Menu

Get Expert Legal Support Today

Launching a start-up in the UK brings excitement and tough decisions about structure and compliance. Many founders think incorporation is only for big players or worry the process is complicated, yet registering a limited company with Companies House is a common, straightforward step. Choosing business incorporation gives your company a separate legal identity and limited liability protection, but it also means new responsibilities. This guide clears up misconceptions and explains what incorporation really offers, helping you make confident choices for your business.

Business incorporation is the formal process of registering a business as a limited company with Companies House under the Companies Act 2006. When you incorporate, your business becomes a separate legal entity distinct from you as an individual. This separation is one of the most powerful reasons founders choose incorporation in the first place.

Here’s what happens when you incorporate:

Unfortunately, several misconceptions surround incorporation that can lead to poor decisions.

Many founders believe incorporation is only for large companies or multinational operations. The truth? Incorporation is a straightforward, common procedure that applies to limited companies of all sizes across the UK. Small start-ups use it regularly.

Another widespread myth is that incorporating automatically protects your personal assets no matter what. Limited liability is powerful, but it’s not a blanket shield. If you personally guarantee a loan, that guarantee still stands. If you commit fraud or breach duties as a director, protection can be pierced.

Some founders think the incorporation process itself is complicated and time-consuming. In reality, the registration process is relatively straightforward when you understand the steps involved.

A third misconception: incorporation is always the right choice. Not every business needs to incorporate. Some work better as sole traders or partnerships. Your business structure should match your specific situation, growth plans, and liability exposure.

Incorporation creates a separate legal entity with its own rights and responsibilities, but it doesn’t eliminate all personal liability or make business decisions automatically lawful.

Understanding what incorporation actually is—and what it isn’t—helps you make the right choice for your start-up. Limited liability protection under company law exists specifically to encourage business growth while managing risk.

When you incorporate, you’re accepting certain obligations: filing requirements, director responsibilities, and accounting standards. These aren’t burdens; they’re the trade-off for legal separation and liability protection.

The key takeaway? Incorporation is a powerful tool with real benefits, but it requires understanding both what it delivers and what it doesn’t. Before incorporating, evaluate whether the benefits match your business needs and whether you’re prepared for the ongoing compliance responsibilities.

Pro tip: Speak with a legal advisor before incorporating to confirm it’s the right structure for your specific circumstances, rather than assuming it’s necessary or assuming it solves all liability concerns.

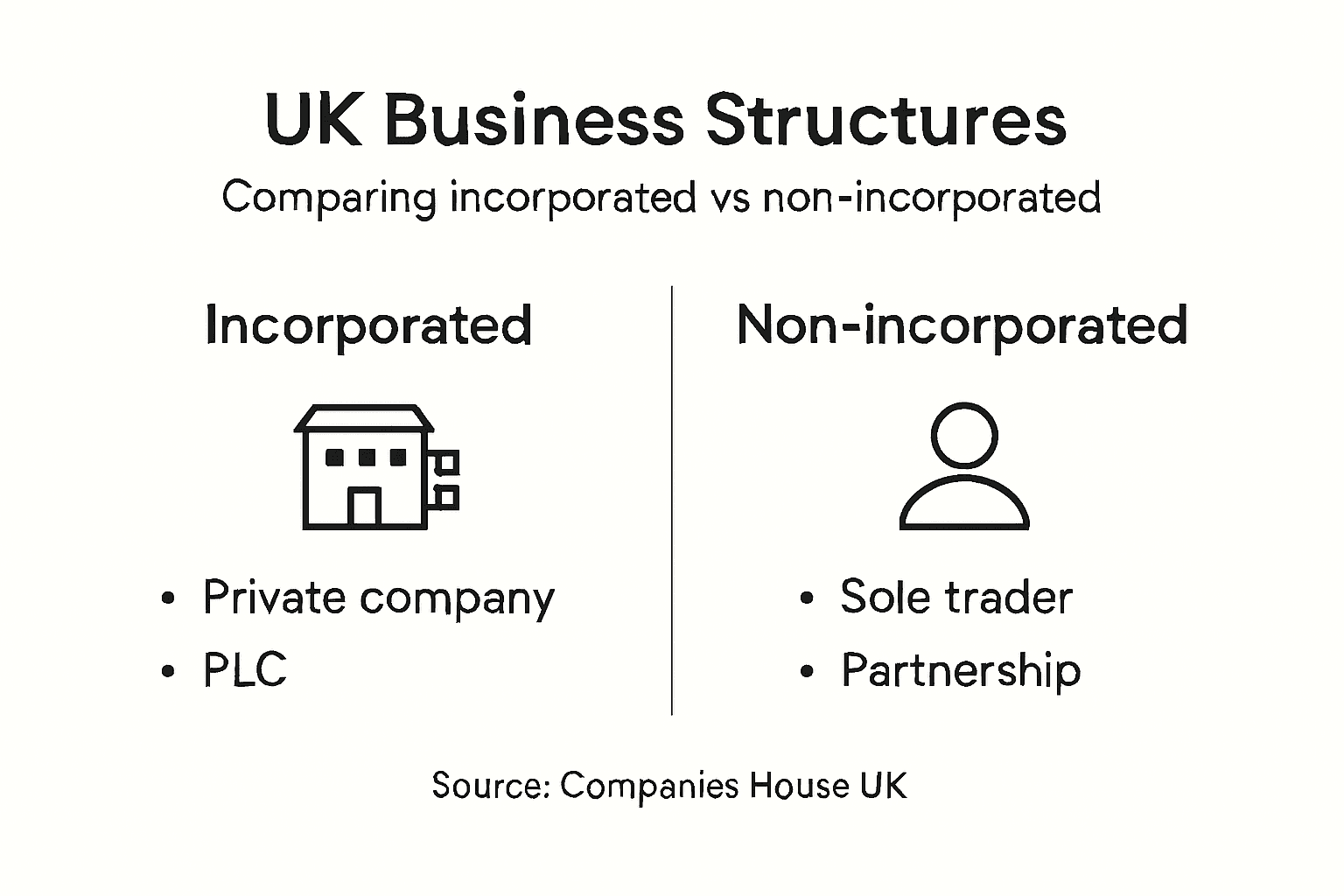

The UK offers several business structures, each with different legal implications, tax treatments, and compliance requirements. Choosing the right one shapes how your company operates, how much liability you carry, and what paperwork you must complete each year.

Understanding your options prevents costly mistakes and ensures you select the structure that matches your business goals.

The most common choice for start-ups is a private company limited by shares. This structure separates your personal liability from the company’s debts. Shareholders own the company through shares, and their liability is limited to their investment amount.

A private company limited by guarantee works differently. Instead of shares, members guarantee to contribute a fixed amount if the company fails. This structure suits charities and not-for-profit organisations more than commercial start-ups.

Private unlimited companies offer no liability protection. Your personal assets remain at risk if the business fails. Few start-ups choose this route because the liability exposure is significant.

Public limited companies (PLCs) can sell shares to the public and trade on stock exchanges. They require substantial capital, stricter governance, and greater disclosure requirements. Most start-ups never reach this stage.

A sole trader structure means you and your business are legally identical. You keep all profits but bear unlimited personal liability. Setup is simple and cheap, but your personal assets are exposed to business debts.

A partnership splits ownership between two or more people. Partners share profits and decision-making. Each partner can be held personally liable for the entire partnership’s debts—even those created by other partners.

Limited liability partnerships (LLPs) combine elements of both structures. Members gain limited liability protection whilst maintaining partnership flexibility. Corporate structures and director responsibilities vary significantly across these entity types, affecting your personal exposure and compliance burden.

A branch is an extension of an overseas company without separate legal personality. It operates under the parent company’s legal umbrella. A subsidiary is a separate legal entity, usually a limited company, owned by a parent company.

Community interest companies are limited companies with a social purpose. They must prove their activities benefit the community and restrict profit distribution.

Key differences at a glance:

Here is a summary of the main UK business structures and how they compare:

| Structure Type | Liability Level | Compliance Burden | Most Suitable For |

|---|---|---|---|

| Sole Trader | Unlimited | Minimal | Solo operations, freelancers |

| Partnership | Unlimited (jointly) | Moderate | Co-owned small businesses |

| Limited Company (Ltd) | Limited | High | Growing start-ups, SMEs |

| Limited Liability Partnership | Limited | Moderate to high | Professional practices |

| Public Limited Company (PLC) | Limited (shareholder) | Very high | Large, capital-seeking firms |

| Company Limited by Guarantee | Limited (guarantee) | High | Charities, not-for-profits |

| Private Unlimited Company | Unlimited | High | Rare, complex arrangements |

| Branch (of overseas co.) | Dependent on parent | Moderate | Foreign company expansion |

| Community Interest Company | Limited | High | Social enterprises |

Your choice of structure affects taxation, liability, funding opportunities, and ongoing administration. There is no universal “best” structure—only the right one for your circumstances.

Each structure triggers different tax treatments, accounting requirements, and regulatory obligations. A limited company requires annual filings with Companies House, audit requirements above certain thresholds, and director formalities. A sole trader files a self-assessment tax return with minimal compliance overhead.

Start-ups typically choose between sole trader status (if you’re solo and want simplicity) or a private company limited by shares (if you want liability protection and growth potential).

Pro tip: Consult a legal advisor before deciding on your structure; switching structures later creates complications and additional costs that proper upfront planning avoids.

Registering your company with Companies House transforms your business idea into a legal entity. The process is straightforward when you know what information and documents you need. Missing steps or incorrect details delay approval and waste time you could spend building your business.

The registration process typically takes 2-4 weeks when you submit everything correctly.

Gather these essentials before contacting Companies House:

Your registered office address is where Companies House sends official documents. It doesn’t need to be your trading address, but it must be a real, physical location in the UK.

The process follows a clear sequence:

Registering your private company requires submitting an application form specifying company name, registered office address, director details, shareholder information, and articles of association. Companies House reviews your submission for completeness and compliance.

Once approved, you receive a Certificate of Incorporation. This official document confirms your company exists as a separate legal entity. It’s your proof of incorporation and you’ll need it for opening a business bank account, securing contracts, and other official matters.

Registration isn’t the end; it’s the beginning. Your company must now:

Registration creates legal separation between you and your company, but it also creates compliance responsibilities that continue throughout your company’s life.

Many founders overlook these ongoing duties. Missing filing deadlines triggers penalties, and repeated failures can result in strike-off (removal from the register) or director disqualification.

Pro tip: Set calendar reminders for your confirmation statement and accounts filing deadlines now, or assign a team member to track them; most penalties result from missed deadlines rather than incorrect filings.

Incorporation isn’t free, and it’s not always the right choice. Understanding both the advantages and costs helps you make an informed decision that matches your business ambitions and financial reality.

The benefits can be substantial, but they come with trade-offs worth carefully considering.

The primary advantage is limited liability protection. Your personal assets remain separate from business debts. If your company fails, creditors cannot pursue your home, savings, or personal belongings. Your loss is limited to your share investment amount.

Incorporation also builds credibility with customers and investors. A limited company appears more established and trustworthy than a sole trader. Banks and suppliers often view incorporated businesses more favourably when evaluating loan applications or credit terms.

Your incorporated company can own property, enter contracts, and hold assets in its own name. This separation creates flexibility for business growth and makes transferring ownership easier if you eventually sell the company.

There are potential tax efficiencies too. Corporations pay corporation tax on profits rather than income tax. Depending on your income level and business structure, this can result in tax savings. You also have more flexibility in managing dividends and reinvestment of profits.

Incorporation demands higher compliance and administration costs. You must file statutory accounts with Companies House annually, complete tax returns, keep detailed records, and file confirmation statements. These requirements consume time and often require professional accountancy support.

Setup costs are modest (£12-40 in Companies House fees), but ongoing costs accumulate. Accountancy fees typically range from £800 to £2,500 annually depending on business complexity. If you need professional legal advice on corporate matters, those costs compound.

Limited liability incorporation protections come alongside dividend taxation and increased financial reporting obligations. Dividends you withdraw from profits are taxable, creating a “double taxation” effect where profits are taxed as corporation tax and again as dividend tax.

For small, low-profit businesses, the compliance burden often outweighs the benefits. A sole trader operating from home with minimal staff rarely needs limited liability protection.

Consider these recurring expenses:

These costs directly impact your cash flow. A business earning £30,000 profit annually may find accountancy fees consume 3-8% of profit.

The table below highlights key financial considerations for a newly incorporated business:

| Expense Type | Typical Annual Cost | Impact on Small Firms |

|---|---|---|

| Accountancy Services | £800 – £2,500 | Reduces cash flow, may be significant |

| Companies House Fees | £0 – £40 per filing | Modest, but recurring |

| Legal Advice | £200 – £500 per hour | Costly if ongoing issues |

| Corporation Tax Prep | Often included in fees | Essential for compliance |

| Dividend Tax | Variable | Further reduces net profits |

However, larger or growth-focused businesses often benefit. If you’re seeking investment, operating in regulated sectors, or planning significant growth, incorporation’s advantages justify the costs.

Incorporation creates a legal shield and enhances credibility, but it transforms you from a sole operator into a company director with compliance responsibilities and costs that reduce net profit.

Calculate your specific situation. Project your anticipated profits, estimate accountancy costs for your business complexity, and assess whether liability protection matters in your industry. Some sectors (consulting, online retail) carry minimal liability risk. Others (construction, healthcare) demand protection.

Pro tip: Request quotes from 2-3 accountants before incorporating; costs vary significantly, and finding an affordable, reliable accountant makes the difference between incorporation being worthwhile and becoming a financial drain.

Incorporation creates legal obligations that, when ignored, trigger serious consequences. Fines, director disqualification, and company dissolution are real penalties for non-compliance. Understanding the risks and common pitfalls helps you protect your business and reputation.

The good news: most mistakes are entirely preventable with proper planning and ongoing attention.

Once incorporated, your company must meet strict filing deadlines:

Missing even one deadline triggers penalties. First breach: £150. Second breach within 5 years: £375. Further breaches: £750 or more. Repeated non-compliance can lead to strike-off, removing your company from the register entirely.

Non-compliance with director responsibilities creates personal liability. Directors who fail to file accounts or confirmation statements can face prosecution. In serious cases, directors face disqualification from running any UK company for up to 15 years.

Many founders make preventable errors that damage their business from day one:

Choosing an unsuitable company name that infringes regulations or misleads customers. Names cannot be identical to existing companies, cannot suggest unwarranted connection to the government, and cannot include prohibited words without permission.

Providing incomplete or inaccurate information on application forms. Errors regarding director names, addresses, or shareholdings complicate future transactions and create compliance problems.

Using an inappropriate registered office address. A valid physical UK address is mandatory. Virtual offices are acceptable, but a residential address belonging to a director who doesn’t genuinely work there raises red flags with Companies House.

Failing to understand director responsibilities. Directors must act within company powers, avoid conflicts of interest, and maintain accurate records. Personal liability attaches to directors who act recklessly or fraudulently.

Incorporation protects personal assets from business debts, but the protection isn’t absolute. Personal liability pierces when directors:

Directors face personal liability for unpaid employee wages and tax debts in certain circumstances. This means your personal assets can still be pursued even though your company is incorporated.

Compliance is not optional; it’s the foundation of legal incorporation benefits. Non-compliance transforms incorporation from protection into liability.

Keep detailed records of all company decisions. Document board meetings, approval of financial statements, and significant business decisions. When regulators investigate, good record-keeping proves you acted responsibly and in good faith.

Pro tip: Implement a compliance calendar on day one, assigning responsibility for each deadline to a specific person; automate reminders 6 weeks before each filing date to ensure nothing slips through.

Starting your business journey with the right incorporation structure can be confusing and stressful. From understanding limited liability protection to navigating ongoing compliance responsibilities, the legal landscape requires clear guidance and trusted advice. If you want to avoid costly mistakes and shield yourself from personal liability while setting your company up for growth success, expert assistance is essential.

Ali Legal specialises in supporting UK start-ups through every step of the incorporation process. We provide straightforward advice, fixed fees, and dedicated long-term relationships to ensure you meet registration requirements and avoid common pitfalls such as missed filings or incorrect documentation. Don’t let compliance worries hold back your ambitions. Reach out today to discuss how our corporate and commercial legal services can give you confidence to focus on growing your business. Start building your legally sound company now by contacting us via Ali Legal Contact. For ongoing support with director responsibilities and company law compliance visit Corporate Law UK Guide and understand the importance of Limited Liability Protection for your peace of mind.

Business incorporation is the process of registering a business as a separate legal entity. It is important for start-ups as it provides limited liability protection for personal assets, allowing for growth while managing risk.

Common misconceptions include the belief that incorporation is only for large businesses, that it automatically protects personal assets in all situations, and that the process is overly complicated. In reality, incorporation can benefit businesses of all sizes and requires ongoing compliance and management.

Limited liability protection means that the personal assets of shareholders or directors are generally protected from the debts and liabilities of the business. If the company fails, creditors can only pursue the assets of the company itself, not the individual’s personal possessions, unless personal guarantees are made.

Incorporated companies must file a confirmation statement annually, submit annual accounts to Companies House, pay corporation tax on profits, maintain statutory records, and notify Companies House of any changes to directors or shareholders.