TL;DR:

- Marine insurance law is a specialized legal framework governing maritime risks like storms and piracy.

- Core principles include utmost good faith, insurable interest, and proximate cause, affecting claim validity.

- Businesses must regularly review and adapt policies due to evolving risks and legal nuances in international waters.

Many shipowners and cargo operators assume their standard commercial policy covers everything that can go wrong at sea. It does not. A single cargo loss in international waters, an uninsured hull collision, or a missed warranty clause can expose a business to millions in unrecovered losses. Marine insurance law is a distinct legal framework built specifically around the perils of maritime commerce, and understanding it is not optional for businesses that operate ships, move cargo, or manage freight. This guide covers what marine insurance law is, the principles that govern it, the policy types available, current market trends, and how to apply it all in practice.

| Point | Details |

|---|---|

| Covers maritime risks | Marine insurance law specifically covers losses from perils at sea, not just general business risks. |

| Principles govern claims | Utmost good faith, indemnity, and other principles decide how claims succeed and when they can fail. |

| Policy choice is critical | Selecting the right type of marine policy is essential for full protection—standard business insurance is not enough. |

| Law is globally influential | UK marine insurance principles shape laws worldwide but local legal details must always be checked. |

| Legal advice avoids pitfalls | Consulting marine legal experts minimises compliance issues and claim disputes. |

Marine insurance law is not simply a subset of general insurance. It is a specialised body of law that governs contracts where an insurer agrees to indemnify the insured against losses arising from maritime perils. As the Marine Insurance Act 1906 establishes, these contracts cover ships, cargo, freight, and liabilities arising during marine adventures. The Act, passed in the United Kingdom, remains one of the most influential pieces of insurance legislation ever written, and its principles have been adopted across dozens of jurisdictions worldwide, including through instruments such as Canadian marine insurance law.

“Marine insurance law governs contracts where an insurer indemnifies the insured against losses from maritime perils during marine adventures, including ship, cargo, freight, and liabilities.”

The parties involved are straightforward: the insured (shipowner, cargo owner, or freight operator), the insurer (underwriter or mutual club), and sometimes a broker acting as intermediary. The subject matter can be a vessel, a consignment of goods, the expected freight income, or third-party liabilities. What makes this framework unique is how it defines a “maritime peril.” This includes storms, fire, collision, piracy, jettison, and barratry, among others. General commercial policies rarely contemplate these risks with the same precision.

A common misconception is that any business insurance policy will respond to a cargo loss at sea. In reality, without a specific marine policy aligned with the maritime law framework, a claim may be declined on the basis that the peril is not covered. Businesses operating internationally must treat marine insurance law as a foundational compliance requirement, not an optional add-on.

Key parties and their interests at a glance:

The legal principles underpinning marine insurance are not abstract theory. They directly determine whether a claim succeeds or fails. The core concepts in maritime insurance include utmost good faith, insurable interest, indemnity, proximate cause, subrogation, contribution, warranties, and sue and labour. Each one carries practical weight.

Businesses often stumble on disclosure and warranties. Under the Insurance Act 2015, which reformed the MIA 1906 for commercial policyholders, the duty of fair presentation replaced the older harsh disclosure rules. However, the Indian marine insurance framework and others still carry stricter requirements. If you trade internationally, navigating maritime legal requirements across jurisdictions is essential, and the principles of UK contract law apply to how these marine contracts are interpreted.

Pro Tip: Always document your vessel’s condition, cargo specifications, and voyage details before inception of cover. Gaps in disclosure are the single most common reason marine claims are disputed.

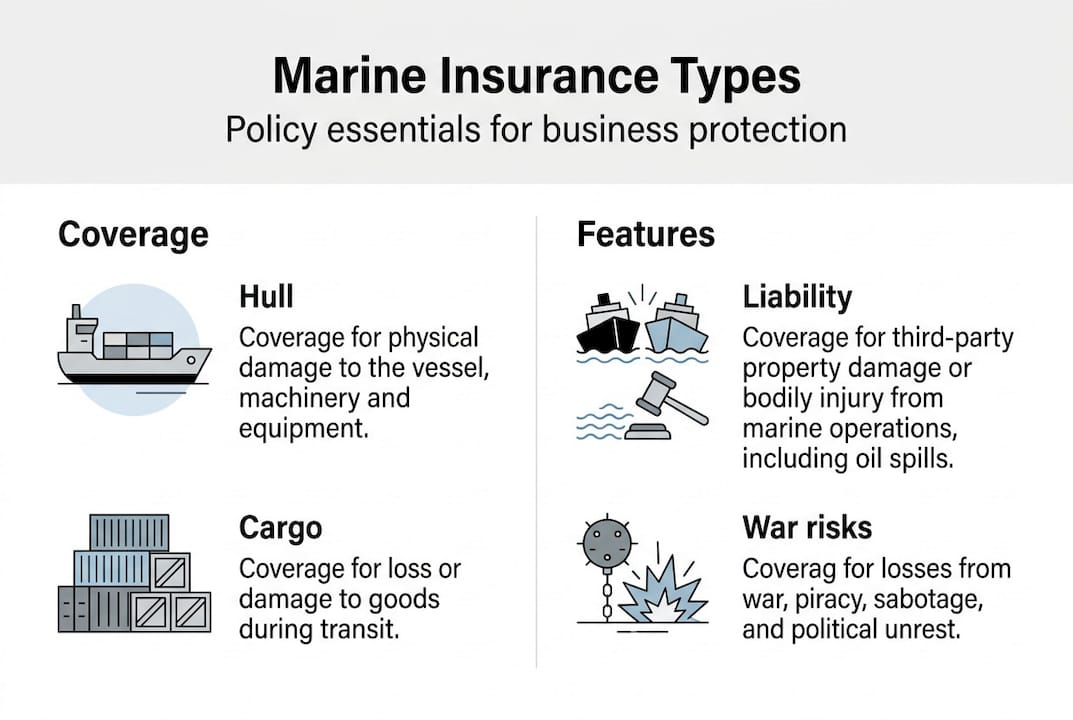

Choosing the right type of marine insurance is as important as understanding the law behind it. Policy mechanics and coverage types confirm that every policy must specify the assured, the subject matter, the risks covered, the sum insured, and the period of cover. Missing any of these elements creates ambiguity that insurers will exploit at the claims stage.

The four primary categories are:

| Coverage type | What it protects | Key feature |

|---|---|---|

| Hull and Machinery | The vessel and equipment | Physical damage, total loss |

| Cargo (ICC A/B/C) | Goods in transit | Broad to narrow named perils |

| Freight | Expected freight income | Income protection on loss |

| P&I | Third-party liabilities | Mutual club, broader liability |

P&I clubs deserve special mention. They are mutual associations, not commercial insurers, and they cover liabilities that standard H&M policies exclude. For businesses facing a shipping dispute insurance scenario, P&I cover is often the critical layer. Ambiguous policy wording and gaps between H&M and P&I cover are among the most expensive mistakes businesses make. Review marine insurance key concepts carefully before placing cover.

The marine insurance market is not static. Global marine premiums reached USD 39.92 billion in 2024, reflecting sustained growth driven by geopolitical disruption, rising asset values, and increasing cargo volumes. The Red Sea crisis, sanctions exposure, and climate-related losses have all pushed underwriters to reassess risk appetites.

“The global marine insurance market continues to grow, but loss ratios are stabilising as underwriters apply stricter risk selection and pricing discipline.”

| Region | Premium share (2024) | Key risk driver |

|---|---|---|

| Europe | ~45% | Geopolitical, sanctions |

| Asia Pacific | ~30% | Cargo volume, natural catastrophe |

| Americas | ~15% | Gulf weather, piracy |

| Rest of world | ~10% | Emerging trade routes |

On the legal front, the pay first clause ruling in MS Amlin v King Trader confirmed that pay first clauses in marine policies are enforceable even in insolvency situations. This has significant implications for businesses relying on P&I cover when counterparties become insolvent. General average cases continue to generate disputes, particularly where cargo interests contest contributions. The fortuity principle, which requires that a loss be accidental rather than intentional, has also been tested in recent cases involving deliberate scuttling.

For businesses with cross-border exposure, UK international business law and cross-border contract law intersect directly with how marine insurance disputes are resolved. Jurisdiction clauses in policies matter enormously when a claim arises in a foreign port.

Knowing the law is one thing. Applying it consistently within your business operations is another. Geopolitical risks including the Red Sea and sanctions regimes are actively reshaping premium structures in 2026, and businesses that fail to update their cover accordingly will find gaps at the worst possible time.

Here is a practical five-step compliance checklist:

The top mistakes businesses make include assuming renewal terms are identical to the previous year, failing to notify insurers of route changes, and neglecting to read exclusions carefully. Understanding business liability essentials is a useful complement to your marine insurance review. The Marine Insurance Act 1906 remains the bedrock text, and familiarity with its provisions is non-negotiable for any business operating in this space.

Pro Tip: Request a policy gap analysis from your broker or legal adviser every time your trading patterns change. What was adequate cover last year may be dangerously inadequate today.

Most articles on marine insurance law stop at the principles and policy types. The harder truth is that the greatest risk for businesses is not ignorance of the law. It is the assumption that a policy placed last year still fits the risks you carry today.

Marine commerce is not static. Sanctions lists change overnight. New trading routes open through previously uncharted waters. Climate events alter the frequency and severity of losses in ways that insurers are still pricing into their models. A policy that was perfectly adequate for a fixed trade route in 2024 may carry silent gaps in 2026 if the vessel now transits a sanctioned region.

We have seen businesses invest significant effort in understanding the legal framework, only to rely entirely on their broker’s annual renewal without independent scrutiny. Brokers are valuable, but they are not your legal advisers. The distinction matters when a claim is disputed. Regular independent review, legal due diligence on policy wording, and a genuine readiness to challenge insurer interpretations are what separate businesses that recover from losses from those that do not. Navigating maritime complexities requires ongoing legal engagement, not a one-time policy placement.

Understanding marine insurance law is the foundation, but applying it correctly under commercial pressure is where businesses most often need support. Legal counsel adds value at every stage: selecting the right policy structure, reviewing contract terms before placement, managing claims disputes, and responding to enforcement actions.

At Ali Legal, our maritime law services are designed for businesses that need clear, strategic advice on high-value maritime risks. Whether you are dealing with a cargo dispute, a hull claim, or a P&I liability, our team brings both legal precision and commercial understanding to the table. We also offer commercial dispute support for businesses where insurance disputes escalate into litigation. If you want to ensure your marine insurance arrangements are legally sound and commercially robust, speak to our legal team today.

It covers losses related to ships, cargo, freight, and liabilities from maritime perils such as storms, collisions, fire, and piracy. The framework is built around indemnifying the insured for financial losses arising during marine adventures.

The key principles are utmost good faith, insurable interest, indemnity, proximate cause, subrogation, contribution, warranties, and sue and labour. Each principle affects whether a claim is valid and how much is recoverable.

Policies must specify the assured, the subject matter, the risks covered, the sum insured, and the period of cover. The type of policy, whether hull, cargo, freight, or P&I, determines the scope of protection.

A P&I club is a mutual insurer that covers third-party maritime liabilities excluded from standard hull and machinery policies, including environmental damage, crew injury, and cargo claims from third parties.

Most jurisdictions follow the principles of the UK Marine Insurance Act 1906, but local statutes and case law introduce variations. Businesses trading internationally must check the specific rules that apply in each relevant jurisdiction.