Menu

Get Expert Legal Support Today

TL;DR:

- Residency status affects legal rights, obligations, and benefits in a country, but definitions vary across domains. It is possible to be a resident in multiple jurisdictions simultaneously, creating complex tax, legal, and compliance considerations. Proper legal analysis and proactive structuring are essential to avoid costly mistakes and leverage residency benefits effectively.

Residency status is one of the most misunderstood concepts in law and finance, and that misunderstanding carries real consequences. Many people assume their citizenship or visa determines how they are treated in every legal context, but that is rarely the whole picture. Your residency status for tax purposes may be completely different from your status for immigration or banking purposes, sometimes within the very same country. Whether you are an individual relocating abroad, a business expanding across borders, or someone managing assets in multiple jurisdictions, knowing precisely where you stand is not optional. It is foundational.

| Point | Details |

|---|---|

| Residency differs by context | Tax, legal, and immigration authorities can all treat you as a resident under different rules. |

| Multiple residencies possible | It’s common and sometimes required to have more than one residency at the same time. |

| Check legal criteria | Always confirm residency rules before moving, investing, or filing taxes to avoid costly errors. |

| Strategic planning pays off | Planning your residency properly can protect assets, reduce risk, and maximise compliance. |

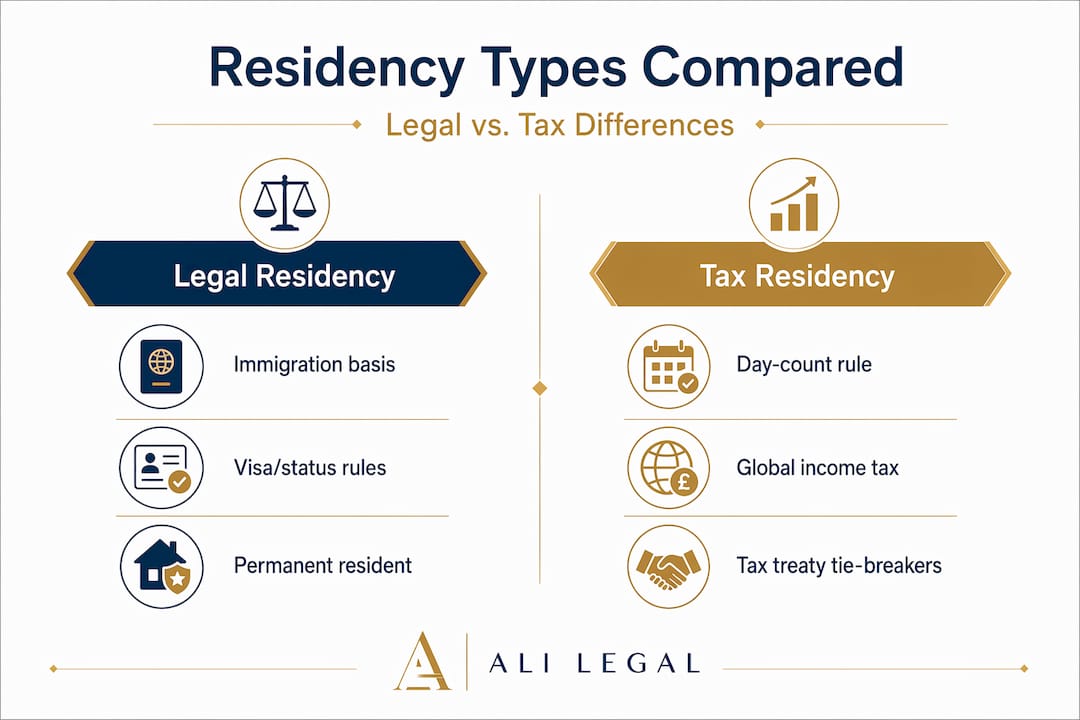

At its core, residency status is a legal concept that determines your rights, obligations, and the benefits you are entitled to in a given country. But the term does not mean the same thing across every legal domain. Tax authorities define it one way, immigration agencies define it another, and civil courts may apply a third interpretation entirely.

Residency status usually refers to whether an individual or business is treated as a resident under a country’s rules, particularly for tax and jurisdictional purposes, and this can differ substantially from immigration or visa status. That distinction is not a technicality. It is the difference between owing taxes in one country or three, between qualifying for banking services or being rejected, and between operating a business legally or unknowingly triggering foreign compliance obligations.

The OECD makes this especially clear in its guidance on tax residency. Tax residency is determined under each jurisdiction’s domestic tax laws, and a person may be a tax resident in more than one jurisdiction simultaneously. Holding citizenship or having the right to reside in a country does not automatically make you a tax resident there.

Here is why that matters in practice:

It is also worth understanding the difference between residency and citizenship law. Citizenship is typically permanent and tied to nationality; residency is transactional and contingent on specific legal tests that can change year to year.

No two countries determine residency using exactly the same framework, though several common tests apply across major jurisdictions. Understanding these frameworks is essential if you operate, live, or hold assets in more than one country.

For individuals, US tax residency is established if a person meets either the Green Card Test or the Substantial Presence Test for the calendar year. The Green Card Test is straightforward: if you hold a lawful permanent resident card, you are a US tax resident regardless of where you actually live. The Substantial Presence Test is more nuanced.

Under the Substantial Presence Test, you are treated as a US resident if you meet a day-count formula of at least 183 days during a three-year period, calculated using all current-year days, one-third of the prior year’s days, and one-sixth of the year before that. Exceptions apply for exempt individuals (such as students and diplomats), but most long-term visitors are caught by this rule without realising it.

![]()

For companies, the picture is equally complex. Canadian corporate residency can be “deemed” (for example, if the company was incorporated in Canada after April 1965) or determined through the common-law test of central management and control. Crucially, treaty rules can override these deeming provisions entirely, which is why corporate residency demands specific legal analysis rather than assumptions.

The table below summarises how several major jurisdictions approach residency determination:

| Country | Individual test | Corporate test | Treaty override? |

|---|---|---|---|

| United States | Green Card Test or Substantial Presence Test | Place of incorporation or management | Yes |

| United Kingdom | Statutory Residence Test (days and ties) | Central management and control | Yes |

| Canada | Common-law ties or deemed | Incorporation or central management | Yes |

| Australia | Domicile or 183-day rule | Place of incorporation or central management | Yes |

| Germany | Habitual abode or domicile | Registered seat or management | Yes |

To assess your own residency status, walk through this process:

Pro Tip: Never assume a tax treaty automatically resolves your dual residency. Treaty tie-breakers are assessed in a specific order and require factual analysis. Claiming the wrong status on a self-certification form can constitute a false declaration, which carries serious legal penalties in many jurisdictions. The UK extradition law framework is one example of how far cross-border legal consequences can reach when individuals misrepresent their status.

Many people are surprised to learn that having residency status in more than one country at the same time is not just possible; it is relatively common. This happens for individuals who relocate mid-year, for businesses that operate across borders, and for anyone who triggers residency tests in multiple countries simultaneously.

The US IRS explicitly acknowledges this: you can be both a nonresident and a resident for US tax purposes during the same calendar year, typically in the year you arrive or depart. This is called dual-status filing, and it triggers specific reporting requirements that differ from standard resident or nonresident returns.

For global banking and CRS-style reporting, financial institutions are required to collect self-certifications that disclose all tax residences, not just one. This confirms that multiple tax residencies are a real and documented scenario, not a legal anomaly.

“A person may be a tax resident in more than one jurisdiction simultaneously, and financial institutions under the Common Reporting Standard must collect and report all relevant tax residences.” — OECD CRS guidance

The following table illustrates how dual residency can arise in practice:

| Scenario | Tax consequence | Immigration consequence |

|---|---|---|

| Moving to the US mid-year | Dual-status tax return required | Visa or Green Card status separate |

| UK national working in Germany | May be tax resident in both | Separate immigration rules apply |

| Canadian company with UK board | Possible dual corporate residency | Corporate registration rules differ |

| Retired expat splitting time | Day-count triggers multiple residencies | Immigration permissions may be limited |

The risks of misunderstanding your status in these situations are significant:

Matters related to international law for businesses and conflict of laws become directly relevant here, particularly when businesses are structured across multiple legal systems and assume their incorporation jurisdiction is their only residency.

Knowing the theory is one thing. Applying it to your specific circumstances is another. Here is a structured approach to establishing your residency status across the most common frameworks.

Step-by-step checklist:

Tax residency determinations often hinge on days and factual ties, but countries can also use treaty tie-breakers or domestic deeming rules. Residency status for tax treaties and for immigration programmes are not automatically the same, which is why they must always be assessed separately.

For immigration-specific contexts such as US naturalisation, the USCIS definition of continuous residence is tied to maintaining a permanent dwelling place as a lawful permanent resident, with specific thresholds for absences that can interrupt continuity. This is entirely separate from the Substantial Presence Test used by the IRS.

State-level rules add another layer of complexity. In New York State, for example, the resident concept is linked to domicile rather than physical presence alone. New York differentiates between domicile and statutory residence, and residents are taxed on all income regardless of where it is earned. This means a person could be a nonresident for federal purposes but a resident for state purposes.

Pro Tip: Businesses expanding cross-border frequently underestimate how quickly they can become tax-resident in a new jurisdiction. A single director signing contracts or making decisions from a foreign country can trigger corporate residency under the central management and control test. Structure your board activities carefully with legal guidance, as explored further in UK trust law and asset protection planning.

Documents typically required to prove residency status to banks, tax authorities, and immigration agencies include:

Most articles on residency status treat it as a purely administrative matter. Check the boxes, count the days, file the right form. But in our experience working with individuals and businesses across multiple jurisdictions, the most serious problems arise not from ignorance of the basic rules but from overconfidence in simplified answers.

Dual-status tax years are a perfect example. Many people receive advice that they “left” or “arrived” in a country and assume their residency changed neatly on that date. In reality, the IRS, HMRC, and equivalent bodies analyse the entire year holistically. A single miscalculated day, one overlooked tie, or one assumption about a treaty can result in a surprise tax liability that dwarfs any professional fee that proper advice would have cost.

We also see businesses make avoidable errors when expanding internationally. A UK company that appoints a director in Singapore, holds board meetings there, and delegates strategic decisions to that director may find itself treated as a Singapore tax resident under the central management and control test, entirely contrary to what was intended. This creates corporate residency in two jurisdictions simultaneously, with all the compliance costs that entails.

The strategic opportunity that most guides ignore is that residency status, when planned proactively, can offer genuine advantages. Structuring where you are resident, and in which legal sense, can influence how assets are protected, where disputes are resolved, and how efficiently income is taxed. The key word is proactive. Reactive compliance after a tax authority raises an enquiry is expensive and stressful. Structuring your residency deliberately and legally, before you move or expand, is the approach that sophisticated individuals and businesses take.

Our strongest advice: never rely on verbal reassurances, simplified online tools, or generic country guides. Your specific facts determine your status, and those facts must be assessed by someone qualified to apply the relevant legal tests. The consequences of getting it wrong, whether double taxation, penalties, or legal disputes, are too significant to treat as an afterthought.

Navigating residency status across multiple countries requires more than a checklist. It requires precise legal analysis of your specific circumstances, applied against the relevant domestic laws, treaty provisions, and reporting obligations.

At Ali Legal, we work with individuals, businesses, and international clients on exactly these challenges. Our team has direct experience with immigration law, multi-jurisdictional disputes, cross-border corporate compliance, and international law services that span civil, commercial, and regulatory matters. Whether you are planning a move, restructuring a business, or responding to a compliance query from a tax authority, we can provide the specific, documented advice you need to act with confidence. To discuss your situation with a qualified solicitor, speak to our team today.

Yes, countries apply different legal definitions to each domain, so you may be a resident for tax but not for immigration purposes, or vice versa. The OECD confirms that the right to reside or hold citizenship does not automatically confer tax residency.

You will typically need proof of address, records of time spent in each country, and local tax filings or identification numbers. CRS reporting requirements mean financial institutions are also obliged to collect self-certifications disclosing all tax residences.

It applies a three-year day-count formula where you qualify as a US resident if the total reaches at least 183 days, calculated as all current-year days plus one-third of the prior year and one-sixth of the year before that.

Yes, if a company meets the legal residency tests in multiple jurisdictions simultaneously, it can hold dual residency unless a tax treaty resolves the conflict. Canadian corporate tax rules illustrate this clearly, as residency can arise through both incorporation and central management, with treaty overrides available in some cases.