Menu

Get Expert Legal Support Today

Starting a new business in the United Kingdom often comes with doubts about legal requirements and company set-up costs. Many entrepreneurs believe that registering a company is expensive or complicated, yet the truth is that company formation can be completed online within 24 hours, sometimes costing less than £50. Understanding this process helps you unlock legal protection, boost your business credibility, and avoid unnecessary compliance headaches as you grow.

Company formation is the legal process of establishing a business entity with distinct legal status in the United Kingdom. Incorporation creates a separate legal structure that protects individual owners from personal liability while providing businesses with enhanced credibility and operational flexibility.

Contrary to popular misconceptions, company formation is relatively straightforward in the UK. Here are some key characteristics of the process:

Many entrepreneurs hesitate due to widespread myths about complexity and expense. Company formation myths often discourage potential business owners from taking this important step. However, the reality is that incorporating a company has become increasingly accessible and user-friendly.

Company formation transforms a business from a simple trading activity into a recognised legal entity with structured governance and potential tax advantages.

The primary types of company structures in the UK include:

Pro tip: Before registering, conduct thorough research on which company structure best suits your specific business needs and long-term objectives.

The United Kingdom offers several distinct business structures that cater to different entrepreneurial needs and organisational objectives. Business structures vary in liability, governance, and operational complexity across multiple legal frameworks.

The primary company structures in the United Kingdom include:

Public Limited Companies differ significantly from private limited companies. These organisations can offer shares to the general public and must meet more stringent regulatory requirements, including higher transparency standards and minimum capital requirements.

Selecting the appropriate company structure represents a critical decision that impacts taxation, legal obligations, and future business growth potential.

The choice of company structure depends on several key considerations:

Company structure selection impacts fundamental business operations and should align with strategic organisational goals.

To clarify the differences and business implications of UK company structures, see the comparison below:

| Company Structure | Liability Protection | Fundraising Potential | Typical Use Case |

|---|---|---|---|

| Private Limited (Ltd) | Owners protected from debts | Limited to private investment | Small and medium enterprises |

| Public Limited (PLC) | Shareholders liable only for shares held | Can sell shares to public markets | Large companies seeking capital |

| Limited Liability Partnership (LLP) | Partners have limited liability | Not designed for equity fundraising | Professional services firms |

| Unlimited Company | No liability protection for owners | Minimal fundraising options | Niche or specialist businesses |

| Guarantee Company | Protection similar to Ltd | No share capital, relies on guarantees | Clubs, charities, non-profits |

Pro tip: Consult a legal professional to thoroughly evaluate which company structure best matches your specific business model and future aspirations.

Company registration in the United Kingdom involves a structured legal process designed to establish a business as a formal legal entity. Registering a company creates a distinct legal structure that provides entrepreneurs with essential legal protections and business credibility.

The key steps for company registration include:

Companies House offers multiple registration methods, with online registration being the most popular and efficient approach. The digital platform allows entrepreneurs to complete the entire process within 24 hours, typically costing £100 for online submissions.

Accurate and comprehensive documentation represents the cornerstone of successful company registration in the United Kingdom.

Crucial documentation required for registration encompasses:

Business registration establishes a separate legal entity recognised under UK law, offering significant advantages for entrepreneurs.

Pro tip: Prepare all required documentation thoroughly and double-check information before submission to prevent potential delays in the registration process.

Company directors in the United Kingdom shoulder significant legal obligations that extend far beyond basic management responsibilities. Directors have comprehensive legal duties that require careful navigation of complex regulatory landscapes.

The core responsibilities of company directors encompass several critical areas:

Financial and administrative responsibilities are particularly demanding. Directors must ensure meticulous record-keeping, timely financial reporting, and strict compliance with regulatory requirements. This includes preparing annual accounts, submitting confirmation statements, and maintaining transparent financial documentation.

A company director’s primary duty is to act in the best interests of the organisation, balancing legal compliance with strategic business objectives.

Specific legal obligations for directors include:

Company directors bear ultimate legal responsibility for their organisation’s performance and regulatory compliance, even when administrative tasks are delegated.

Pro tip: Maintain a comprehensive compliance calendar and consider professional legal advice to navigate the complex landscape of directorial responsibilities.

Company compliance involves navigating a complex landscape of financial and legal responsibilities that extend well beyond initial registration. Limited companies face substantial ongoing regulatory requirements that demand consistent attention and strategic management.

The primary ongoing costs and compliance considerations include:

Financial risks emerge from potential non-compliance, which can result in significant penalties, legal challenges, and potential director disqualification. Businesses must allocate resources for maintaining accurate documentation, filing timely reports, and ensuring transparent financial operations.

Proactive compliance management represents a critical investment in your company’s long-term sustainability and legal protection.

Key ongoing compliance obligations encompass:

Hidden compliance costs can significantly impact business budgeting and require careful financial planning.

For reference, here is a summary of essential compliance tasks and their business impact:

| Compliance Task | Frequency | Business Impact |

|---|---|---|

| Annual accounts submission | Once per year | Ensures financial transparency |

| Corporation tax reporting | Annually | Obligatory for HMRC compliance |

| Confirmation statement filing | Yearly | Maintains accurate public records |

| Statutory records maintenance | Continuous | Helps prevent legal disputes |

| PSC tracking | As changes occur | Demonstrates ownership transparency |

Pro tip: Create a comprehensive compliance calendar and budget for potential administrative expenses to prevent unexpected financial strain.

Starting a company in the United Kingdom involves important legal steps and ongoing compliance that can feel overwhelming. From choosing the right structure to understanding director responsibilities and maintaining continuous regulatory obligations, every element is crucial to protect your business and personal interests. Navigating these complexities demands clear advice, transparency, and a tailored approach that aligns with your long-term goals.

Ali Legal specialises in comprehensive corporate and commercial law services designed to guide you through every phase of company formation and compliance. We understand the emotional weight behind these decisions and offer fixed fees, straightforward advice, and a client-centric experience. By partnering with us, you gain access to knowledgeable solicitors dedicated to securing your business’s success and legal integrity.

Ready to take confident steps towards establishing or managing your UK company with professional legal support? Contact us today for a clear consultation that prioritises your needs. Visit Ali Legal Contact Us now to start your journey or explore our guidance on legal responsibilities for company directors and compliance strategies. Don’t let uncertainty delay your business ambitions — trust Ali Legal to make company formation fast and transparent.

Company formation is the legal process of establishing a business entity with distinct legal status, allowing the business to operate separately from its owners while providing liability protection and operational flexibility.

The company formation process can be completed online within 24 hours, provided all the necessary documentation is prepared and submitted correctly.

Key requirements for registering a company include selecting a company name, preparing necessary documentation, identifying directors and shareholders, defining articles of association, and submitting these to Companies House.

Company directors must ensure timely filing of annual accounts, pay Corporation Tax, maintain accurate company records, and comply with various statutory reporting requirements to avoid penalties and legal issues.

Every family facing uncertainty about their residency in the United Kingdom knows how confusing citizenship rules can seem. Understanding British citizenship law is vital for securing your place and unlocking your legal rights. The law shapes who can belong, how membership is granted, and what protection or benefits you have as a resident. This article offers clear guidance on the official pathways and requirements, making complex legal concepts easier to grasp for those seeking certainty about their future in the United Kingdom.

Citizenship law in the United Kingdom represents a complex legal framework that determines an individual’s membership, rights, and obligations within the national community. At its core, British citizenship establishes a fundamental legal relationship between a person and the state, defining who belongs and under what conditions.

The legal definition of citizenship encompasses several critical dimensions:

British citizenship can be acquired through multiple pathways, including:

Each pathway involves distinct eligibility criteria and procedural requirements. For instance, citizenship by birth is not automatically granted and depends on complex factors such as parental status, immigration history, and the specific period of birth.

Citizenship represents more than a legal document - it embodies belonging, identity, and participation in the national community.

The legal framework surrounding citizenship balances individual rights with the state’s sovereign authority to define membership. This means that while individuals may qualify for citizenship, the final decision remains within governmental discretion.

Naturalisation represents a particularly intricate process where immigrants can transition to full citizenship status. This typically requires:

The evolving nature of citizenship law reflects broader social and political transformations, adapting to changing migration patterns, international obligations, and domestic policy priorities.

Pro tip: Always consult official government resources and consider professional legal advice when navigating complex citizenship applications to ensure accurate understanding of your specific circumstances.

The United Kingdom offers several distinct types of British nationality, each with unique characteristics and legal implications. Understanding these variations is crucial for individuals navigating their legal status and potential rights within the British immigration system.

British Citizenship represents the most comprehensive form of national membership, providing the broadest range of rights. The primary types of British nationality include:

Each category reflects different historical, territorial, and legal connections to the United Kingdom, with varying levels of rights and protections.

Here is a summary comparison of key types of British nationality and their core benefits:

| Nationality Type | Right to Live in UK | Voting Rights | British Passport |

|---|---|---|---|

| British Citizen | Unlimited, unrestricted | Full national and local | Entitled |

| British Overseas Territories Citizen | Restricted to territories | None in the UK | Entitled |

| British Overseas Citizen | No automatic right | None | Entitled |

| British Subject | Limited (if right of abode) | None in the UK | Entitled |

| British National (Overseas) | No automatic right | None | Entitled |

| British Protected Person | No automatic right | None | Entitled |

Not all forms of British nationality offer the same entitlements, making careful distinction essential.

British Citizens enjoy the most extensive privileges, including:

Other categories like British Overseas Citizens have more limited rights, often stemming from historical colonial relationships. These status types emerged from the complex process of decolonisation, preserving legal connections with individuals from former British territories.

The nuanced landscape of British nationality reflects the nation’s intricate historical and legal evolution. Each type of citizenship represents a unique legal pathway, shaped by geopolitical changes and specific immigration policies.

Pro tip: Consult an immigration specialist to understand precisely which type of British nationality applies to your specific personal and familial circumstances.

The cornerstone of British nationality law is the British Nationality Act 1981, which establishes the comprehensive legal framework governing citizenship acquisition and rights in the United Kingdom. This foundational legislation defines the intricate pathways through which individuals can become British citizens.

The primary application routes for British citizenship include:

Citizenship is not merely a legal status, but a complex negotiation between individual circumstances and national policy.

Naturalisation represents the most common pathway for adults seeking British citizenship. The process involves rigorous eligibility criteria:

Each application route carries unique requirements and documentation challenges. Citizenship by registration offers alternative pathways for individuals with specific connections to the United Kingdom, such as children of British parents or individuals with historical territorial links.

The application process typically involves comprehensive documentation and verification by UK immigration authorities. Applicants must provide extensive personal history, linguistic evidence, and meet stringent character assessment standards.

Pro tip: Carefully document every aspect of your personal and professional history, and consider seeking professional legal guidance to navigate the complex citizenship application process.

British citizenship encompasses a comprehensive set of legal entitlements and societal responsibilities that define an individual’s relationship with the United Kingdom. Core citizenship rights extend far beyond mere legal documentation, representing a fundamental connection to national identity and civic participation.

The primary rights of British citizens include:

Citizenship is a dynamic contract between the individual and the state, balancing privileges with collective responsibilities.

Civic Obligations represent the reciprocal commitments citizens make to their society:

Beyond legal frameworks, citizenship embodies a deeper sense of belonging. The right of abode allows British citizens complete freedom to enter, live, and work in the United Kingdom without immigration restrictions. This fundamental right distinguishes citizens from other residency statuses.

Citizens also bear significant responsibilities in maintaining the social fabric. Good character remains a crucial aspect of citizenship, particularly during naturalisation processes and ongoing civic engagement.

Pro tip: Maintain comprehensive documentation of your civic contributions and legal compliance to support your standing as a responsible British citizen.

Navigating the path to British citizenship involves confronting several significant financial and procedural challenges. The journey is complex, with multiple potential obstacles that can deter even the most determined applicants.

Key financial hurdles include:

The financial burden of citizenship applications can be substantial, often creating systemic barriers for vulnerable migrants.

The primary cost components of citizenship applications typically involve:

Citizenship requirements extend beyond mere financial considerations. Applicants must demonstrate:

Migrant communities face disproportionate challenges in navigating these complex requirements. Low-income individuals often find the cumulative costs and stringent criteria particularly prohibitive.

Additional hidden expenses can include professional document preparation, potential legal advice, and multiple test attempts. Some applicants might require multiple applications, further increasing the financial strain.

Here’s a concise overview of common citizenship application costs and practical strategies:

| Expense Category | Typical Amount | Suggested Mitigation |

|---|---|---|

| Application Fee | £1,330 (approximate) | Budget in advance |

| Language Test | £150–£200 | Prepare thoroughly to avoid retakes |

| Document Translation | £50–£200 per document | Use certified translators only |

| Legal Assistance | £500–£2,000 | Seek free legal clinics or advice |

| Biometric Registration | £20–£50 | Check if included in main fee |

Pro tip: Begin saving and preparing documentation early, and explore potential fee waivers or reduced-cost support programmes to manage citizenship application expenses.

Understanding British citizenship law involves complex terms like naturalisation, registration, and right of abode that can be overwhelming and daunting. If you are facing challenges such as meeting residency requirements, passing language tests, or managing the high costs linked to citizenship applications then you do not have to face these hurdles alone. Ali Legal specialises in providing clear and strategic legal solutions tailored to your personal circumstances. Our transparent approach emphasises fixed fees and straightforward advice ensuring you stay informed every step of the way.

Explore our comprehensive legal services on All | Ali Legal to find immigration support and more. Take control of your citizenship journey now and benefit from expert guidance designed to simplify application routes and protect your rights. Contact us today at https://alilegal.co.uk/contact-us and let Ali Legal help turn complex citizenship law into clear pathways forward.

Citizenship law in the UK is a complex legal framework that outlines the rights, obligations, and paths to legal membership in the national community, determining who can be classified as a British citizen.

British citizenship can be acquired through several pathways, including birth within the UK, descent from British parents, naturalisation, and registration under specific legal provisions.

British citizens enjoy various rights, including the unrestricted right to live and work in the UK, eligibility to vote in national elections, and access to public services and social welfare.

Common challenges include high application fees, costs for language tests and document translations, complex procedures, and stringent eligibility criteria that can create barriers for applicants.

Running a business in the United Kingdom often means grappling with changing regulations, complex contracts, and evolving legal obligations. The risks can lead not only to financial losses but also threaten your reputation and asset security. By understanding the essentials of legal risk management and implementing strategic frameworks for compliance and protection, you can build a resilient foundation that helps your organisation avoid costly mistakes and maintain integrity.

Legal risk management represents a strategic approach organisations use to identify, assess, and mitigate potential legal challenges before they escalate into significant problems. For UK businesses, this process involves systematically evaluating potential legal vulnerabilities across multiple operational domains.

At its core, legal risk management encompasses several critical components:

Understanding legal risk requires businesses to recognise that risks are not merely about avoiding litigation, but about protecting organisational integrity through structured approaches. These approaches involve carefully mapping potential legal challenges that could disrupt business operations, damage reputation, or result in financial penalties.

Companies must develop robust frameworks that anticipate potential legal complications. This involves creating systematic processes for ongoing legal assessment, which includes regular review of contracts, understanding current regulatory requirements, and maintaining comprehensive documentation of all potential risk areas.

Typical Legal Risk Categories Include:

Pro tip: Conduct a comprehensive legal risk audit annually to proactively identify and address potential vulnerabilities before they become significant challenges.

UK businesses face a complex landscape of potential legal risks that can significantly impact their operations and financial stability. Key legal risks span multiple operational domains, requiring strategic awareness and proactive management.

The primary categories of legal risks businesses must navigate include:

The following table compares the impact of key legal risk categories on UK businesses:

| Legal Risk Category | Typical Impact on Business | Example Scenario |

|---|---|---|

| Contractual | Financial losses, disputes | Unclear contract terms cause claims |

| Regulatory Compliance | Fines, operational restrictions | Missed legislative change leads to penalties |

| Employment Law | HR disputes, tribunal claims | Staff grievance mishandled |

| Intellectual Property | Loss of innovation, reputation | Patent infringement by competitor |

| Data Protection | Regulatory fines, data breaches | Customer information exposed |

Contractual risks represent one of the most prevalent challenges for organisations. These risks emerge from poorly drafted contracts, ambiguous terms, or failure to fully understand contractual obligations. Comprehensive contract management strategies can help mitigate potential disputes and financial exposure.

Moreover, regulatory compliance risks continue to evolve, with businesses facing increasing scrutiny across various sectors. This requires maintaining up-to-date knowledge of legislative changes, implementing robust internal compliance mechanisms, and regularly reviewing organisational practices to ensure alignment with current legal standards.

Legal risks are not static; they represent dynamic challenges that demand continuous monitoring and strategic adaptation.

Common Sources of Legal Vulnerability:

Pro tip: Develop a comprehensive legal risk register that systematically tracks and evaluates potential legal vulnerabilities across all operational domains.

Legal risk assessment represents a systematic approach that enables businesses to identify, evaluate, and proactively manage potential legal vulnerabilities. Comprehensive risk assessment frameworks provide organisations with strategic tools to understand and mitigate potential legal challenges.

The legal risk assessment process typically involves several critical stages:

Effective risk assessment requires a multi-dimensional approach. Businesses must consider various factors, including the specific nature of their industry, regulatory environment, operational complexities, and potential legal exposure. This involves conducting thorough internal audits, reviewing existing contracts, and analysing potential areas of legal vulnerability.

Key Components of Legal Risk Assessment:

Legal risk assessment is not a one-time event, but a continuous process of strategic evaluation and adaptation.

Mitigation strategies must be tailored to each organisation’s unique risk profile. This involves developing robust internal policies, implementing comprehensive training programmes, and creating clear protocols for managing potential legal challenges.

Pro tip: Conduct a quarterly legal risk assessment that involves cross-departmental collaboration to ensure a holistic approach to identifying and managing potential legal vulnerabilities.

Navigating the complex landscape of UK legal frameworks requires businesses to develop a comprehensive understanding of regulatory obligations. Comprehensive business regulation guidance provides critical insights into maintaining legal compliance across various operational domains.

The primary legal frameworks that UK businesses must understand include:

Compliance is not a static concept but a dynamic process requiring continuous adaptation. Businesses must remain vigilant about evolving legal requirements, implementing robust internal mechanisms to track and respond to regulatory changes. This involves establishing dedicated compliance teams, conducting regular training programmes, and maintaining meticulous documentation of organisational practices.

Key Compliance Strategy Components:

Effective compliance is about understanding the spirit of the law, not just its letter.

Organisations must develop a proactive approach to compliance, integrating legal requirements into their core operational strategies. This means going beyond mere technical adherence and cultivating a culture of ethical and responsible business practices.

Pro tip: Develop a dedicated compliance calendar that tracks upcoming regulatory changes and schedules regular internal reviews to ensure ongoing legal alignment.

Legal risk management demands a proactive approach to identifying and mitigating potential organisational vulnerabilities. Businesses frequently encounter several recurring challenges that can significantly impact their legal and operational stability.

The most prevalent legal risk management pitfalls include:

Small and medium-sized enterprises are particularly susceptible to legal vulnerabilities due to limited resources and complex regulatory landscapes. Many organisations struggle with developing robust risk management frameworks that can effectively anticipate and mitigate potential legal challenges.

Critical Prevention Strategies:

Here is a summary of prevention strategies and their benefits for legal risk management:

| Prevention Strategy | Benefit for Organisations | Example Outcome |

|---|---|---|

| Legal training programmes | Improved staff legal awareness | Fewer inadvertent policy breaches |

| Regular compliance audits | Early risk detection | Issues addressed before penalties arise |

| Systematic documentation processes | Evidence in disputes | Quick retrieval during investigations |

| Clear risk communication channels | Faster escalation of issues | Prompt action on legal concerns |

| Ongoing expert consultation | Updated compliance knowledge | Adaptation to new regulations |

Legal risk prevention is not about eliminating all risks, but about managing them intelligently and strategically.

Successful prevention requires a cultural shift within organisations, transforming legal compliance from a bureaucratic requirement to a strategic business priority. This involves creating an environment where every team member understands their role in maintaining legal integrity.

Pro tip: Develop a standardised risk reporting template that enables consistent, clear communication of potential legal vulnerabilities across all organisational levels.

Navigating the complexities of legal risk management is essential for safeguarding your UK business from costly disputes, compliance breaches, and reputational damage. This article highlights critical challenges such as contractual risks, regulatory compliance, and evolving data protection laws that demand your immediate attention. Key goals for any organisation include proactive legal assessment, strategic risk mitigation, and maintaining robust internal compliance.

At Ali Legal, we understand these pain points and offer tailored legal solutions designed to help you build a resilient framework. Whether you need assistance with contract drafting, compliance audits or ongoing risk evaluation, our team delivers straightforward advice with transparency and speed. Explore our comprehensive insights and resources in Uncategorized | Ali Legal to deepen your understanding.

Ready to take control of your legal risks before they escalate? Connect with our expert solicitors today for a clear, strategic approach that protects your business integrity. Visit Ali Legal Contact Us now and secure your business future with confidence.

Legal risk management is a strategic approach that organisations use to identify, assess, and mitigate potential legal challenges before they escalate into significant problems. It involves proactive legal assessments, compliance monitoring, risk mitigation planning, and regular legal audits.

Typical categories of legal risks include contractual risks, regulatory compliance risks, employment law risks, intellectual property risks, and data protection and privacy risks. Each category has its unique impact on business operations and financial stability.

Businesses can conduct an effective legal risk assessment by identifying potential risks, evaluating their likelihood and impact, developing targeted mitigation strategies, continuously monitoring risks, and maintaining comprehensive documentation of the assessment process.

Compliance is crucial in legal risk management as it ensures that businesses adhere to relevant laws and regulations. This proactive approach helps prevent legal disputes, financial penalties, and reputational damage, thus safeguarding the organisation’s integrity and sustainability.

A well-structured estate plan is one of the most powerful tools for protecting family wealth and passing on your legacy with confidence. Without thoughtful preparation, even sizeable assets can quickly become entangled in legal uncertainty and unnecessary disputes. This article cuts through misconceptions and highlights why comprehensive estate planning is vital for every high-net-worth family in the United Kingdom, providing clear, practical steps to secure your assets and support your loved ones.

Estate planning represents a strategic approach to managing and preserving family wealth after an individual’s death. At its core, estate planning involves making critical legal arrangements to ensure your assets are distributed according to your specific wishes, minimising potential tax liabilities and potential family conflicts.

Understanding estate planning requires dispelling several common myths. Many people mistakenly believe that estate planning is only for wealthy individuals, when in reality, comprehensive estate management is crucial for families across different financial backgrounds. The process involves more than simply drafting a will - it encompasses detailed considerations about asset distribution, potential inheritance tax implications, and protecting vulnerable family members.

Key components of effective estate planning include:

Contrary to popular belief, estate planning is not a one-time event but an ongoing process that requires periodic review and adjustment. Life changes such as marriage, divorce, birth of children, or significant financial shifts necessitate updating estate planning documents to ensure they remain current and reflective of your intentions.

Pro tip: Consult a legal professional annually to review and update your estate planning documents, ensuring they accurately represent your current financial situation and family circumstances.

Estate planning involves three critical legal instruments that provide comprehensive protection for individuals and their families: wills, trusts, and powers of attorney. Each plays a unique role in managing and protecting assets, ensuring that an individual’s wishes are respected and financial interests are safeguarded throughout different life stages.

Wills represent the foundational document in estate planning, legally dictating how personal assets will be distributed after death. These legal documents are crucial for preventing potential family disputes and ensuring that specific wishes are legally recognised. Without a properly drafted will, assets may be distributed according to standard inheritance laws, which might not align with an individual’s intentions.

Key considerations for effective estate planning include:

Trusts offer an additional layer of financial protection and flexibility. They enable individuals to set specific conditions for asset distribution, potentially reducing inheritance tax liabilities and providing structured financial support for beneficiaries. Different types of trusts can be established to address various family and financial scenarios, from protecting vulnerable family members to managing complex asset portfolios.

Lasting Powers of Attorney (LPA) are another essential component of comprehensive estate planning. These legal arrangements allow trusted individuals to make critical decisions on one’s behalf if mental capacity is compromised. There are two primary types of LPA in the UK: one for health and welfare decisions, and another for property and financial affairs.

Professional legal guidance is essential when establishing these complex legal instruments to ensure they accurately reflect your intentions and provide maximum protection.

Pro tip: Consult a qualified legal professional who specialises in estate planning to create a comprehensive strategy tailored to your unique family and financial circumstances.

To clarify the main legal tools, here is a comparison of wills, trusts, and lasting powers of attorney:

| Instrument | Primary Purpose | Typical Use Case |

|---|---|---|

| Will | Directs distribution of estate assets | Outlining beneficiaries and executors |

| Trust | Manages assets with set conditions | Protecting minors, reducing tax |

| Lasting Power of Attorney | Delegates decision-making authority | Managing affairs if incapacitated |

Estate planning in the United Kingdom is governed by a complex legal framework that significantly influences how individuals can manage and distribute their assets. These laws provide critical guidelines that determine inheritance rights, tax implications, and the overall process of asset transfer upon an individual’s death.

One of the most fundamental legal considerations is the intestacy rules governing estate distribution. When an individual dies without a valid will, these statutory regulations determine how assets are allocated among surviving family members. The hierarchy of inheritance follows a strict legal protocol, prioritising spouses, civil partners, and direct descendants.

Key legal aspects affecting estate planning include:

The Inheritance and Trustees’ Powers Act 2014 introduced significant changes to how estates are managed. This legislation modified previous inheritance laws, particularly regarding the rights of spouses and civil partners. For instance, the Act altered the distribution of assets when someone dies without a will, ensuring more equitable treatment of surviving partners and children.

Legal frameworks are dynamic, with periodic legislative updates significantly impacting estate planning strategies.

Understanding these legal intricacies requires careful navigation of complex statutory requirements. Different rules apply depending on whether an individual is domiciled in England, Wales, Scotland, or Northern Ireland, adding another layer of complexity to estate planning decisions.

Pro tip: Consult a specialised legal professional who can provide up-to-date guidance on the latest legislative changes affecting estate planning in your specific region.

Inheritance Tax (IHT) represents a critical financial consideration for individuals engaged in comprehensive estate planning across the United Kingdom. This complex taxation mechanism directly impacts how families preserve and transfer wealth, requiring strategic financial management and proactive planning.

The current UK tax framework establishes specific inheritance tax thresholds and regulations that significantly influence estate planning strategies. Typically, estates valued above £325,000 are subject to a 40% tax rate, though numerous exemptions and allowances can help mitigate this substantial financial burden.

Key financial considerations in inheritance tax planning include:

Nil-Rate Band and Residence Nil-Rate Band provide crucial mechanisms for reducing inheritance tax liability. The standard nil-rate band allows individuals to pass on £325,000 tax-free, with an additional residence nil-rate band of £175,000 when passing a primary residence to direct descendants. This means married couples can potentially shield up to £1 million from inheritance tax through careful planning.

Below is a summary of key inheritance tax thresholds and benefits available in the UK:

| Allowance Type | 2024/25 Value | Who Benefits |

|---|---|---|

| Nil-rate band | £325,000 | All UK estate owners |

| Residence nil-rate band | £175,000 | Passing home to descendants |

| Combined spouse benefit | Up to £1 million total | Married couples or civil partners |

Proactive estate planning can significantly reduce inheritance tax liabilities, preserving more wealth for future generations.

Complex estates require sophisticated financial strategies, including lifetime gifting, establishing trusts, and leveraging various tax relief mechanisms. Professional financial advice becomes essential in navigating these intricate regulations and developing a comprehensive wealth preservation approach.

Pro tip: Conduct a comprehensive estate valuation and consult a tax specialist annually to optimise your inheritance tax strategy and maximise potential exemptions.

Estate planning requires meticulous attention to detail, with numerous potential missteps that can significantly compromise the intended distribution of family wealth. Navigating these complex legal and financial landscapes demands strategic foresight and comprehensive understanding of potential risks.

One of the most critical errors individuals make is failing to create a legally valid will. Without a properly constructed legal document, assets may be distributed according to standard intestacy rules, potentially contradicting an individual’s genuine wishes and causing unnecessary familial conflict.

Common estate planning pitfalls include:

Incomplete Documentation represents another significant risk in estate planning. Many individuals mistakenly believe that verbal agreements or informal arrangements will suffice, when in reality, legally binding documentation is crucial for ensuring precise asset transfer and minimising potential disputes among beneficiaries.

Professional legal guidance can help prevent costly mistakes and ensure comprehensive estate protection.

Complex family structures and changing life circumstances further complicate estate planning. Marriages, divorces, births, and significant financial changes necessitate regular document reviews and updates to maintain the relevance and effectiveness of estate planning strategies.

Pro tip: Schedule an annual comprehensive review of your estate planning documents with a legal professional to ensure they remain current and accurately reflect your intentions.

Estate planning can feel overwhelming especially with complex laws and tax implications that threaten your family’s financial future. Whether you are navigating wills, trusts, or inheritance tax strategies, Ali Legal understands the challenges you face in securing your assets and ensuring your intentions are respected. From drafting clear and legally binding documents to managing lasting powers of attorney, our client-centred approach provides transparent, straightforward advice with fixed fees and speedy solutions.

Take control of your estate with confidence today. Visit Ali Legal to access expert legal support tailored to your unique situation. Don’t leave your family’s wealth to chance – contact us now to start your personalised estate planning journey and safeguard your legacy with trusted professionals dedicated to clarity and long-term care.

Estate planning is a strategic approach to managing and preserving family wealth after an individual’s death. It ensures that assets are distributed according to your wishes, minimises tax liabilities, and helps prevent family conflicts.

Key components include drafting a legally binding will, identifying and valuing personal assets, considering inheritance tax strategies, establishing trusts for specific beneficiaries, and designating a power of attorney.

Estate planning is an ongoing process, so it’s advisable to review and update your documents annually or after significant life changes, such as marriage, divorce, or the birth of children, to ensure they reflect your current circumstances.

A will directs the distribution of estate assets after death, a trust manages assets under certain conditions possibly reducing tax liabilities, and a lasting power of attorney allows trusted individuals to make decisions on your behalf if you become incapacitated.

Running a UK SME can quickly become overwhelming when faced with legal responsibilities and tough regulatory choices. Every decision, from company structure to record-keeping and compliance, shapes your firm’s future and risk profile. Knowing what is required – and when – can help you avoid costly mistakes and safeguard your business in the long run.

This guide reveals the most important legal tips every UK SME needs to operate smoothly and meet government expectations. You will discover practical steps for tackling crucial tasks like statutory filings, record maintenance, and selecting the best structure for your goals.

Get ready to uncover clear, actionable advice that can help you protect your company and boost your confidence in handling legal duties. The strategies you find here will lay the groundwork for stronger compliance and long-term business success.

Selecting the right legal structure is a fundamental decision that can significantly impact your UK small or medium enterprise (SME). The structure you choose determines everything from tax obligations to personal liability and operational flexibility.

Understanding the key legal structures available in the United Kingdom is crucial for making an informed choice. The most common options include:

When selecting a legal structure, consider critical factors such as business complexity, growth potential, and financial risk. Comprehensive corporate governance guidelines from Companies House provide valuable insights into these considerations.

Your chosen legal structure will define how you operate, raise capital, and manage legal responsibilities.

Each structure offers unique advantages and challenges. A sole trader structure works well for small, low-risk businesses with minimal complexity. In contrast, a limited company provides stronger legal protection and potential tax efficiencies for growing enterprises.

Key considerations when choosing your legal structure include:

Pro tip: Consult a legal professional to assess your specific business needs and select the most appropriate legal structure for your SME’s unique circumstances.

Statutory filings are the backbone of legal compliance for UK SMEs. Maintaining accurate and timely records is not just a legal requirement but a critical aspect of professional business management.

Companies in the United Kingdom are legally obligated to submit various documents to Companies House within specific timeframes. Regulatory compliance requirements cover multiple essential submissions including:

The consequences of missing these statutory filing deadlines can be severe. Penalties may include:

Timely and accurate statutory filing is not optional it is a fundamental legal responsibility for UK businesses.

Proactive compliance requires establishing robust systems and processes. This means creating internal tracking mechanisms to monitor upcoming filing deadlines and ensuring all required documentation is prepared well in advance.

The recent changes to UK company law have further emphasised the importance of accurate company information submission, with enhanced monitoring and stricter penalties for non-compliance.

Pro tip: Invest in digital filing management tools or work with a professional accountant to streamline your statutory filing process and avoid potential compliance pitfalls.

Accurate company records and minutes are the foundation of good corporate governance for UK SMEs. These documents serve as a critical legal and historical record of your business’s key decisions and activities.

Official record-keeping guidelines require businesses to maintain comprehensive documentation that demonstrates transparency and accountability. The essential records every UK company must maintain include:

Maintaining these records is not just a legal requirement but a strategic practice that provides multiple benefits:

Accurate record-keeping is the backbone of corporate integrity and legal protection.

Digital record management has transformed how SMEs approach documentation. Modern businesses can leverage online platforms to update company information efficiently and maintain real-time compliance.

Key considerations for effective record management include implementing robust digital filing systems establishing clear document retention policies and training staff on proper record-keeping protocols.

Pro tip: Invest in a secure digital document management system that automatically timestamps and archives your company records ensuring easy retrieval and maintaining a comprehensive audit trail.

Contracts and agreements form the legal backbone of business relationships for UK SMEs. Properly drafted documents protect your company’s interests and provide clear guidelines for all business interactions.

Contract preparation guidelines emphasise the critical importance of comprehensive documentation that addresses potential scenarios and mitigates legal risks. Every SME should focus on creating robust agreements that cover key business relationships.

Essential types of contracts for UK SMEs include:

Key considerations when drafting business contracts:

A well-drafted contract is your best defence against potential legal disputes and misunderstandings.

The legal framework surrounding company agreements requires meticulous attention to detail. Each document should be tailored to your specific business needs while maintaining legal precision.

Understanding the nuanced requirements of commercial contract drafting can help SMEs protect their interests and establish clear operational boundaries.

Pro tip: Consider engaging a legal professional to review your contracts periodically and ensure they remain current with changing business regulations and company circumstances.

Directors of UK SMEs carry significant legal responsibilities that extend far beyond day-to-day business management. Understanding and monitoring these duties is crucial to protecting both the company and personal interests.

Director responsibilities under UK law encompass a comprehensive range of legal and ethical obligations that require careful navigation and proactive management.

Key statutory duties for company directors include:

Potential personal liabilities directors may face:

Directors are legally bound to act in the best interests of their company at all times.

The corporate governance framework requires directors to demonstrate transparency accountability and ethical decision making. UK Corporate Governance standards provide comprehensive guidance on managing these responsibilities effectively.

Strategic approaches to managing director duties include regular legal training ongoing compliance reviews and maintaining comprehensive documentation of key business decisions.

Pro tip: Conduct quarterly internal reviews of director activities and consider professional legal advice to ensure continuous compliance with evolving corporate governance requirements.

Data protection is no longer an optional extra for UK SMEs but a critical legal requirement that demands comprehensive and proactive management. Your organisation’s approach to personal data handling can significantly impact its reputation and legal standing.

Data protection guidance from the Information Commissioner’s Office highlights the essential elements of robust privacy policies.

Key components of effective data protection policies include:

Critical legal considerations for SMEs:

Privacy is not just a legal requirement it is a fundamental business trust mechanism.

The UK GDPR framework requires businesses to demonstrate active data protection management. This means going beyond simple compliance to creating a culture of privacy awareness.

Lawful basis interactive guidance provides SMEs with practical tools to navigate complex data protection requirements.

Effective implementation involves regular staff training comprehensive documentation and proactive risk management strategies.

Pro tip: Conduct an annual comprehensive privacy policy review and invest in staff data protection training to ensure ongoing compliance and reduce potential legal risks.

Making significant business decisions without professional legal guidance can expose your UK SME to substantial risks and potential financial consequences. Proactive legal consultation is an investment in your company’s future stability and strategic growth.

Critical business scenarios requiring legal consultation include:

Key reasons to seek professional legal advice:

Legal advice is not an expense it is a strategic safeguard for your business.

Understanding the nuanced legal landscape requires expertise that goes beyond general business knowledge. Legal consultation preparation involves comprehensive review of your specific business context and potential implications.

Effective legal consultation requires transparent communication detailed documentation and a willingness to explore multiple perspectives before making critical decisions.

Professional solicitors can provide:

Pro tip: Schedule legal consultations early in your decision making process and prepare comprehensive documentation to maximise the value of professional legal advice.

Below is a comprehensive table summarising the main points and strategies discussed throughout the article regarding legal considerations for UK SMEs.

| Topic | Key Details | Significance |

|---|---|---|

| Choosing a Legal Structure | Explore options: Sole Trader, Partnership, Limited Company, LLP. Assess factors like liability and tax implications. | Determines operations and compliance demands. |

| Ensuring Statutory Compliance | Submit accurate Company accounts and other filings timely as per Companies House requirements. | Avoid financial penalties and maintain legal standing. |

| Maintaining Company Records | Sustain detailed documentation such as financial statements and meeting minutes. | Encourages transparency and aligns with governance standards. |

| Drafting Contracts | Include precise terms in contracts (employment, suppliers, etc.) to safeguard interests. | Minimises disputes and clarifies obligations. |

| Director Responsibilities | Adhere to statutory duties and maintain integrity in decision-making. | Prevents legal repercussions and upholds corporate governance. |

| Data Protection Management | Implement secure, transparent data handling policies aligned with the GDPR. | Upholds trust and avoids legal penalties. |

| Seeking Legal Advice | Consult professionals during significant business changes for informed decisions. | Supports strategic planning and risk mitigation. |

Navigating the complex dos and don’ts of corporate law can feel daunting for any UK SME owner. From choosing the right legal structure to ensuring compliance with statutory filings and monitoring director duties, the challenges are many. If you want to avoid costly legal pitfalls and confidently secure your business’s future, understanding these key responsibilities is essential. Common pain points include managing contracts correctly, maintaining accurate company records, and implementing robust data protection policies—all critical for long-term success.

Do not leave your SME vulnerable. Visit Ali Legal to access straightforward advice tailored to your business needs. Explore our comprehensive legal services in Uncategorized | Ali Legal and our complete range at All | Ali Legal for expert guidance. Take the decisive step now and consult with an experienced solicitor who can help you implement effective corporate governance and compliance strategies immediately.

Choosing the right legal structure is crucial for your UK SME. Consider factors like personal liability, tax implications, and growth potential. Evaluate options such as Sole Trader, Partnership, Limited Company, and Limited Liability Partnership to find the best fit for your business goals.

To ensure compliance, maintain an organised filing system for all required documents, such as annual accounts and confirmation statements. Set up reminders for submission deadlines to complete filings on time and avoid penalties.

Your UK SME must maintain comprehensive records, including registers of members, accounting records, and minutes of board meetings. Establish a routine to regularly review and update these documents to ensure compliance and transparency.

Look to seek legal advice before making major changes, such as corporate restructuring or entering significant contracts. Engaging a legal professional early can help you identify potential risks and safeguard your company’s interests.

Directors must fulfil statutory duties, including promoting the company’s success and avoiding conflicts of interest. Regularly review director activities to ensure compliance with these responsibilities and maintain good corporate governance.

To implement effective data protection policies, establish clear consent mechanisms and secure data storage protocols. Conduct regular training sessions for staff on data handling to ensure everyone understands their responsibilities in protecting personal data.

Operational challenges and shifting market demands often push mid-sized companies in the United Kingdom to rethink their structure. For executives and legal leaders, choosing the right approach means balancing business resilience with strict regulatory standards. This introduction breaks down the Corporate Insolvency and Governance Act 2020, key restructuring mechanisms, and strategic options to help British companies take confident, compliant steps toward renewed efficiency.

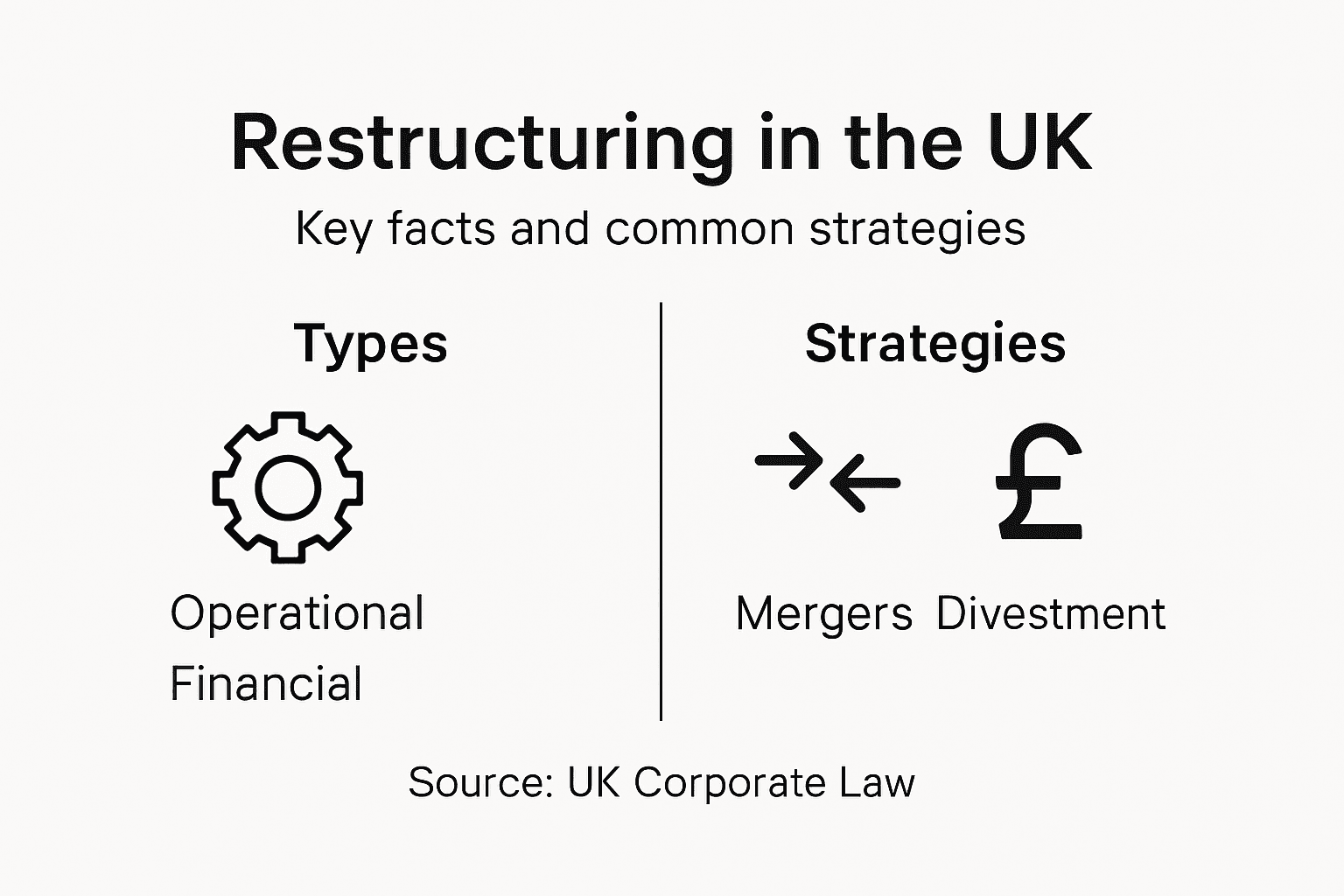

Corporate restructuring represents a strategic process through which businesses reorganise their operational, financial, and legal frameworks to enhance performance, mitigate risks, and adapt to changing market conditions. In the United Kingdom, this complex procedure involves multiple legal mechanisms designed to support corporate transformation and financial resilience.

The landscape of corporate restructuring in the UK has been significantly reshaped by recent legislative developments, particularly the Corporate Insolvency and Governance Act 2020. This legislation introduced several critical restructuring tools for businesses facing financial challenges:

Businesses typically pursue restructuring for several strategic reasons:

Corporate restructuring is not about survival, but strategic transformation.

The process involves comprehensive assessment of a company’s current state, identifying potential structural modifications, and implementing carefully planned changes across financial, operational, and organisational dimensions.

Pro tip: Engage experienced legal and financial professionals early in your restructuring journey to navigate complex regulatory requirements and minimise potential risks.

Corporate restructuring encompasses a diverse range of strategic approaches designed to transform and optimise business operations. Corporate restructuring strategies in the United Kingdom involve multifaceted processes that address financial, legal, and organisational dimensions of a company’s structure.

The primary types of corporate restructuring can be categorised into several key strategies:

Each restructuring strategy requires careful planning and precise execution. Financial restructuring often involves complex negotiations with creditors, shareholders, and financial institutions to realign the company’s monetary framework. Legal restructuring might include changing the business’s legal form, such as transitioning from a limited company to a limited liability partnership.

Strategic restructuring is not about drastic changes, but calculated and methodical transformation.

Operational restructuring focuses on enhancing efficiency by streamlining processes, eliminating redundant roles, and realigning departments to create a more agile and competitive organisational structure.

Pro tip: Conduct a comprehensive internal audit before initiating any restructuring to identify precise areas requiring strategic intervention.

The UK’s corporate restructuring landscape is governed by a complex legal framework of key legislative acts, primarily encompassing the Insolvency Act 1986, Companies Act 2006, and the Corporate Insolvency and Governance Act 2020. These statutes provide comprehensive guidelines for directors navigating financial challenges and corporate transformation.

Directors have critical legal responsibilities during restructuring processes, which include:

The legal mechanisms available for restructuring include various court-supervised procedures such as:

Directors must balance legal compliance with strategic business preservation.

Specifically, directors must exercise extreme caution when a company approaches financial difficulty, as their decision-making becomes critically scrutinised under legal frameworks. Failure to act responsibly can result in personal liability and potential disqualification.

The following table summarises how different restructuring procedures impact major stakeholder groups in UK companies:

| Procedure | Impact on Shareholders | Impact on Creditors | Role of Directors |

|---|---|---|---|

| Restructuring Plan | May dilute ownership, but can preserve future value | Must consider proposals; claims may be adjusted | Lead planning, ensure fair treatment and compliance |

| CVA | May affect dividend prospects | Negotiated settlements, possible losses | Facilitate negotiations, uphold legal duties |

| Administration | Shareholder control reduced | Rescue or repayment prioritised | Manage operations under administrator supervision |

| Scheme of Arrangement | Shareholder votes needed | Creditor consent critical | Coordinate court process, maintain transparency |

Pro tip: Maintain meticulous records of all decision-making processes and seek independent legal advice before implementing significant restructuring measures.

Corporate restructuring requires a systematic approach, beginning with comprehensive financial review and early intervention. The process demands meticulous planning, stakeholder engagement, and strategic decision-making to navigate complex financial challenges effectively.

The primary practical steps for corporate restructuring typically include:

The key procedural routes for UK corporate restructuring involve several critical stages:

Successful restructuring balances legal compliance with strategic business preservation.

Licensed insolvency practitioners play a crucial role in managing and overseeing restructuring proceedings, ensuring transparency and adherence to statutory requirements. They provide independent assessment and guidance throughout the complex transformation process.

Pro tip: Engage specialised legal and financial professionals early to develop a comprehensive restructuring strategy that minimises potential risks and maximises business continuity.

Corporate restructuring presents significant challenges, with numerous potential risks that demand careful navigation. Directors must approach the process with strategic precision, understanding the complex financial and legal landscape that could potentially compromise the entire restructuring effort.

The primary risks and potential pitfalls in corporate restructuring include:

Critical cost considerations for UK corporate restructuring involve multiple expense categories:

Strategic planning is the most effective risk mitigation strategy in corporate restructuring.

Common pitfalls that companies must carefully avoid include inadequate stakeholder communication, incomplete financial assessments, and failing to develop comprehensive restructuring proposals that address all potential contingencies.

The table below compares common risks and their mitigation strategies during corporate restructuring in the UK:

| Risk Type | Example Challenge | Mitigation Strategy |

|---|---|---|

| Financial Risk | Cash flow instability | Early budgeting and monitoring |

| Legal Risk | Directors’ liability exposure | Seek expert legal guidance |

| Operational Risk | Loss of staff morale | Regular stakeholder communication |

| Reputational Risk | Negative media coverage | Provide transparent updates |

Pro tip: Conduct a rigorous pre-restructuring risk assessment and maintain transparent communication with all key stakeholders to minimise potential complications.

Corporate restructuring presents complex legal challenges that demand precise strategy and expert guidance. Whether you need help understanding director duties, managing financial risks, evaluating restructuring plans or navigating legal frameworks in the United Kingdom, Ali Legal stands ready to support your business transformation with transparency and speed. Avoid costly pitfalls and ensure compliance by partnering with specialists who prioritise clear communication and tailored advice.

Take control of your company’s future with Ali Legal’s professional corporate and commercial law services. Act now to minimise risks and protect stakeholder interests through strategic legal support designed to deliver straightforward solutions. Contact us today to arrange a consultation and gain peace of mind through expert guidance tailored to your restructuring needs. Visit Ali Legal Contact Page for prompt assistance and explore how our dedicated team can help you achieve a successful restructuring outcome.

Corporate restructuring is a strategic process where businesses reorganise their operational, financial, and legal frameworks to improve performance, mitigate risks, and adapt to changing market conditions.

The key types of corporate restructuring include financial restructuring, legal restructuring, and operational restructuring, each focusing on different aspects such as debt management, legal entity changes, and operational efficiency.

Potential risks include financial risks like cash flow disruptions, legal risks such as non-compliance with regulations, operational risks affecting business continuity, and reputational risks from negative public perception.

Directors can ensure compliance by understanding their fiduciary duties, maintaining financial transparency, seeking expert legal guidance, and documenting all decision-making processes meticulously.

Mergers and acquisitions can reshape the future of any British company, but even seasoned corporate finance managers face uncertainty when the rules seem ever more technical and demanding. With the Competition and Markets Authority strictly enforcing competition law and the Companies Act 2006 guiding transaction structure, managing regulatory compliance is crucial. This article highlights the key legal frameworks, potential pitfalls, and practical steps every British finance manager should know before pursuing an ambitious merger or acquisition.

Mergers and acquisitions (M&A) represent complex legal transactions where companies combine or transfer ownership, fundamentally reshaping business structures and competitive landscapes. In the United Kingdom, these strategic manoeuvres are carefully regulated to protect market competition and consumer interests.

The legal framework for mergers and acquisitions in the UK is primarily governed by several key regulatory bodies and legislative mechanisms:

Under UK law, a merger occurs when two separate entities combine to create a single new organisation, while an acquisition involves one company purchasing another, typically absorbing its operations and assets. The CMA investigates potential market impacts to ensure these transactions do not substantially reduce market competition.

Specifically, the CMA evaluates M&A transactions based on several critical criteria:

Businesses contemplating mergers or acquisitions must navigate a complex regulatory environment that prioritises maintaining fair market conditions. The legal scrutiny ensures that corporate restructuring does not compromise consumer welfare or create monopolistic market conditions.

Pro tip: Always engage legal counsel specialising in corporate transactions before initiating any merger or acquisition to ensure comprehensive regulatory compliance and strategic alignment.

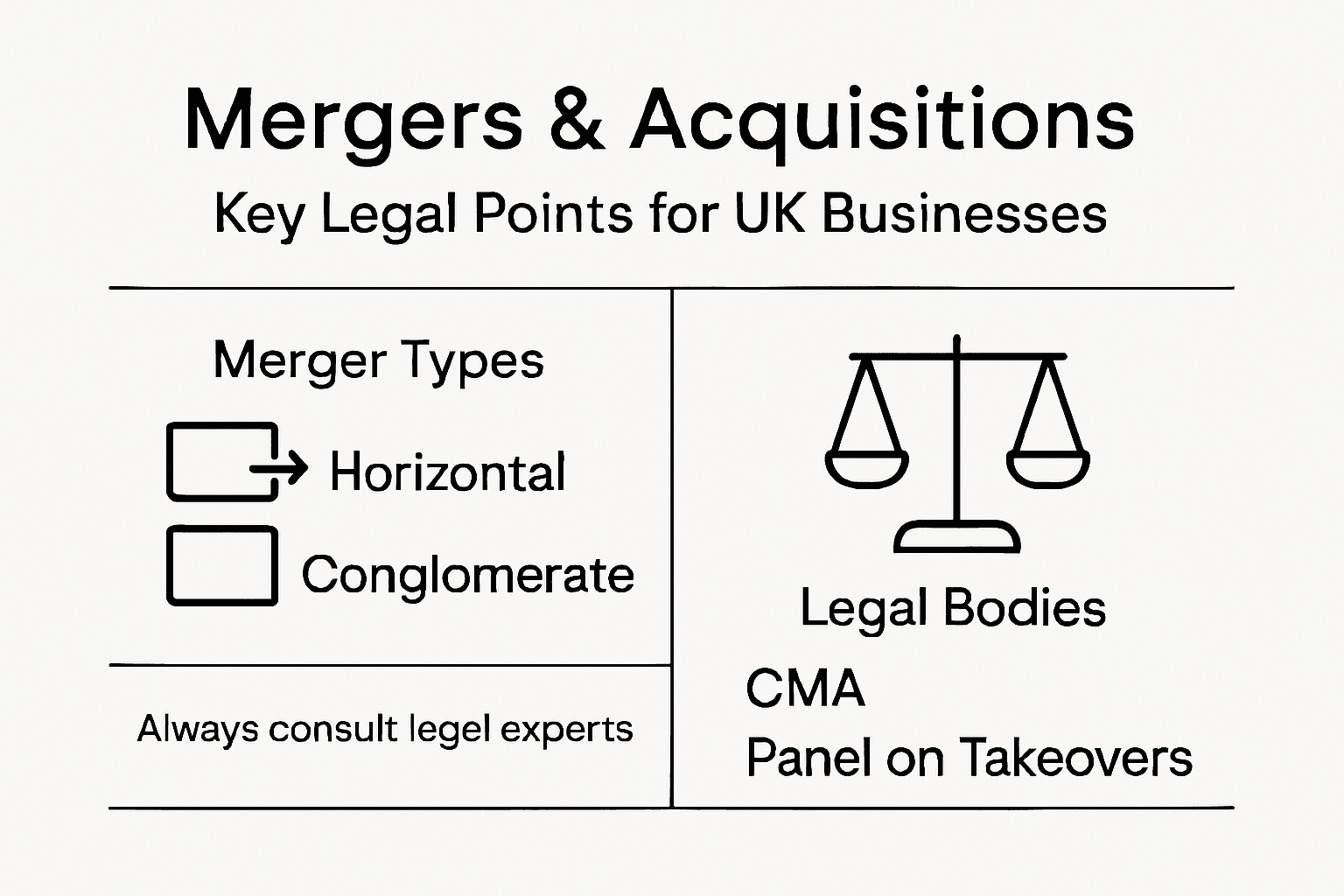

Mergers and acquisitions in the United Kingdom represent sophisticated legal strategies for corporate transformation, encompassing multiple complex transaction types designed to achieve strategic business objectives. UK legal frameworks recognise several distinctive M&A approaches that businesses can strategically employ.

The primary categories of mergers and acquisitions include:

Each merger type carries unique legal and strategic implications. Horizontal mergers typically aim to consolidate market share, reduce competition, and achieve economies of scale. Vertical mergers focus on streamlining supply chain efficiencies and reducing operational costs by integrating different production stages.

Conglomerate mergers represent more complex transactions where businesses from entirely different sectors combine, often seeking portfolio diversification and risk mitigation. These transactions require meticulous legal scrutiny to ensure compliance with competition regulations.

The following table compares the main types of mergers and acquisitions and their strategic objectives:

| Merger Type | Typical Parties Involved | Primary Objective | Key Legal Consideration |

|---|---|---|---|

| Horizontal | Direct competitors | Increase market share | Competition law compliance |

| Vertical | Supply chain partners | Streamline operations | Regulatory approval of integration |

| Conglomerate | Unrelated industries | Diversify business | Detailed risk assessment required |

| Friendly Acquisition | Willing buyer and seller | Mutual business growth | Clear communication to shareholders |

| Hostile Takeover | Unwilling target company | Gain control quickly | Defence strategies by target |

In the United Kingdom, merger transactions must navigate intricate regulatory landscapes to protect market competition and shareholder interests.

The legal mechanisms for these transactions vary, with specific processes like schemes of arrangement providing court-sanctioned methods for corporate restructuring. Companies must carefully evaluate their strategic objectives, potential synergies, and regulatory constraints when considering any merger or acquisition strategy.

Pro tip: Consult specialised corporate legal experts who understand the nuanced differences between merger types to develop a comprehensive and legally robust transaction strategy.

The United Kingdom maintains a sophisticated legal infrastructure governing mergers and acquisitions, designed to protect market integrity, shareholder interests, and economic competition. UK merger control mechanisms represent a comprehensive system of regulatory oversight that ensures transparent and fair corporate transactions.

Key regulatory bodies responsible for overseeing M&A activities include:

Statutory legislation plays a crucial role in defining the legal landscape for corporate transactions. The Enterprise Act 2002 and Companies Act 2006 provide the foundational legal frameworks that govern merger and acquisition processes, establishing clear guidelines for corporate restructuring and shareholder protections.

The Competition and Markets Authority holds particular significance in M&A transactions. This regulatory body has the power to investigate and potentially block mergers that might substantially reduce market competition or harm consumer interests. Their assessment criteria include market concentration, potential price increases, and impacts on consumer choice.

Regulatory oversight ensures that corporate transactions balance commercial interests with broader economic and consumer welfare considerations.

Additional regulatory mechanisms include the City Code on Takeovers and Mergers, which provides detailed rules for public company acquisitions. This code ensures transparency, fairness, and equal treatment of shareholders during complex corporate transactions.

Below is a summary of key UK regulatory bodies and their principal functions in M&A processes:

| Regulator | Role in M&A | Business Impact |

|---|---|---|

| Competition and Markets Authority | Monopoly prevention | May block anti-competitive deals |

| Financial Conduct Authority | Ensures market fairness | Sets standards for financial disclosures |

| Panel on Takeovers and Mergers | Administers takeover code | Protects shareholder equality |

| Financial Reporting Council | Monitors governance standards | Ensures accurate financial reporting |

Pro tip: Engage specialised legal counsel with expertise in UK corporate law to navigate the intricate regulatory landscape and ensure full compliance with statutory requirements.

The merger and acquisition process in the United Kingdom involves a structured, multi-stage approach designed to ensure transparency, regulatory compliance, and strategic alignment. CMA’s transaction investigation process provides a comprehensive framework for navigating complex corporate transactions.

The typical M&A transaction process encompasses the following critical stages:

The preliminary assessment involves extensive financial and strategic evaluation. Companies must carefully analyse potential targets, examining financial performance, market positioning, and alignment with overall business strategy. This stage requires meticulous research and strategic thinking to identify opportunities that genuinely enhance corporate value.

Successful M&A transactions balance strategic vision with rigorous financial and legal scrutiny.

Regulatory investigations represent a crucial phase in the transaction process. The Competition and Markets Authority conducts detailed assessments to ensure that proposed mergers do not substantially reduce market competition or harm consumer interests. These investigations can involve multiple stages, with companies required to provide comprehensive evidence and potentially negotiate remedies.

Pro tip: Engage specialised legal and financial advisors early in the M&A process to anticipate potential regulatory challenges and develop proactive mitigation strategies.

Mergers and acquisitions represent complex transactions fraught with potential financial and legal risks that can significantly impact corporate strategies. Insurance due diligence reveals critical hidden exposures that companies must carefully evaluate before finalising any transaction.

Key potential risks in M&A transactions include:

Financial Risks

Undisclosed historical debts

Unexpected retrospective premium adjustments

Undervalued asset assessments

Unresolved legal claims

Regulatory Risks

Potential competition authority penalties

Non-compliance with national security regulations

Unexpected integration compliance costs

Post-completion regulatory investigations

The comprehensive risk assessment requires meticulous examination of multiple corporate dimensions. Companies must conduct thorough financial, legal, and operational investigations to uncover potential liabilities that might not be immediately apparent during initial negotiations.

Successful M&A transactions demand rigorous due diligence to mitigate potential financial and legal vulnerabilities.

Legal due diligence plays a crucial role in identifying and allocating potential risks. This process involves detailed investigations into historic insurance limits, ongoing claim reserves, and potential regulatory penalties. Sophisticated organisations develop sophisticated risk transfer strategies and comprehensive business continuity plans to manage potential exposure.

Pro tip: Engage specialised forensic accountants and legal experts to conduct exhaustive risk assessments before finalising any merger or acquisition transaction.

Mergers and acquisitions demand sophisticated legal strategies to mitigate potential risks and ensure successful corporate transactions. Legal safeguards protect businesses during complex negotiations by establishing comprehensive protective mechanisms throughout the transaction process.

Key legal safeguards and potential pitfalls include:

Fundamental Legal Safeguards:

Common Potential Pitfalls:

The contractual framework represents a critical element in managing potential legal vulnerabilities. Companies must develop meticulous documentation that clearly defines expectations, allocates risks, and establishes precise mechanisms for addressing potential disputes or unexpected challenges.

Successful M&A transactions require proactive legal strategies that anticipate and mitigate potential risks before they materialise.

Regulatory compliance demands exceptional attention, particularly regarding competition laws and shareholder disclosure requirements. Organisations must navigate complex legal landscapes, ensuring transparent communication and adherence to statutory requirements throughout the transaction process.

Pro tip: Engage specialised legal counsel with extensive M&A experience to conduct comprehensive risk assessments and develop robust contractual protections.

Navigating mergers and acquisitions in the United Kingdom demands expert legal guidance to manage complex regulatory frameworks and mitigate financial and operational risks. With challenges such as compliance with Competition and Markets Authority regulations, thorough due diligence, and crafting robust contractual safeguards, the process can quickly become overwhelming. If you are seeking clarity on key legal insights and want to ensure your corporate transactions proceed smoothly, Ali Legal offers strategic, transparent, and client-focused solutions tailored for your unique situation.

Take control of your M&A journey now by consulting with our experienced legal team. We prioritise clear communication, fixed fees, and long-term relationships to help you achieve your business goals without costly surprises. Ready to safeguard your merger or acquisition with professional advice? Contact us today at Ali Legal to start securing your transaction with confidence.

A merger occurs when two companies combine to form a new entity, while an acquisition involves one company purchasing another, integrating its operations and assets into its own.

The main regulatory bodies include the Competition and Markets Authority (CMA), Financial Conduct Authority (FCA), Panel on Takeovers and Mergers, and the Financial Reporting Council.

The M&A process typically includes strategic planning, due diligence, and regulatory assessment, ensuring thorough evaluation and compliance at each stage.

Common risks include undisclosed debts, regulatory penalties, integration compliance costs, and valuation errors, all of which can significantly impact the success of a transaction.

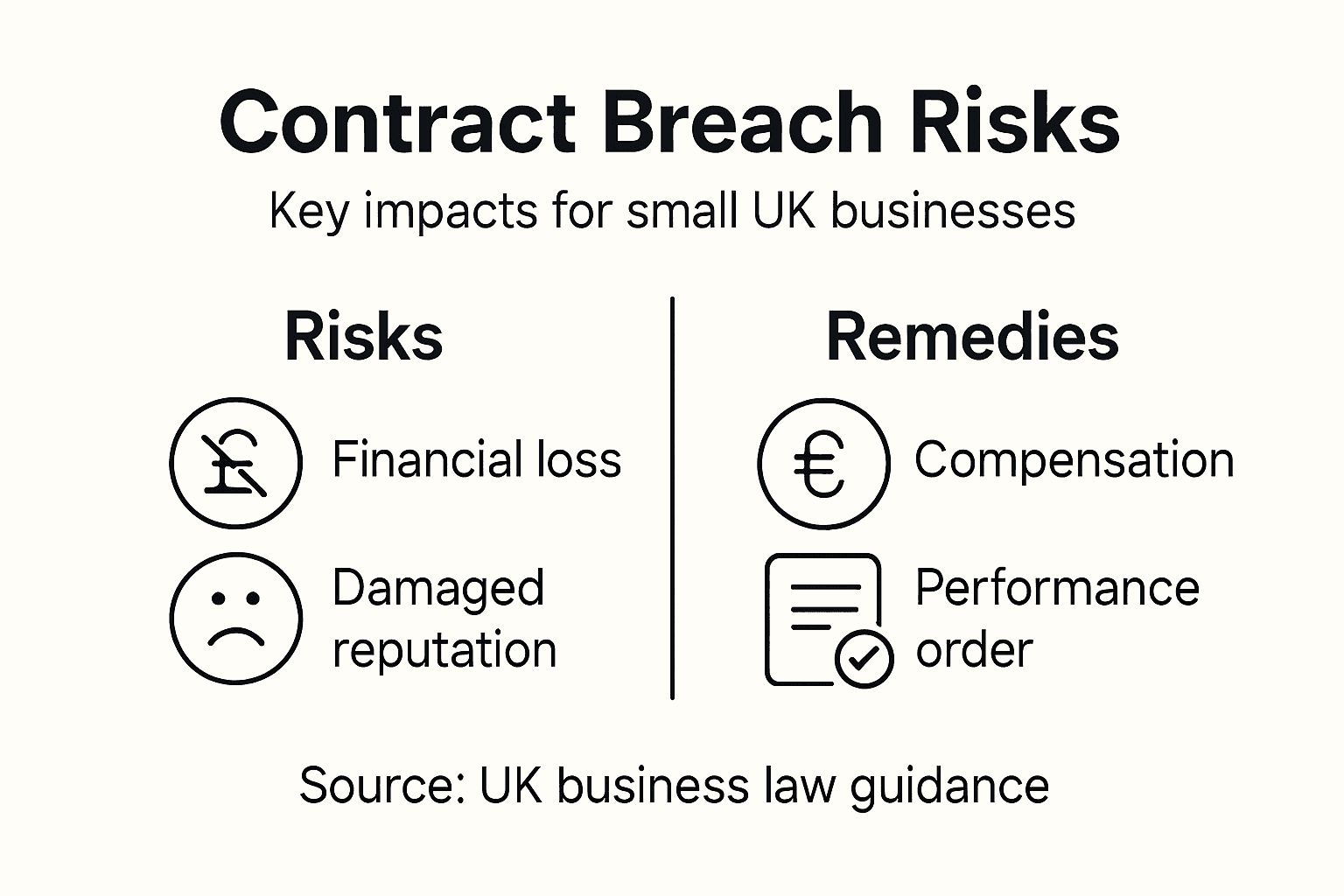

A supplier suddenly misses a key delivery, or a vendor disputes payment terms and your small business faces immediate uncertainty. For UK-based owners, these moments are not just stressful but can disrupt critical operations and threaten valuable relationships. Understanding the essentials of a breach of contract in British law helps you respond swiftly and protect your interests, ensuring every agreement works for—not against—your company.

In British legal practice, a breach of contract represents a significant legal event where one party fails to fulfil their contractual obligations as originally agreed. When considering employment contract terms, such breaches can emerge through multiple scenarios that fundamentally disrupt the established legal agreement between parties.

A breach occurs when specific contractual conditions are not met, which can manifest in several distinct ways:

Under UK law, breaches are typically categorised into three primary types: