Menu

Get Expert Legal Support Today

Many people believe asset protection is simply about hiding wealth from creditors or avoiding legitimate obligations. That misunderstanding can lead to poor decisions and legal trouble. True asset protection involves legally structuring your finances and holdings to shield them from genuine risks like lawsuits, business failures, and unforeseen liabilities. This guide clarifies what asset protection actually means, explores proven strategies including trusts and business structures, and explains how UK legal frameworks support these methods. You’ll learn practical steps to evaluate your risks, select appropriate protection tools, and implement them correctly. Whether you’re a business owner or an individual with assets to preserve, understanding these principles helps you make informed decisions and avoid costly mistakes.

| Point | Details |

|---|---|

| Legal protection | Asset protection uses lawful strategies to safeguard personal and business holdings from creditors, lawsuits, and liabilities. |

| Multiple tools | Effective protection combines trusts, insurance policies, and appropriate business structures tailored to individual circumstances. |

| UK compliance | Success requires understanding and following UK legal frameworks to ensure strategies remain valid and enforceable. |

| Professional guidance | Expert legal advice prevents common pitfalls and ensures asset protection plans align with current regulations. |

| Regular reviews | Updating protection measures as circumstances change maintains their effectiveness over time. |

Asset protection refers to strategies that legally protect assets from creditors and liabilities. It’s not about evading legitimate debts or hiding wealth from authorities. Instead, it involves structuring your holdings in ways that make them less vulnerable to claims whilst remaining fully compliant with the law.

The purpose is straightforward: preserve what you’ve worked to build. Business owners face risks from commercial disputes, professional negligence claims, and contract breaches. Individuals encounter threats from divorce proceedings, personal injury claims, and unexpected financial crises. Without proper protection, a single lawsuit or business failure can wipe out savings, property, and investments accumulated over decades.

Several misconceptions cloud understanding of this field. Some think asset protection only matters for the wealthy, but anyone with property, savings, or business interests benefits from appropriate safeguards. Others assume it involves offshore accounts or complex schemes, when often the most effective tools are domestic trusts and properly structured business entities. The key is matching strategies to your specific situation and risk profile.

Key risks that asset protection addresses include:

Understanding legal risk management forms the foundation for effective asset protection. UK law provides various frameworks, from trust legislation to company structures, that enable legitimate protection when used correctly. The challenge lies in selecting appropriate tools and implementing them before problems arise, because courts view protection measures established after a claim surfaces with considerable scepticism.

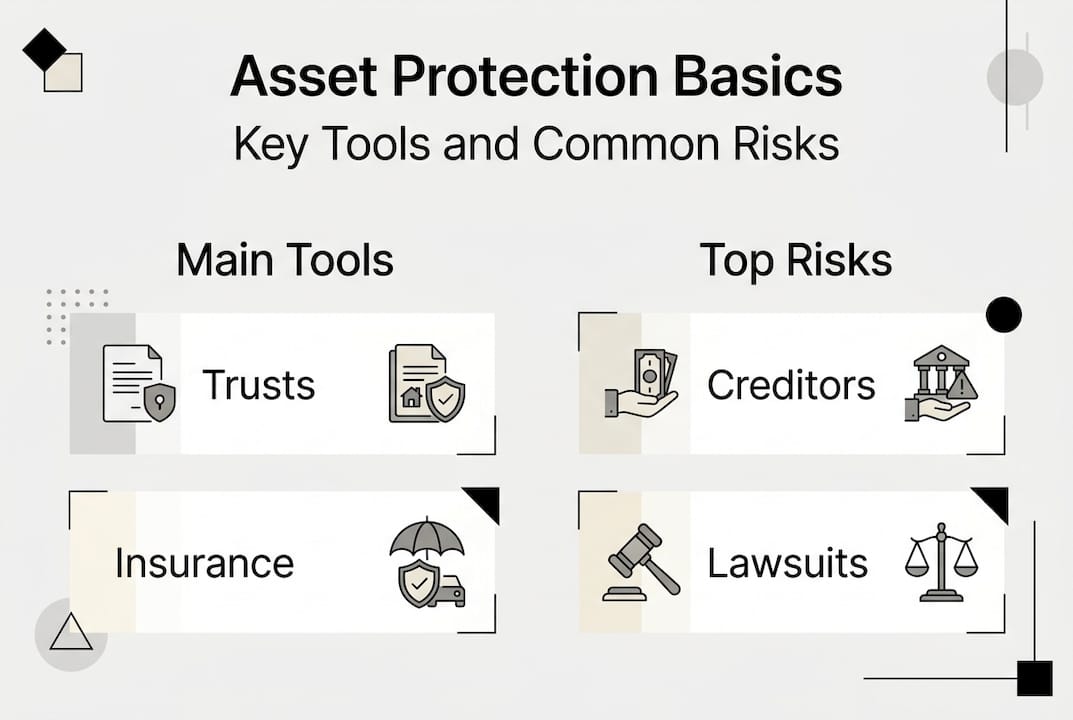

Several proven methods help safeguard assets, each with distinct advantages depending on your circumstances. The most effective approach typically combines multiple strategies rather than relying on a single tool.

Trusts are a popular legal mechanism used to isolate assets from personal liabilities in the UK. When you place assets into a properly structured trust, they’re owned by the trust itself rather than you personally. This separation means creditors pursuing claims against you cannot easily access trust property. Discretionary trusts offer particular flexibility, allowing trustees to distribute income and capital among beneficiaries as circumstances change.

Insurance provides another essential layer of protection. Professional indemnity insurance shields business owners from negligence claims, whilst liability insurance covers accidents and injuries. These policies transfer risk to insurers, preventing claims from directly threatening your personal wealth. The key is maintaining adequate coverage limits that reflect your actual exposure.

Business structures significantly impact asset protection. Operating as a limited company creates legal separation between business debts and personal assets. If the company faces financial difficulty, creditors generally cannot pursue directors’ personal property beyond their investment in the company. This contrasts sharply with sole traders, whose personal assets remain fully exposed to business liabilities.

| Strategy | Primary benefit | Main limitation |

| — | — |

| Discretionary trusts | Strong creditor protection through legal separation | Requires professional setup and ongoing management |

| Limited companies | Shields personal assets from business debts | Directors may face personal liability for wrongful trading |

| Insurance policies | Transfers risk to insurers with defined coverage | Only protects against insured risks up to policy limits |

| Pension schemes | Protected from most creditors under UK law | Funds locked until retirement age |

UK legal frameworks support these strategies through established trust law, company legislation, and insurance regulations. However, certain limitations apply. Courts can set aside transfers made to defraud creditors, and some debts like personal guarantees pierce corporate protection. Understanding these boundaries prevents wasted effort on ineffective measures.

Practical implementation tips include:

Pro Tip: Many people focus solely on property law when protecting real estate, but combining property ownership structures with insurance and trusts creates far stronger protection than any single method alone.

The most robust protection comes from layering strategies. A business owner might operate through a limited company, maintain comprehensive insurance, place investment property in a trust, and maximise pension contributions. Each layer addresses different risks, and together they create defence in depth that’s difficult for creditors to penetrate. Professional advice ensures these elements work together effectively rather than creating conflicts or gaps.

Successful asset protection depends on understanding and complying with UK legal frameworks to avoid challenges. Several key areas of law shape what’s permissible and what crosses into problematic territory.

Trust law provides the foundation for one of the most powerful protection tools. The Trustee Act 2000 and various case law principles govern how trusts must be established and administered. Trusts created for legitimate purposes like estate planning or protecting vulnerable beneficiaries receive full legal recognition. However, trusts established solely to frustrate creditors may be set aside under the Insolvency Act 1986.

Property law affects how you can structure ownership of real estate and physical assets. Joint tenancy versus tenancy in common creates different inheritance and creditor exposure profiles. Placing property into trusts or companies changes the legal ownership and associated protections. Each structure carries specific implications for tax, succession, and creditor access.

Company law determines how business structures protect personal assets. The Companies Act 2006 establishes limited liability for shareholders, but directors face personal liability for wrongful trading if they continue operating whilst insolvent. Understanding these boundaries helps you maintain protection whilst avoiding personal exposure.

Ensuring legal compliance requires several steps:

The timing of protective measures matters enormously. Courts scrutinise transfers made shortly before or after claims arise, often viewing them as attempts to defraud creditors. Establishing protection during stable periods, as part of normal financial planning, carries far less risk of challenge.

Common legal pitfalls include:

Professional legal advice significantly improves outcomes in securing assets effectively. Attempting to implement complex structures without expert guidance often creates vulnerabilities rather than protection.

Documented professional consultation serves two purposes. First, it ensures your strategies actually work as intended under current law. Second, it demonstrates good faith if anyone later questions your actions. Courts view individuals who sought and followed professional advice more favourably than those who attempted DIY protection schemes.

Estate planning integrates closely with asset protection. Wills, trusts, and succession planning all affect how assets are protected during your lifetime and after death. Coordinating these elements prevents gaps where assets become vulnerable during transitions.

Regular legal reviews keep protection current as laws change. Tax legislation, insolvency rules, and trust law all evolve. What worked five years ago might now create unexpected exposure. Annual reviews with your legal adviser identify needed updates before problems arise.

Implementing effective protection requires systematic evaluation of your situation followed by targeted action. Start by assessing your specific risks and assets, then select appropriate strategies.

Step by step risk evaluation and strategy selection:

Personal finance scenarios demonstrate how protection works in practice. Consider a medical professional facing potential negligence claims. Professional indemnity insurance provides the first line of defence, covering most claims up to policy limits. Placing the family home and investment property into a trust adds another layer, separating personal assets from professional liabilities. Maximising pension contributions moves additional wealth into protected vehicles.

Business contexts require different approaches. A company director might establish a limited company to separate business debts from personal wealth. Key person insurance protects against financial impact if crucial team members become unable to work. Maintaining proper corporate formalities, separate bank accounts, and clear documentation preserves the limited liability protection.

Insurance and liability coverage form essential components of any protection plan. Professional indemnity, public liability, and directors’ and officers’ insurance address different risk categories. The key is matching coverage to actual exposure. Under insurance leaves gaps, whilst excessive coverage wastes money better spent elsewhere.

Planning and regular reviews are key to keeping asset protection measures effective over time. Life changes constantly. You acquire new assets, start businesses, face different risks, and encounter evolving legal frameworks. Annual reviews ensure your protection adapts accordingly.

Pro Tip: The most common implementation mistake is waiting until problems appear before establishing protection. Courts view last minute transfers with extreme scepticism and often set them aside. Effective protection requires planning during calm periods, not crisis response.

Practical implementation considerations include:

Real world application often combines multiple tools. A business owner might operate through a limited company with comprehensive insurance, place investment property in a family trust, maximise pension contributions, and maintain emergency reserves in protected accounts. Each element addresses specific risks whilst together creating robust overall protection.

Common mistakes to avoid during implementation:

The most effective protection balances security with practicality. Overly complex schemes become difficult to maintain and may not survive legal challenge. Simple, well documented structures implemented for clear purposes tend to prove most durable. Focus on legitimate business and family planning objectives, with asset protection as a natural consequence rather than the sole purpose.

Protecting your assets requires more than understanding general principles. You need strategies tailored to your specific situation, implemented correctly within UK legal frameworks. That’s where expert guidance makes the difference between effective protection and wasted effort.

Ali Legal provides experienced civil litigation support when disputes threaten your interests. Our team understands how asset protection intersects with litigation, helping you safeguard holdings whilst resolving conflicts effectively. We’ve guided countless clients through complex situations where proper planning prevented devastating losses.

Our commercial litigation expertise extends to protecting business interests during high stakes disputes. Whether you’re facing contract breaches, partnership disagreements, or creditor claims, we develop strategies that defend your position whilst preserving what you’ve built.

Accessible consultations let us understand your unique circumstances and tailor protection strategies accordingly. We explain options clearly, outline costs transparently, and help you make informed decisions about safeguarding your wealth. Contact Ali Legal today to discuss how we can help secure your financial future with expert legal guidance and proven asset protection strategies.

Asset protection encompasses legal strategies that shield your wealth from creditors, lawsuits, and other financial threats. It matters because unexpected claims, business failures, or legal disputes can eliminate assets you’ve spent years building. Proper protection preserves your financial security whilst remaining fully compliant with UK law.

Trusts create legal separation by transferring ownership to the trust itself, removing assets from your personal estate. This differs from insurance, which transfers risk to insurers, and company structures, which separate business from personal liabilities. Trusts offer particular strength against personal creditors but require proper setup and ongoing administration to remain effective.

Courts can set aside transfers made to defraud creditors under insolvency law, potentially reversing your protection efforts. You might face accusations of fraudulent conveyance if timing or documentation appears suspicious. Improperly structured protection can also trigger unexpected tax liabilities or fail to provide intended benefits, wasting time and money.

Costs vary significantly based on complexity. Simple measures like adequate insurance might cost hundreds annually, whilst establishing trusts typically requires several thousand pounds in legal fees plus ongoing administration costs. Limited company formation costs less than trusts but requires annual compliance expenses. Professional advice helps identify cost effective options for your situation.

Seek advice before problems arise, ideally as part of regular financial planning. Once claims surface or financial difficulty looms, options become limited and courts scrutinise any protective measures closely. Early consultation during stable periods provides maximum flexibility and ensures strategies withstand potential challenges whilst serving legitimate purposes.