Menu

Get Expert Legal Support Today

TL;DR:

- Fiduciary duty is a legally binding obligation that requires acting in the best interests of the beneficiary, not oneself. Breaches can lead to personal liability, penalties, or unwinding transactions, emphasizing the importance of process, disclosures, and proper governance. Understanding and carefully managing fiduciary relationships across roles and regulations is essential to avoid costly disputes and ensure lawful conduct.

Most people assume that fiduciary duty is simply about being honest or “doing the right thing.” That assumption can be costly. Fiduciary duty is a legally binding obligation with real-world consequences, including personal liability, civil penalties, and the unwinding of business transactions. Whether you are a company director, a trustee managing a family estate, or a professional handling client funds, understanding the full scope of fiduciary duty is not optional. This guide clarifies the legal principles, practical applications, regulatory standards, and contractual dimensions of fiduciary duty so you can make informed decisions.

| Point | Details |

|---|---|

| Fiduciary duty defined | A fiduciary must act in the best interests of another, guided by loyalty and care. |

| Impacts on business | Everyday decisions by company officers and professionals can trigger legal obligations and liability. |

| Compliance matters | Failure to observe fiduciary duty can lead to personal and financial penalties, especially in regulated fields. |

| Modification by contract | Certain agreements can shape or limit fiduciary duties, but boundaries are policed by courts. |

| Process over result | Courts judge fiduciaries mostly on process, disclosure, and intent, not purely on business outcomes. |

At its core, fiduciary duty is a legal relationship where the fiduciary must act in the best interests of the beneficiary or principal rather than in the fiduciary’s own interests. The word “fiduciary” comes from the Latin fiducia, meaning trust. Courts take that trust seriously, treating breaches not merely as mistakes but as wrongs that can justify significant remedies.

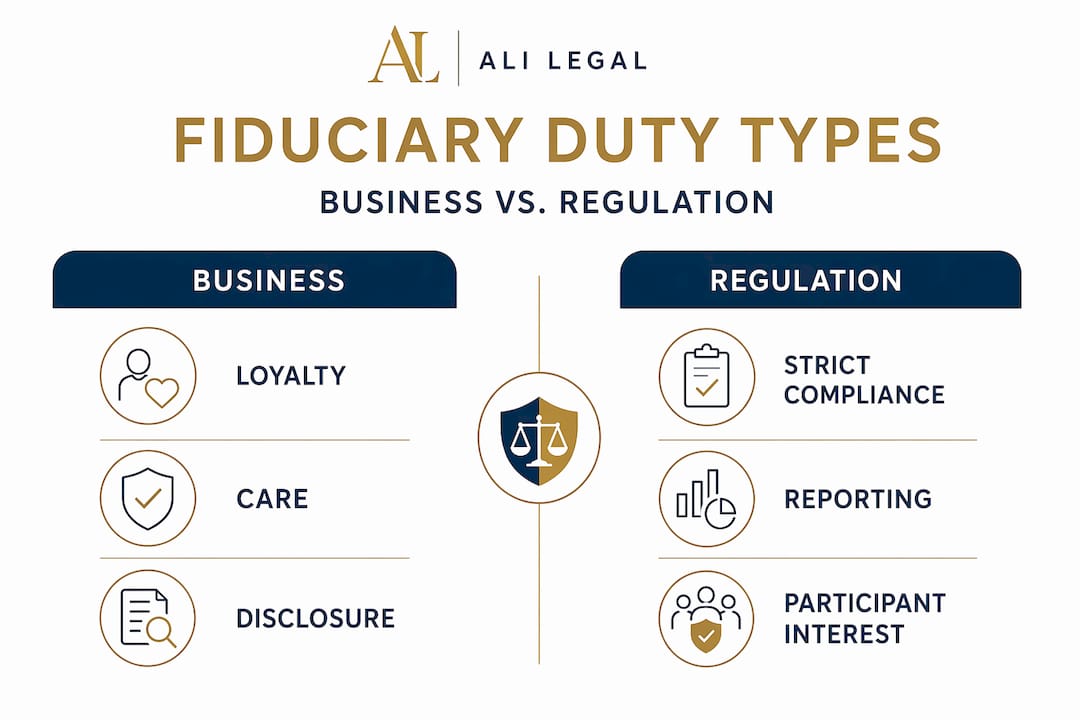

The obligations that make up fiduciary duty are often grouped into four core duties:

These duties are not abstract ideals. They show up in everyday business situations. A company director who approves a contract with a supplier they secretly part-own has breached the duty of loyalty. A pension trustee who fails to diversify fund investments without good reason may breach the duty of care. A solicitor who withholds material information from a client may breach the duty of disclosure. The consequences in each case can range from personal financial liability to disqualification from office.

Who can be a fiduciary? The list is broader than most people expect:

| Fiduciary role | Relationship to beneficiary | Common context |

|---|---|---|

| Company director | Owes duties to the company | Business governance |

| Trustee | Owes duties to trust beneficiaries | Wills, estates, family trusts |

| Solicitor/lawyer | Owes duties to client | Legal representation |

| Financial adviser | Owes duties to client | Investment and pension advice |

| Corporate officer | Owes duties to the company | Day-to-day management |

| Agent | Owes duties to principal | Real estate, commercial agents |

Understanding which category applies to your situation is the first step. The legal obligations differ in depth and scope depending on the role, but they all share the same foundational principle: someone else’s interests come first.

“A fiduciary relationship is one of the most significant legally recognised relationships precisely because it demands that self-interest yield entirely to the interests of another.” This is why courts scrutinise fiduciary conduct with such particular care.

Pro Tip: If you are uncertain whether a relationship in your business creates fiduciary obligations, look at whether one party places significant trust and confidence in another to act on their behalf. That is usually the clearest indicator. You can learn more about how these principles apply to corporate law duties in a business setting.

With a working definition in mind, let us see how fiduciary duties play out in vital business and professional relationships. The duty of loyalty and care are not theoretical concepts in a textbook. They directly shape how directors vote at board meetings, how compliance officers report misconduct, and how fund managers allocate capital.

In a business context, the most commonly scrutinised fiduciary roles include:

Comparing the duties of a company director with those of a trust trustee illustrates how fiduciary standards adapt to context:

| Aspect | Company director | Trust trustee |

|---|---|---|

| Whom duty is owed to | The company as a whole | Individual beneficiaries |

| Standard of care | Reasonable, skilled director | Prudent person managing others’ affairs |

| Conflicts of interest | Must disclose; board may authorise | Generally must avoid entirely |

| Profit rule | May profit with proper authorisation | Must not profit from position |

| Flexibility | Greater latitude via articles | Strict controls in trust deed and statute |

The consequences of breaching fiduciary duty in business are significant and often personal. They include:

Good corporate governance structures exist precisely to minimise these risks. Governance frameworks, board committees, and clear escalation policies help ensure that fiduciaries operate within their obligations, even under commercial pressure. When these frameworks fail, understanding the scope of business liability becomes critically important.

Pro Tip: Board minutes are among the most powerful tools a director has. They evidence that decisions were made with proper deliberation, full information, and in the company’s interests. Keep them detailed and accurate at every meeting.

Understanding fiduciary duty in everyday business is crucial, but regulatory frameworks add another layer of strict compliance. The United States’ Employee Retirement Income Security Act (ERISA) is one of the most instructive examples globally, including for UK business owners thinking about pension governance.

ERISA mandates that fiduciaries act solely in the interest of participants and beneficiaries. The statute goes further, requiring adherence to specific prudence and diversification standards, and it leaves little room for interpretation. The obligations are precise, and the enforcement mechanisms are robust.

The risks of failing to comply are not abstract. Fiduciaries under ERISA can be held personally accountable for breaches, including personal liability, civil penalties, and excise taxes. This means that where a trustee or plan administrator makes a careless decision, even without dishonest intent, they may be personally required to make good the loss from their own pocket.

Key compliance obligations that regulated fiduciaries must address include:

The lessons from ERISA translate directly to UK pension governance, where The Pensions Regulator expects trustees to demonstrate that their decisions are documented, considered, and made in the exclusive interest of members. Organisations that build disciplined compliance processes see dramatically fewer disputes and enforcement actions.

Effective legal risk management in this space means treating fiduciary compliance as a business process, not a legal formality. That means regular training, independent review, and a genuine culture of accountability at trustee and board level.

Pro Tip: If your business sponsors a pension or retirement plan, treat the trustee role as a distinct function with its own governance structure. Mixing it informally with other management responsibilities is one of the most common routes to inadvertent breach.

While laws set many standards, documents and contracts can sometimes modify a fiduciary’s obligations in ways that are not always obvious. Limited liability company agreements, partnership deeds, and trust documents can all affect the scope of fiduciary duties, but the latitude available is more restricted than many business owners assume.

Courts do not simply read contract terms at face value when fiduciary duties are at stake. Governing documents can influence how fiduciary duties are modified or limited, but disputes often turn on the precise details of interpretation. In a notable 2026 decision from the Delaware Court of Chancery, the court concluded that an LLC agreement had not successfully eliminated fiduciary duties, even where the drafting appeared to attempt it. The lesson: poorly worded exculpatory clauses are frequently ineffective.

There are important considerations when reviewing fiduciary provisions in business documents:

Swiss corporate governance rules offer an interesting parallel. Swiss company law imposes strict duties on directors and managers, and while board regulations can define responsibilities in detail, they cannot remove the fundamental obligations owed to the company. International business owners operating across jurisdictions often discover that local governance requirements are more demanding than their home jurisdiction’s framework.

Understanding contractual liability in this context is essential. Contractual modifications to fiduciary duty can be legitimate and commercially sensible, but only when drafted with legal precision and with full awareness of what the law permits. Similarly, trust law and fiduciary duties interact closely when family wealth is structured through trusts, and the terms of the trust deed will be examined closely in any dispute.

“Courts interpret fiduciary duty clauses strictly. What the parties intended and what the document actually achieves can be very different things—and that gap is where disputes are born.”

Here is the insight that often catches business owners off guard: a bad outcome is not the same as a breach. Courts assess fiduciary conduct based on the quality of the process, not solely the result. Fiduciary claims often focus on process, disclosures, and conflicts of interest rather than results alone. An investment that loses value does not automatically mean a trustee breached their duty. A business decision that proves commercially disastrous does not automatically expose a director to liability.

What courts actually examine is whether the fiduciary asked the right questions before deciding, whether they obtained appropriate advice, whether they disclosed relevant interests, and whether they genuinely placed the beneficiary’s interests first. This is both reassuring and demanding. Reassuring, because honest mistakes made with proper care are defensible. Demanding, because it places a high premium on documentation, transparency, and disciplined process.

The most common pitfalls we see in practice follow a familiar pattern. Conflicts of interest go undisclosed because they seem minor or obvious. Decisions are made without adequate information because time pressure feels like a valid excuse. Board minutes record conclusions without capturing the deliberative process. These gaps, individually small, collectively create the conditions for a successful breach claim.

Business owners sometimes focus on negligence law as the primary risk in commercial decisions, overlooking that a fiduciary claim can be more powerful: it does not require proving that the outcome was unreasonable, only that the process was tainted by self-interest or inadequate care.

The practical implication is straightforward. Invest in process. Record your reasoning. Disclose early and openly. Obtain independent advice on significant decisions. These habits do not just protect you legally. They make for better governance and stronger business outcomes over time.

Fiduciary obligations can arise in contexts you may not have anticipated, from a directorship taken on as a favour to a trustee role inherited through family circumstances. Anyone worried about their fiduciary obligations or facing possible breach scenarios can benefit from expert legal guidance before matters escalate.

At Ali Legal, we advise directors, trustees, business owners, and individuals on the full range of fiduciary issues, from pre-emptive compliance reviews to active dispute resolution. Our commercial litigation expertise means we understand both the legal theory and the commercial realities at stake. Whether you need to understand your obligations before signing a governance document, or you are already facing a claim, we offer clear, strategic advice built around your situation. You can also explore our civil litigation best practices resources to understand how disputes of this kind are most effectively managed. Fixed fees, direct access to experienced solicitors, and straightforward advice from day one.

Fiduciaries including directors, trustees, and plan administrators can be held personally liable for breaches, and liability can arise even where the fiduciary acted without any dishonest intent.

Certain agreements can limit or clarify fiduciary duties, but courts scrutinise such clauses closely, and duties relating to fraud or wilful misconduct are generally not waivable regardless of the contract’s terms.

A fiduciary must act with loyalty, avoid conflicts of interest, exercise due care and skill, and fully disclose all relevant information to the beneficiary or principal throughout the relationship.

Yes, fiduciary duties extend well beyond business settings and arise in personal trusts, estate administration, professional relationships such as solicitor and client, and certain medical and counselling contexts.

Courts typically focus on whether the decision-making process was sound rather than the outcome alone, so a poor result does not automatically constitute breach if the fiduciary acted with proper care, full information, and genuine good faith.