes far beyond paperwork—it is about protecting hard-earned assets and reputation. If you want to cut through confusion about contractual liability and confidently manage business agreements, this guide provides practical insight on where risks arise and how to address them.

Contractual liability represents a fundamental legal concept that establishes the obligations and potential financial responsibilities businesses face when entering into agreements. In the United Kingdom, contractual liability is a strict legal framework that determines when and how a party can be held responsible for breaching the terms of a contract. Theoretical analysis of contract law suggests this framework is grounded in the core principle that contracts are legally binding promises between parties.

At its essence, contractual liability means that when one party fails to fulfil their agreed obligations, they may be legally required to compensate the other party for any resulting losses or damages. This liability extends beyond simple monetary transactions and can include various forms of performance, delivery of goods or services, or adherence to specific contractual conditions. English contract law emphasises that these obligations are enforceable through court mechanisms, providing businesses with clear recourse when agreements are not honoured.

The scope of contractual liability is broad and encompasses multiple scenarios. Businesses can be held liable for direct breaches such as non-delivery of products, failure to complete services as specified, or violations of agreed payment terms. Additionally, liability can extend to indirect consequences arising from contractual failures, including financial losses, reputational damage, and potential legal costs associated with resolving disputes. Understanding these potential risks is crucial for UK businesses seeking to protect their interests and maintain robust commercial relationships.

Pro tip: Always consult a legal professional and thoroughly review contract terms before signing to understand the full extent of potential contractual liabilities and negotiate clauses that provide appropriate protections for your business.

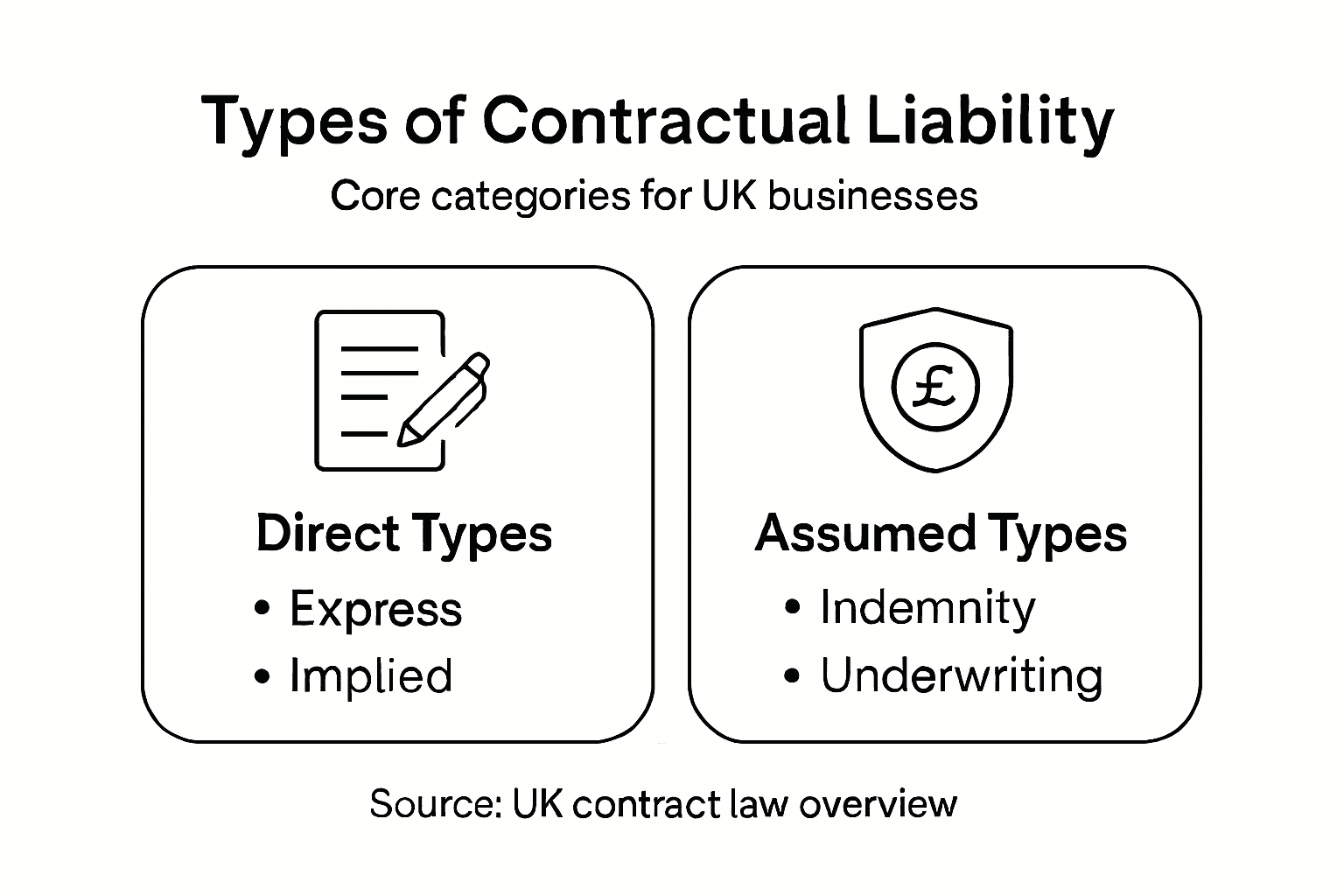

Contractual liability in the United Kingdom encompasses several distinct types that businesses must understand to effectively manage their legal risks. Distinct liability frameworks reveal that these types are not uniform but vary based on the specific nature of contractual agreements and potential breaches. The primary categories include express liability, implied liability, and assumed liability, each with unique characteristics and legal implications.

Express liability represents the most straightforward type, emerging directly from explicit terms written into a contract. These are clear, predetermined obligations that a party agrees to fulfil, such as delivering specific goods, completing defined services, or making precise financial payments. In contrast, implied liability arises from legal principles or industry standards not explicitly stated in the contract but understood to be part of the agreement. These can include expectations of reasonable performance, professional standards, or obligations derived from established business practices.

Contractual liability from an underwriting perspective highlights another crucial category: assumed liability. This occurs when a business voluntarily accepts responsibility for risks or potential damages that would not typically be their legal obligation. For instance, a contractor might assume liability for potential workplace accidents or equipment damage beyond their original contractual scope. Understanding these nuanced differences is critical for UK businesses to accurately assess their potential legal exposures and implement appropriate risk management strategies.

Pro tip: Consult with a legal professional to conduct a comprehensive review of your contractual documents, ensuring you fully understand the different liability types and potential risks embedded in your business agreements.

Here is a summary of the main types of contractual liability and how they differ in business contexts:

| Liability Type | Origin | Typical Example | Legal Implication |

|---|---|---|---|

| Express | Written contractual terms | Delivery date specified in contract | Direct and clearly enforceable |

| Implied | Law or standard business practices | Reasonable care expected from a supplier | Applied even if unwritten |

| Assumed | Voluntary addition by a party | Contractor takes on extra safety risks | May exceed normal obligations |

UK business contracts operate under a complex legal framework that governs contractual obligations and liability. Exclusion and limitation clauses play a critical role in defining the extent of potential legal responsibilities. The primary legislative instrument controlling these provisions is the Unfair Contract Terms Act 1977, which establishes crucial guidelines for how businesses can structure their contractual protections and limitations.

The key legislative framework encompasses several fundamental statutes that regulate contractual relationships. The Contracts (Rights of Third Parties) Act 1999 provides mechanisms for third parties to enforce contract terms, while the Sale of Goods Act 1979 and the Supply of Goods and Services Act 1982 establish baseline standards for commercial transactions. These laws collectively create a robust system that balances commercial flexibility with consumer and business protections, ensuring that contractual agreements maintain fairness and legal integrity.

Liability limitation provisions represent a critical aspect of UK contract law, allowing businesses to manage potential financial risks. Typical clauses include liability caps, which limit the maximum financial exposure in case of breach, and indemnity provisions that allocate specific risks between contracting parties. Courts carefully scrutinise these clauses to ensure they are reasonable, transparent, and do not unfairly disadvantage one party. Businesses must craft these provisions with precision, understanding that overly restrictive clauses may be deemed unenforceable if they contravene principles of fairness and reasonableness.

Pro tip: Engage a qualified legal professional to review your contract clauses, ensuring they comply with UK legislation and provide appropriate protection without creating undue legal vulnerabilities.

The following table outlines key legislative acts relevant to contractual liability in the UK:

| Legislation | Main Purpose | Typical Impact on Contracts |

|---|---|---|

| Unfair Contract Terms Act 1977 | Limits unfair contract exclusions | Protects against extreme liability limits |

| Sale of Goods Act 1979 | Sets standards for sale of goods | Ensures goods match description |

| Supply of Goods and Services Act 1982 | Regulates supply of services and goods | Guarantees reasonable care and skill |

| Contracts (Rights of Third Parties) Act 1999 | Grants rights to third parties | Allows non-signatories to enforce terms |

Businesses in the United Kingdom face complex legal obligations that directly influence their contractual risk exposure. Risk allocation strategies demonstrate that understanding and managing potential liabilities is crucial for maintaining financial stability and legal compliance. These obligations extend beyond simple contractual performance, encompassing broader responsibilities that can significantly impact a company’s operational and financial health.

The nature of business obligations varies depending on the specific type of contract and industry sector. Fundamental obligations include delivering agreed services or products, maintaining professional standards, ensuring workplace safety, and providing accurate representations of capabilities and potential outcomes. Companies must carefully assess their ability to fulfil contractual terms, as failure to meet these obligations can result in substantial financial penalties, legal disputes, and potential reputational damage. Contract law fundamentals emphasise the importance of clear, precise contractual language that explicitly defines these obligations and potential consequences of non-performance.

Risk exposure is particularly nuanced for UK businesses, with potential liabilities extending across multiple dimensions. Financial risks include direct contractual breach penalties, potential compensation claims, and indirect costs associated with dispute resolution. Legal risks involve potential litigation, regulatory penalties, and loss of business credibility. Businesses must develop comprehensive risk management strategies that include thorough contract reviews, appropriate insurance coverage, robust internal compliance mechanisms, and proactive legal consultation to mitigate these potential exposures.

Pro tip: Conduct regular internal audits of your contractual obligations and maintain comprehensive documentation to demonstrate your commitment to contractual performance and risk management.

Managing contractual liability is a critical strategic process for UK businesses seeking to protect their financial and legal interests. Liability limitation strategies provide essential frameworks for understanding and mitigating potential risks inherent in commercial agreements. These strategies involve carefully crafting contract terms that define and restrict potential financial exposure while maintaining fair and reasonable obligations between parties.

Businesses can implement several key approaches to minimise contractual liability risks. Risk allocation techniques involve precisely defining each party’s responsibilities, setting clear performance expectations, and establishing well-defined consequences for potential breaches. Appropriate contract selection plays a crucial role in this process, requiring businesses to thoroughly assess potential risks before finalising contractual agreements. This might include negotiating liability caps, implementing robust indemnification clauses, and ensuring comprehensive insurance coverage that aligns with potential contractual risks.

Effective risk management also demands proactive monitoring and periodic contract reviews. Businesses should develop internal processes for continuously evaluating their contractual obligations, identifying potential vulnerabilities, and updating agreements to reflect changing operational circumstances. This approach involves maintaining detailed documentation, conducting regular risk assessments, and seeking professional legal advice to ensure contractual terms remain protective and compliant with current legal standards.

Pro tip: Develop a comprehensive contract management system that includes regular legal reviews, risk assessments, and clear escalation procedures for potential contractual challenges.

Understanding contractual liability is essential for UK businesses aiming to minimise financial exposure and legal risks. Whether it involves managing express, implied, or assumed liabilities, the challenge lies in navigating complex obligations and ensuring contracts include effective limitation clauses that comply with UK legislation. Without expert guidance, businesses risk costly disputes, potential penalties, and damage to their reputation.

Ali Legal’s dedicated team offers practical solutions tailored to your needs. With a focus on clear communication, fixed fees, and long-term advising, we help you craft robust contracts and manage risk confidently. Explore our insights in our Uncategorized | Ali Legal section and see how strategic legal advice can safeguard your interests.

Don’t leave your business vulnerable to contractual pitfalls. Contact Ali Legal today and get fast, transparent, and strategic support to understand your liabilities and protect your commercial relationships. Reach out now through our contact page and take control of your contractual obligations.

Contractual liability is the legal responsibility of a party to fulfil the obligations defined in a contract. If a business fails to meet these obligations, it may be required to compensate the other party for any resulting losses or damages.

The primary types of contractual liability include express liability, which arises from explicitly stated terms in a contract; implied liability, which is derived from legal principles or established business practices; and assumed liability, where a party voluntarily takes on additional responsibilities beyond their original obligations.

Companies can manage their contractual liability risks by clearly defining each party’s responsibilities in contracts, negotiating liability caps and indemnification clauses, conducting regular contract reviews, and ensuring appropriate insurance coverage.

The consequences of breaching a contract can include financial penalties, claims for compensation, legal disputes, reputational damage, and potential regulatory penalties, depending on the nature of the breach and the applicable contractual terms.